Europe Direct Drive Wind Turbine Market Size and Forecast 2025–2033

Low-Maintenance Wind Technology Powering Europe’s Renewable Transition

Market Snapshot

The Europe Direct Drive Wind Turbine Market is anticipated to reach US$ 8.94 billion in 2033 from US$ 4.11 billion in 2024, growing at a CAGR of 9.02% during 2025–2033. This expansion is driven by rising investments in renewable energy, supportive government policies, and growing demand for efficient, low-maintenance turbine systems. As Europe accelerates toward carbon-neutral targets, direct drive technology is emerging as a cornerstone of its sustainable energy future.

Europe Direct Drive Wind Turbine Market Overview

A direct drive wind turbine eliminates the conventional gearbox by connecting a low-speed generator directly to the turbine rotor. This design significantly reduces mechanical complexity, improving reliability, lowering maintenance costs, and extending service life. Because gearboxes are often the most failure-prone components in traditional turbines, their removal represents a major advancement in operational stability.

Across Europe, direct drive turbines are gaining strong traction, particularly in offshore wind farms and large-scale onshore installations where maintenance access is limited and downtime is costly. Countries such as Germany, Denmark, the Netherlands, and the United Kingdom have emerged as early adopters, integrating this technology into national renewable strategies. As the European Union pursues aggressive emission-reduction goals and energy independence, advanced turbine architectures like direct drive systems are becoming essential tools in reshaping the continent’s power landscape.

Growth Drivers in the Europe Direct Drive Wind Turbine Market

1. Rising Offshore Wind Installations

Europe has established itself as the global leader in offshore wind power. Nations including the United Kingdom, Germany, Denmark, and the Netherlands continue to expand offshore capacity in the North Sea and Baltic Sea. Direct drive turbines are ideally suited for offshore applications due to their low maintenance needs, high reliability, and fewer moving parts, reducing the frequency of service interventions in difficult marine environments.

With many European governments committing to ambitious offshore wind targets as part of their net-zero strategies, demand for gearbox-free turbine systems is accelerating. Offshore wind farms benefit significantly from reduced lifetime operating costs and improved availability, making direct drive systems an economically attractive choice.

A notable development occurred in June 2025, when ORLEN Neptun inaugurated Poland’s first offshore wind farm installation terminal in Świnoujście, one of the most advanced in Europe. The terminal will support large offshore projects and has entered a long-term cooperation with Ocean Winds, underscoring the region’s commitment to next-generation wind infrastructure.

2. Robust Government Policies and Stimulus

The European Green Deal and the Fit for 55 initiative have positioned renewable energy at the center of the region’s economic and environmental agenda. Financial incentives, carbon pricing mechanisms, and clean-energy mandates are actively encouraging investments in high-efficiency technologies, including direct drive turbines.

At the national level, governments are simplifying permitting processes, modernizing grid infrastructure, and providing subsidies for offshore and onshore wind projects. According to EU targets announced in October 2023, renewable energy must represent 42.5% or more of total energy consumption by 2030, requiring installed wind and renewable capacity to expand from 204 GW in 2022 to over 500 GW by 2030. Such ambitious objectives create a powerful tailwind for advanced turbine technologies that offer reliability and long-term economic value.

3. Technological Advancements in Generators

European leadership in engineering and renewable R&D has driven significant improvements in generator design, materials, and digital monitoring systems. Innovations in permanent magnet synchronous generators (PMSG) and electrically excited synchronous generators (EESG) have enhanced power density, reduced nacelle weight, and improved energy conversion efficiency.

The integration of predictive maintenance, IoT-based condition monitoring, and AI-driven performance optimization further boosts turbine uptime and output. As manufacturing costs decline and operational efficiency improves, direct drive turbines are increasingly selected for new installations and repowering projects. Europe is rapidly becoming a global hub for cutting-edge wind technology solutions.

Challenges in the Europe Direct Drive Wind Turbine Market

1. High Initial Investment Costs

Despite their operational advantages, direct drive turbines often require higher upfront capital investment, particularly when using permanent magnet technology. Specialized materials, advanced engineering, and precision manufacturing increase initial equipment costs. For smaller developers or onshore projects with tight budgets, this cost barrier may limit adoption, especially in regions with weaker financial incentives.

However, the total cost of ownership over a turbine’s lifecycle is typically lower due to reduced maintenance and downtime, making direct drive systems increasingly attractive for long-term infrastructure planning.

2. Dependence on Rare Earth Materials

Many direct drive turbines rely on permanent magnets made from rare earth elements such as neodymium and dysprosium. These materials are geographically concentrated and subject to price volatility and geopolitical risk. Europe’s dependence on imported rare earths presents strategic challenges for large-scale manufacturing.

In response, manufacturers and policymakers are accelerating research into alternative magnet technologies, recycling programs, and non-rare-earth generator designs, such as electrically excited synchronous generators. While progress is steady, material supply remains a critical consideration for the industry.

Europe Electrically Excited Synchronous Generator Market

Electrically Excited Synchronous Generators (EESGs) are gaining momentum as a viable alternative to permanent magnet systems. By eliminating rare earth components, EESGs reduce supply-chain vulnerabilities while maintaining high efficiency and scalability. These generators are particularly suited for large onshore and offshore wind farms, aligning with Europe’s sustainability goals and efforts to localize clean-energy manufacturing.

As Europe emphasizes resource independence and circular economy principles, EESG-based direct drive systems are expected to play an increasingly important role in future turbine designs.

Europe Less than 1MW Direct Drive Wind Turbine Market

Small-scale wind installations below 1MW capacity are essential for community energy projects, rural electrification, and hybrid renewable systems. Demand for compact direct drive turbines is rising in countries such as Italy and Spain, where decentralized energy initiatives and local incentives encourage adoption.

These systems offer quiet operation, simplified maintenance, and reliable performance in low-wind conditions, making them suitable for agricultural operations, residential developments, and small industrial facilities. Although a niche segment, this category contributes meaningfully to Europe’s distributed renewable energy ecosystem.

Europe Onshore Direct Drive Wind Turbine Market

Onshore wind remains a backbone of Europe’s renewable portfolio. As older wind farms approach the end of their operational life, repowering projects are replacing conventional geared turbines with modern direct drive systems. These upgrades increase capacity factors, improve grid stability, and significantly reduce maintenance requirements.

Direct drive turbines are particularly valuable for remote and difficult-to-access onshore sites, where service logistics are costly. With land availability constraints and growing efficiency expectations, this segment is poised for sustained expansion.

Europe Offshore Direct Drive Wind Turbine Market

Offshore wind is the fastest-growing segment in Europe’s renewable sector, and direct drive technology is rapidly becoming the standard for large offshore installations. By removing the gearbox—a common point of failure—direct drive turbines deliver superior durability, reduced operational expenditure, and enhanced reliability in harsh marine conditions.

Major offshore projects in the North Sea, Baltic Sea, and Atlantic coastlines are driving large-scale adoption. Backed by EU climate policies and national decarbonization commitments, the offshore direct drive market is set to experience strong long-term growth.

Country-Wise Market Insights

France

France is accelerating offshore wind development while modernizing its onshore fleet. Government initiatives promoting domestic manufacturing and technological innovation align closely with direct drive turbine adoption. In May 2022, Siemens Gamesa began manufacturing offshore direct drive nacelles and IntegralBlades at a new plant in Le Havre, marking one of France’s largest renewable energy investments and reinforcing the country’s role in next-generation wind technology.

Germany

As Europe’s largest wind energy market, Germany leads in both offshore deployment and turbine repowering. With advanced engineering capabilities and a robust supply chain, the country is a hub for high-efficiency generator R&D. Environmental constraints, space limitations, and aging infrastructure further strengthen the case for high-performance direct drive systems.

In February 2024, Inox Wind partnered with Germany-based Wind to Energy to introduce new turbine generators, highlighting continued innovation and international collaboration within the market.

United Kingdom

The UK is a global leader in offshore wind, with ambitious targets of 50 GW of offshore capacity by 2030. Direct drive turbines are favored for their low maintenance needs and strong performance in marine environments. Government subsidies and private investment are driving new manufacturing facilities and expanding domestic supply chains.

In July 2022, Hitachi Energy secured a major contract from Ørsted to deliver HVDC systems for the Hornsea 3 offshore wind farm, further supporting the integration of large-scale direct drive turbine installations.

Russia

Although still emerging, Russia’s wind energy sector is gradually expanding due to policy shifts and foreign partnerships. Direct drive turbines are particularly attractive for remote and cold regions, where maintenance access is limited. In December 2024, Rosatom opened a wind turbine blade factory, signaling growing domestic production capabilities. However, geopolitical challenges and limited supply chains continue to constrain rapid market expansion.

Market Segmentation

By Technology

Electrically Excited Synchronous Generator (EESG)

Permanent Magnet Synchronous Generator (PMSG)

By Capacity

Less than 1MW

Between 1MW and 3MW

Greater than 3MW

By Deployment Location

Onshore

Offshore

By Country

France, Germany, Italy, Spain, United Kingdom, Belgium, Netherlands, Russia, Poland, Greece, Norway, Romania, Portugal, Rest of Europe

Company Coverage (Five Viewpoints Each)

Overviews

Key Person

Recent Developments

SWOT Analysis

Revenue Analysis

Key Players

Siemens Gamesa Renewable Energy SA, ENERCON GmbH, Leitner AG, Emergya Wind Technologies B.V., ABB Ltd, VENSYS Energy AG, ReGen Powertech Pvt. Ltd, Northern Power Systems, Rockwell Automation Inc.

Final Thoughts

The Europe Direct Drive Wind Turbine Market is positioned at the forefront of the continent’s clean-energy transformation. With the market projected to grow from US$ 4.11 billion in 2024 to US$ 8.94 billion by 2033, direct drive technology is redefining how wind power is generated, maintained, and scaled.

Although challenges remain—particularly regarding initial capital costs and rare-earth material dependency—the long-term benefits of reliability, efficiency, and reduced operational expenditure far outweigh these obstacles. Supported by strong policy frameworks, accelerating offshore development, and continuous technological innovation, direct drive turbines are rapidly becoming the preferred solution for Europe’s next generation of wind infrastructure.

As Europe advances toward a carbon-neutral future, direct drive wind technology will not only power grids but also symbolize the region’s commitment to sustainable, resilient, and forward-looking energy systems.

About the Creator

Marthan Sir

Educator with 30+ years of teaching experience | Passionate about sharing knowledge, life lessons & insights | Writing to inspire, inform, and empower readers.

Keep reading

More stories from Marthan Sir and writers in The Swamp and other communities.

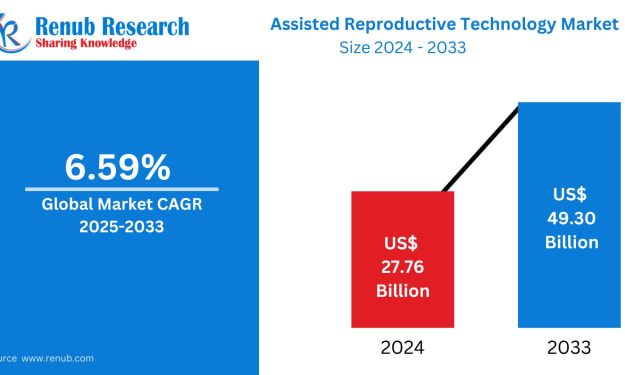

Assisted Reproductive Technology Market Size and Forecast 2025–2033

Introduction: A New Era in Family Building Assisted Reproductive Technology (ART) has transitioned from being a niche medical solution into a globally recognized pathway for family creation. What once addressed only select infertility challenges now encompasses a wide array of technologies designed to support diverse medical, social, and personal reproductive needs. From in vitro fertilization (IVF) and intracytoplasmic sperm injection (ICSI) to cryopreservation, genetic screening, and donor programs, ART has become central to modern reproductive healthcare.

By Marthan Sir6 days ago in The Swamp

Japanese Stocks Soar to Record Highs Amid Speculation of Snap Election

Japanese equities surged to fresh record highs this week, as investors reacted positively to growing speculation of a snap parliamentary election. The Nikkei 225 and Topix indexes have reached levels not seen in decades, reflecting a renewed sense of optimism about the country’s political and economic trajectory. Market watchers say the momentum is being fueled by expectations that the government will seek a fresh mandate to strengthen its economic agenda. A Market on the Rise The Nikkei 225, Japan’s premier stock index, recently climbed to an all-time high, while the broader Topix index followed suit. Analysts attribute the rise to a combination of domestic political signals and global market trends. With signs that a snap election may be called, investors appear to be positioning themselves for a stable, pro-business government that could implement economic policies favoring growth and corporate earnings. Historically, Japanese markets tend to respond positively to political certainty. Investors prefer a clear and decisive government agenda, which can reduce uncertainty and provide confidence in future policy decisions. The current surge in stock prices seems to reflect this sentiment, as traders anticipate that an early election could consolidate support for the ruling coalition, providing a smoother path for upcoming economic initiatives. Political Expectations Driving Investor Behavior Reports suggest that Prime Minister Fumio Kishida and his advisors are considering a snap election to reinforce their mandate, particularly ahead of major fiscal and policy decisions. Markets often react strongly to such developments, as political stability is closely linked to economic planning and investment confidence. “This is a classic case of politics driving market optimism,” said Hiroshi Tanaka, a senior economist at Tokyo-based Nomura Securities. “Investors are betting that a successful election will give the government the authority to push forward with policies that could stimulate corporate earnings and overall economic growth.” The expectation of a snap poll has also fueled speculation in specific sectors. Technology, manufacturing, and export-oriented companies have seen their stock values rise sharply, as these industries are expected to benefit from government policies supporting innovation, trade, and infrastructure development. Global Influences and Investor Sentiment While domestic politics play a key role, global factors have also contributed to the stock market’s momentum. Strong corporate earnings reports, stable interest rates, and an overall positive outlook for international trade have combined to create an environment conducive to market growth. The yen’s recent fluctuations against the dollar have also attracted investor attention. A slightly weaker yen tends to benefit exporters, as Japanese goods become more competitively priced in global markets. This dynamic has contributed to the bullish sentiment among foreign and domestic investors alike. Market analysts warn, however, that while optimism is high, investors should remain cautious. Political developments can be unpredictable, and unexpected changes in government policy or global economic conditions could quickly alter market dynamics. Sector Highlights and Key Performers Several sectors have emerged as key beneficiaries of the current market surge. Technology companies, including those specializing in robotics, semiconductors, and consumer electronics, have seen notable gains. These firms are expected to capitalize on both domestic policy incentives and international demand. The manufacturing sector has also performed well, particularly companies involved in automotive and heavy machinery production. Analysts believe that government-backed infrastructure projects and potential incentives for green technology and sustainable manufacturing could further support these industries. Additionally, export-oriented businesses are benefiting from favorable foreign exchange conditions. A slightly softer yen enhances profit margins for companies selling products overseas, attracting investor interest and pushing stock prices higher. Investor Strategies and Market Outlook Financial advisors are recommending a balanced approach amid this rally. While the market’s upward trajectory is encouraging, the possibility of volatility remains. Investors are being advised to diversify portfolios, consider long-term growth prospects, and remain aware of political and economic developments that could influence market conditions. “The current momentum is exciting, but we must remember that markets are forward-looking and can react sharply to any change in expectations,” noted Keiko Mori, an investment strategist at Mitsubishi UFJ Financial Group. “It’s essential for investors to stay informed and remain disciplined in their strategies.” Looking ahead, the market’s trajectory will likely hinge on the timing and outcome of the anticipated snap election. If the government secures a strong mandate, Japan’s stock market could continue its record-breaking run, supported by policy measures aimed at fostering innovation, infrastructure growth, and corporate profitability. Conversely, any political setbacks or global economic disruptions could temper enthusiasm and lead to short-term corrections. Analysts emphasize the importance of monitoring both domestic political developments and international economic trends to understand the market’s future direction. Conclusion Japan’s stock market rally underscores the deep connection between political developments and investor sentiment. The prospect of a snap election has ignited optimism, pushing the Nikkei 225 and Topix indexes to unprecedented levels. While opportunities abound, market participants are reminded that volatility remains a constant companion, and informed, strategic investment decisions are crucial. As Japan navigates the dual challenges of political strategy and economic growth, investors around the world will be watching closely, eager to see whether the market’s record highs are a prelude to sustained expansion or a momentary peak fueled by election-year speculation.

By Muhammad Hassan6 days ago in The Swamp

Comments

There are no comments for this story

Be the first to respond and start the conversation.