Saudi Arabia Osteoporosis Drugs Market Size and Forecast (2025–2033)

How Saudi Arabia’s Aging Population, Biologics Boom, and Vision 2030 Reforms Are Reshaping Bone Health Treatment

The Saudi Arabia Osteoporosis Drugs Market is entering a transformative era, driven by shifting demographics, healthcare reforms, and growing awareness of bone health. According to Renub Research, the market is expected to reach US$ 308.84 million by 2033, up from US$ 210.89 million in 2024, reflecting a CAGR of 4.33% between 2025 and 2033.

The rise in osteoporosis cases—especially among postmenopausal women and older men—combined with the rapid adoption of biologic therapies and government-backed healthcare initiatives, is fueling the market’s expansion. While bisphosphonates continue to dominate due to affordability and clinical familiarity, biologics and new-generation treatments are emerging as growth leaders.

Below is an in-depth, editorial-style overview of what is driving this market, where it is headed, and why Saudi Arabia is becoming a key market for osteoporosis therapeutics in the Middle East.

Saudi Arabia Osteoporosis Drugs Market Overview

Osteoporosis has become a significant public health issue in Saudi Arabia due to longer life expectancy, sedentary lifestyles, insufficient calcium intake, and vitamin D deficiency—a common concern in the region. As the population ages rapidly, cases of bone fragility, fractures, and chronic musculoskeletal issues are climbing.

Supported by Vision 2030, the Kingdom is actively reforming its healthcare system with a strong focus on early diagnosis, preventive care, and domestic pharmaceutical development. These reforms are improving patient access to diagnostic tools like DEXA scans, broadening treatment options, and accelerating the adoption of innovative drugs, including monoclonal antibodies.

Both branded and generic medications play a crucial role, with generics expected to maintain strong demand in provinces with limited specialty care access. Meanwhile, biologics—known for their superior efficacy—are steadily gaining market share, especially in urban centers.

However, challenges remain. Many patients still struggle with long-term adherence, and rural access to diagnostics and specialist care is limited. Overcoming these issues through digital health tools, integrated care pathways, and fracture liaison services will be vital to reducing the long-term economic burden of osteoporosis.

Key Factors Driving Market Growth

1. A Rapidly Aging Population

One of the strongest drivers of the osteoporosis drugs market is the growing elderly demographic. As life expectancy increases and more citizens enter the 60+ age bracket, osteoporosis risk naturally rises.

This demographic shift has created:

Higher volumes of diagnosed osteoporosis

Increased rates of hip, spine, and wrist fractures

Stronger demand for fracture-prevention therapies

As more Saudis live longer, healthcare providers are seeing a clear rise in chronic bone-related disorders. This makes sustained therapeutic management essential, accelerating growth in both conventional and advanced drug classes.

2. Higher Rates of Screening and Diagnosis

The availability of DEXA and bone mineral density (BMD) assessments across hospitals and clinics has significantly improved early detection rates. Postmenopausal women—historically the most at-risk group—are increasingly undergoing preventive screenings.

Government-led public awareness campaigns and hospital-led wellness programs are encouraging early testing, often before the onset of fractures.

This surge in screening means:

More patients are diagnosed earlier

Treatment begins sooner

Long-term therapeutic demand increases

With early detection improving year after year, the pool of treatable patients continues to expand, directly lifting the market.

3. Government-Initiated Medical Programs

Saudi Arabia’s government plays a central role in driving expansion through its Vision 2030 healthcare transformation strategies, which include:

Public health education campaigns

Preventive screenings and risk assessments

Subsidized treatment options

Drug reimbursement programs

Investments in local pharmaceutical manufacturing

These initiatives reduce patient costs and expand access to therapies—particularly in low-income and rural areas. By promoting osteoporosis awareness and improving provider training, the government is enabling earlier intervention and better long-term treatment outcomes.

Major Challenges in the Market

1. Low Persistence and Adherence

A recurring challenge globally—and in Saudi Arabia—is poor treatment adherence. Osteoporosis therapies, particularly oral bisphosphonates, often require strict dosing regimens. Many patients discontinue due to:

Lack of noticeable immediate benefits

Fear of side effects

Limited understanding of disease progression

Cultural attitudes about long-term medicine use

Non-adherence leads to higher fracture rates and escalated healthcare costs. Addressing this through patient education, digital follow-up tools, and alternative dosing schedules (e.g., quarterly or annual injectables) will be key to improving outcomes.

2. Gaps in Early Detection and Post-Fracture Care

While screening is rising, many at-risk individuals—especially in rural regions—remain undiagnosed. Similarly, fracture liaison services (FLS), which link hospitals to long-term care programs, remain limited outside major cities.

Improving these services could significantly reduce economic burden and improve health outcomes.

Saudi Arabia Osteoporosis Drugs Market: Regional Analysis

Osteoporosis drug demand is highest in urban hubs such as Riyadh, Jeddah, Dammam, and Dhahran—regions with stronger healthcare systems, more specialists, and greater patient awareness. Below is a detailed breakdown.

Dhahran

Dhahran’s osteoporosis drugs market benefits from highly advanced facilities such as Johns Hopkins Aramco Healthcare, which supports cutting-edge diagnostics and bone health management.

Growing early detection rates among Aramco employees and the local population have increased the use of:

Bisphosphonates

New-generation biologics like denosumab

The Vision 2030 expansion, including a new hospital in Dhahran Al-Janoub, is expected to further improve access to DEXA scanning and specialist care. Still, fracture liaison services remain underdeveloped, and expanding them could dramatically improve adherence and post-fracture outcomes.

Riyadh

As the Kingdom’s capital, Riyadh has the most advanced healthcare ecosystem, featuring large hospitals and specialized osteoporosis programs.

Market growth is driven by:

A large elderly population

High prevalence of postmenopausal osteoporosis

Strong physician adoption of biologics

Government-supported reimbursement policies help ensure strong patient uptake. However, awareness gaps persist in suburban districts, and digital health integration could play a crucial role in improving patient monitoring.

Jeddah

Jeddah’s strategic role as a commercial and medical hub boosts its osteoporosis drugs market. Key hospitals like the International Medical Center and King Fahd Hospital support a wide range of diagnostics, including DEXA and advanced endocrinology services.

Treatments commonly prescribed include:

Bisphosphonates

Denosumab

Romosozumab

Challenges include inconsistent follow-up protocols and lower long-term treatment adherence. Expanding patient education and digital tracking solutions could help improve persistence.

Market Segmentations

By Product Type

Bisphosphonates

Calcitonin

Rank Ligand Inhibitors (e.g., Denosumab)

Parathyroid Hormone (PTH) Therapy

Selective Estrogen Receptor Modulators (SERMs)

Sclerostin Inhibitors (e.g., Romosozumab)

Others

By Route of Administration

Oral

Injectable

Others

By States

Dhahran

Riyadh

Khobar

Jeddah

Dammam

Others

Key Companies Profiled

The Saudi Arabia Osteoporosis Drugs Market features a strong mix of multinational pharmaceutical giants and regional players, including:

Amgen Inc.

Eli Lilly and Company

F. Hoffmann-La Roche AG

GlaxoSmithKline Plc

Merck & Co. Inc.

Novartis AG

Pfizer Inc.

Teva Pharmaceutical Industries Ltd.

UCB S.A.

For each company, the report includes:

Overview

Key Executives

Recent Developments

SWOT Analysis

Revenue Insights

Product Portfolio Analysis

Final Thoughts

Saudi Arabia’s osteoporosis drugs market is positioned for steady growth through 2033, fueled by a combination of demographic shifts, advancements in therapeutic options, heightened screening, and strong government involvement. While bisphosphonates remain the backbone therapy, biologics and next-generation treatments are ushering in a new era of improved outcomes and patient satisfaction.

Addressing treatment adherence, expanding diagnostic access, and implementing integrated post-fracture care models will be key to maximizing long-term benefits. As the Kingdom continues to modernize its healthcare infrastructure under Vision 2030, the osteoporosis drugs market will remain a central pillar in its chronic disease management landscape.

About the Creator

jaiklin Fanandish

Jaiklin Fanandish, a passionate storyteller with 10 years of experience, crafts engaging narratives that blend creativity, emotion, and imagination to inspire and connect with readers worldwide.

Keep reading

More stories from jaiklin Fanandish and writers in Longevity and other communities.

Japan Age-Related Macular Degeneration (AMD) Market Size and Forecast 2025–2033

Japan is stepping into a crucial decade in its fight against Age-Related Macular Degeneration (AMD), a leading cause of vision loss among older adults. According to Renub Research, the Japan Age-Related Macular Degeneration (AMD) Market is projected to reach US$ 897.79 million by 2033, rising from US$ 526.46 million in 2024, reflecting a CAGR of 6.11% from 2025 to 2033. As the nation with one of the highest proportions of elderly citizens globally, Japan faces a growing health challenge that is reshaping its pharmaceutical landscape, healthcare priorities, and diagnostic infrastructure.

By jaiklin Fanandishabout a month ago in Longevity

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts12 days ago in Longevity

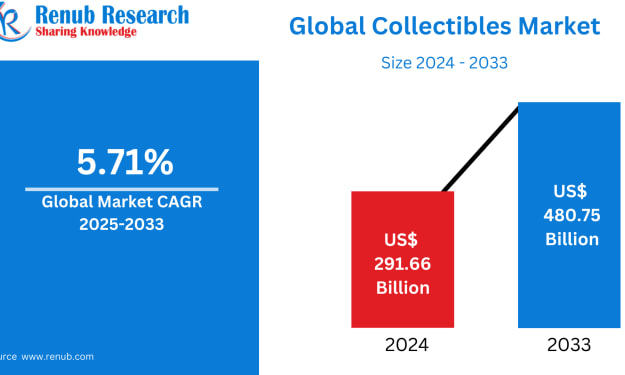

Collectibles Market Size and Forecast 2025–2033

Collectibles Market Outlook 2025–2033 The global Collectibles Market is expected to reach US$ 480.75 billion by 2033, expanding from US$ 291.66 billion in 2024, at a CAGR of 5.71% from 2025 to 2033. This steady rise reflects a powerful convergence of emotional value, investment potential, and technological innovation. From fine art and rare coins to trading cards, pop culture memorabilia, and digital collectibles, the industry continues to broaden its appeal across age groups, geographies, and income levels.

By Renub Research6 days ago in Longevity

How to Succeed at the Benson Directory®

Congratulations and welcome to the Benson Directory® employee #22391! As our newest call handler, you will have the privilege of speaking with dozens of unique and interesting people on a daily basis as well as the opportunity to earn bonuses for high performance. Contained within this handbook you will find a set of ease to follow instructions designed to help you settle in to your new role and begin paving the way to success.

By S. A. Crawforda day ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.