European Union Passenger Car Market Size and Forecast 2025–2033

Electric Mobility, Smart Technologies, and Policy Support Reshape Europe’s Automotive Landscape

Introduction

The European Union passenger car market stands at a pivotal crossroads, balancing decades of automotive heritage with an accelerating transition toward electrification, sustainability, and digital mobility. Passenger cars remain an integral part of daily life across Europe, supporting commuting, tourism, logistics, and personal mobility in one of the world’s most urbanized and infrastructure-rich regions.

According to Renub Research, the European Union Passenger Car Market is expected to reach 12.06 million units by 2033, up from 10.72 million units in 2024, growing at a compound annual growth rate (CAGR) of 1.32% from 2025 to 2033. While growth appears moderate, the structural transformation underway—driven by electric vehicles (EVs), regulatory reforms, and technological innovation—marks a profound shift in how vehicles are designed, produced, and consumed across EU member states.

European Union Passenger Car Market Overview

Passenger cars are primarily designed for transporting people, typically seating up to five occupants, and are used extensively for personal mobility, business travel, and tourism. Europe’s dense road networks, advanced urban planning, and high standards of living have long supported strong demand for passenger vehicles.

Compact and fuel-efficient cars dominate crowded metropolitan areas, while SUVs and premium vehicles enjoy popularity in suburban and high-income segments. Over the past decade, however, electric and hybrid vehicles have gained momentum due to tightening emissions regulations, environmental awareness, and government incentives.

The EU is home to some of the world’s most influential automotive manufacturers, including Volkswagen, BMW, Mercedes-Benz, Renault, and Stellantis. These companies continue to invest heavily in electrification, software integration, and autonomous technologies, ensuring Europe remains a global automotive innovation hub.

Growth Drivers in the European Union Passenger Car Market

Government Incentives and Emission Regulations

One of the strongest drivers shaping the EU passenger car market is regulatory policy. The European Green Deal and Fit for 55 initiatives aim to drastically reduce carbon emissions, pushing automakers and consumers toward cleaner mobility solutions. Governments across the EU provide financial incentives such as purchase subsidies, tax exemptions, lower registration fees, and reduced road taxes for electric and low-emission vehicles.

Additionally, the EU Emissions Trading System (EU ETS) places a price on carbon emissions, encouraging cost-effective reductions across industries. These policies not only stimulate EV demand but also accelerate the development of charging infrastructure, battery recycling facilities, and domestic EV supply chains, fundamentally reshaping the passenger car ecosystem.

Innovation in Electric and Autonomous Technologies

Technological advancement is revolutionizing Europe’s passenger car market. Automakers are launching next-generation electric models with longer driving ranges, faster charging capabilities, and enhanced safety features. Battery costs continue to decline, while improvements in energy density make EVs increasingly competitive with internal combustion engine vehicles.

Parallel investments in autonomous driving, artificial intelligence, and vehicle connectivity are redefining the driving experience. In January 2025, Mercedes-Benz Drive Pilot became the first approved Level 3 autonomous driving system in Germany, marking a milestone for production vehicles operating at speeds of up to 95 km/h. Such innovations enhance safety, convenience, and efficiency, particularly appealing to younger, tech-savvy European consumers.

Urbanization and Car-Sharing Trends

Urbanization across Europe has intensified demand for compact, low-emission vehicles suitable for congested city environments. At the same time, car-sharing and mobility-as-a-service (MaaS) platforms are gaining popularity among environmentally conscious and cost-sensitive consumers.

Manufacturers are responding by designing urban-friendly vehicles with digital connectivity, flexible ownership models, and reduced environmental footprints. In 2023, Hertz partnered with Uber to deploy 25,000 electric vehicles across European capital cities by 2025, aligning with Uber’s goal of becoming a zero-emission platform by 2030. These evolving mobility patterns are diversifying demand while reinforcing sustainability objectives.

Challenges in the European Union Passenger Car Market

High Costs of Electric Vehicles and Infrastructure Gaps

Despite incentives, electric vehicles remain relatively expensive compared to traditional petrol and diesel cars. Battery production, advanced materials, and software integration contribute to higher upfront costs. Moreover, EV charging infrastructure remains unevenly distributed, particularly in rural and economically weaker regions.

This disparity affects consumer confidence and adoption rates. Until charging networks become universally accessible and economies of scale significantly reduce EV prices, affordability concerns will continue to limit the pace of market transformation.

Supply Chain Disruptions and Component Shortages

The EU passenger car industry has faced persistent supply chain challenges in recent years. Semiconductor shortages, geopolitical tensions, and reliance on Asian manufacturing hubs have disrupted production schedules and increased costs.

Automakers have been forced to delay vehicle launches, reduce feature availability, or temporarily shut down production lines. These disruptions undermine market stability and highlight the need for regionalized supply chains, strategic inventories, and local production of critical components to ensure long-term resilience.

Segment Analysis

European Union Sedan Passenger Car Market

Sedans remain an important segment in Europe, offering a balance of comfort, fuel efficiency, and refined design. While SUVs and hatchbacks have gained popularity, sedans continue to attract corporate users and urban professionals, particularly in Germany, France, and Italy.

The integration of hybrid and electric powertrains, advanced infotainment systems, and connectivity features has helped sustain demand in this segment, especially within mid-size and luxury categories.

European Union Petrol Passenger Car Market

Petrol-powered vehicles still account for a substantial share of the EU market, especially in regions with limited EV infrastructure. Their lower purchase price, widespread refueling availability, and improved fuel efficiency keep them attractive to budget-conscious consumers.

Although regulatory pressure is steadily reducing their long-term prospects, petrol cars are expected to remain relevant in rural areas and price-sensitive segments throughout the forecast period.

European Union Battery Electric Passenger Car Market

Battery electric vehicles (BEVs) represent the fastest-growing segment in the EU passenger car market. Strong policy support, environmental awareness, and declining operating costs are accelerating adoption.

Countries such as Germany and the Netherlands lead in BEV penetration, supported by extensive charging networks and fiscal incentives. Continued investment in battery manufacturing and recycling positions the BEV segment for sustained growth through 2033.

European Union Hybrid Electric Passenger Car Market

Hybrid electric vehicles (HEVs) offer a practical transition solution for consumers hesitant to adopt full electric mobility. They provide improved fuel efficiency, lower emissions, and reduced range anxiety, making them especially attractive in urban low-emission zones.

Manufacturers are expanding hybrid offerings across vehicle categories, ensuring steady demand as Europe gradually transitions toward full electrification.

European Union Manual Transmission Passenger Car Market

Manual transmission vehicles have traditionally dominated European roads due to affordability and fuel efficiency. While demand is gradually declining as automatics become more common—especially in EVs—manual cars remain popular in Eastern and Southern Europe, particularly in entry-level and fleet segments.

This segment is expected to persist in cost-sensitive markets over the near to medium term.

Country-Level Insights

France Passenger Car Market

France remains a major EU passenger car market, driven by strong domestic brands such as Renault, Peugeot, and Citroën. Government incentives and scrappage programs actively promote low-emission vehicles. In 2024, the French new car market declined by 3.17% to 1.72 million units, with the Renault Clio and Peugeot 208 leading sales.

Germany Passenger Car Market

Germany is the EU’s largest passenger car market and a global automotive powerhouse. Home to Volkswagen, BMW, and Mercedes-Benz, the country leads innovation in EVs, premium vehicles, and autonomous driving. Strong government support and industrial capacity make Germany a trendsetter for the broader European market.

United Kingdom Passenger Car Market

Although no longer part of the EU, the UK remains influential in the European automotive ecosystem. Demand for electric and hybrid vehicles is rising rapidly, supported by the government’s plan to phase out new petrol and diesel car sales by 2035.

Netherlands Passenger Car Market

The Netherlands stands out as a leader in electric mobility, with high EV adoption rates, dense charging infrastructure, and favorable tax policies. Dutch consumers prioritize sustainability, efficiency, and connectivity, positioning the country at the forefront of Europe’s EV transition.

Competitive Landscape

Key companies operating in the European Union passenger car market include:

Volkswagen AG

Stellantis N.V.

Renault S.A.

BMW AG

Mercedes-Benz Group

Toyota Motor Europe

Ford Motor Company

Volvo Car Corporation

Nissan Motor Co., Ltd.

Each company is analyzed across four viewpoints: overview, key leadership, recent developments & strategies, and financial insights, reflecting intense competition and continuous innovation.

Final Thoughts

The European Union passenger car market is entering a defining decade. While overall unit growth remains steady, the transformation toward electric, connected, and sustainable mobility is reshaping every aspect of the industry—from manufacturing and infrastructure to consumer behavior and policy frameworks.

With Renub Research projecting market volumes to reach 12.06 million units by 2033, Europe’s automotive future will be defined less by scale and more by innovation, environmental responsibility, and adaptability. For manufacturers, policymakers, and consumers alike, the journey ahead is not just about mobility—it is about redefining how Europe moves.

About the Creator

Renub Research

Renub Research is a Market Research and Consulting Company. We have more than 15 years of experience especially in international Business-to-Business Researches, Surveys and Consulting. Call Us : +1-478-202-3244

Keep reading

More stories from Renub Research and writers in Serve and other communities.

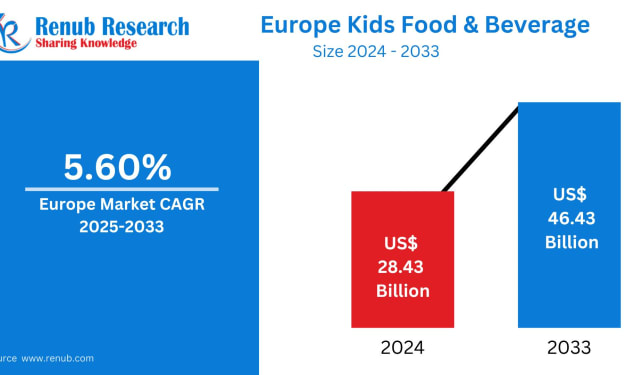

Europe Kids Food & Beverage Market Size and Forecast 2025–2033

Introduction The European kids food and beverage market is undergoing a profound transformation as parents, policymakers, and manufacturers collectively focus on improving childhood nutrition. Once dominated by sugary snacks and heavily processed convenience foods, the market has evolved toward healthier, cleaner, and more transparent offerings designed to support children’s growth, immunity, and overall well-being.

By Renub Research26 days ago in Feast

Stolen Bike, Not Valor

Koa was riding his new electric bike through the city park not too far from the US Embassy where he served in an Asian country. The ride was a part of his daily evening workout. He didn't really like the idea of an electric bike because he thought it was lazy. Besides, Koa had another good mountain bike he'd bought here used and it gave him a much better workout. But this one was his girlfriend's gift for his 29th birthday that she had taken the trouble to ship to him across the ocean. Koa felt obliged to ride it out at least occasionally, but promised himself not to use the battery. He even took it off the bike, to avoid the temptation.

By Lana V Lynx21 days ago in Serve

Let's Don't Do This

"I just can't do this anymore..." "Do what?" What can't you do? Put gas in your own car? I swear to God you make me take care of everything, don't you? You know I'm on my way to work right now but that never stops you from bothering me, does it?"

By Shirley Belk6 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.