Saudi Arabia Dialysis Market Size and Forecast 2025–2033

Rising Burden of Kidney Disease and Vision 2030 Reforms Fuel Long-Term Growth

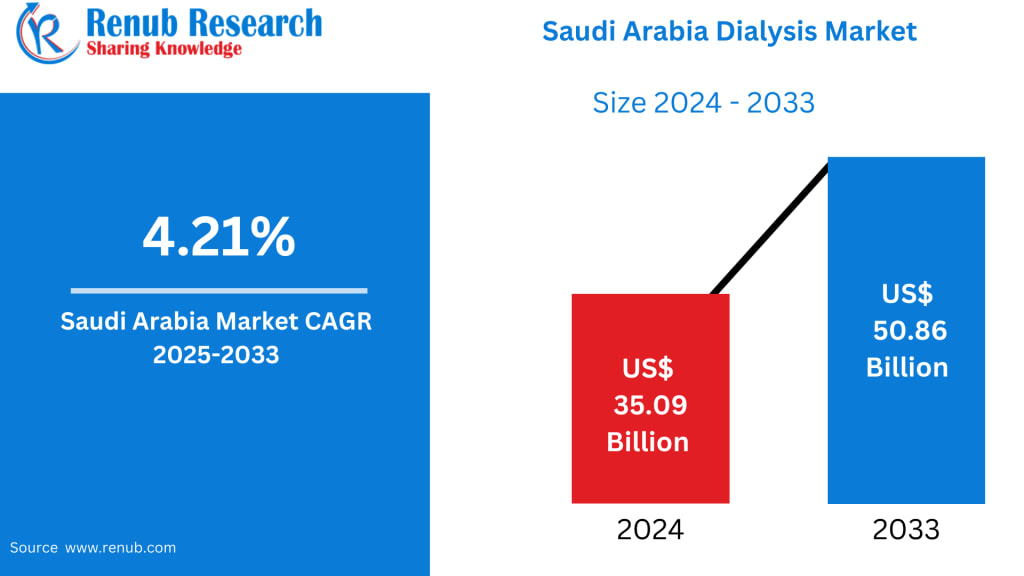

Saudi Arabia Dialysis Market Overview

The Saudi Arabia Dialysis Market is estimated to grow significantly, increasing from US$ 35.09 billion in 2024 to US$ 50.86 billion by 2033, expanding at a compound annual growth rate (CAGR) of 4.21% during 2025–2033, according to Renub Research estimates. This growth trajectory reflects the mounting prevalence of kidney-related disorders, expanding healthcare investments, and the Kingdom’s strategic push to modernize medical infrastructure under Vision 2030.

Dialysis remains a critical life-sustaining therapy for patients suffering from acute kidney injury and chronic kidney disease (CKD), especially those progressing to end-stage renal disease (ESRD). In Saudi Arabia, the increasing incidence of diabetes, hypertension, and obesity—three major contributors to CKD—has significantly expanded the patient pool requiring long-term renal replacement therapy.

Over the past decade, the Saudi healthcare ecosystem has made notable progress in expanding dialysis capacity. Government-led initiatives, coupled with private sector participation, have resulted in the establishment of modern dialysis centers equipped with advanced hemodialysis and peritoneal dialysis technologies. As a result, access to renal care services has improved, particularly in urban and semi-urban areas, positioning dialysis as one of the fastest-growing segments of the Kingdom’s healthcare industry.

Saudi Arabia Dialysis Market Outlook

Dialysis is a clinical process that removes toxins, waste products, and excess fluids from the blood when the kidneys are no longer able to perform these functions efficiently. In Saudi Arabia, dialysis is increasingly essential due to the rising prevalence of lifestyle-related diseases and an aging population.

There are two primary dialysis modalities in use across the country:

Hemodialysis (HD): Blood is filtered externally using a dialysis machine, typically in a hospital or specialized dialysis center.

Peritoneal Dialysis (PD): The lining of the abdomen acts as a natural filter, allowing treatment to be carried out at home in many cases.

Saudi Arabia has heavily invested in expanding dialysis services, with both public hospitals and private providers increasing their treatment capacity. Awareness campaigns and improved diagnostic infrastructure have also contributed to earlier identification of kidney disease, although late-stage diagnosis remains common. As healthcare access improves and patient survival rates increase, the long-term demand for dialysis services, equipment, and consumables is expected to remain strong throughout the forecast period.

Growth Drivers in the Saudi Arabia Dialysis Market

Rising Burden of Chronic Kidney Disease (CKD)

Saudi Arabia is witnessing a sharp rise in non-communicable diseases (NCDs), particularly diabetes, hypertension, obesity, and cardiovascular conditions. These disorders are closely linked to kidney damage and together account for a significant share of national mortality. As CKD progresses to ESRD, dialysis becomes the primary treatment option for patient survival.

A growing elderly population further amplifies dialysis demand, as kidney function naturally declines with age. Additionally, low rates of early CKD detection mean that many patients are diagnosed at advanced stages, requiring immediate and ongoing dialysis. Because dialysis treatments are repetitive and long-term—often conducted multiple times per week—this expanding patient base ensures consistent utilization of dialysis services and stable revenue generation for providers.

Government Healthcare Spending and Vision 2030 Reforms

Healthcare transformation is a core pillar of Saudi Arabia’s Vision 2030 agenda. The government has prioritized expanding access to advanced medical services, upgrading hospital infrastructure, and encouraging private sector participation. Dialysis care has emerged as a high-priority segment due to the rising CKD burden and associated long-term treatment costs.

Through public-private partnerships (PPPs), new dialysis centers are being established, and existing hospitals are being equipped with state-of-the-art machines. The National Center for Privatization plays a key role in regulating healthcare privatization, including outsourcing dialysis services to private operators. By 2030, Saudi Arabia aims for the private sector to deliver nearly 65% of healthcare services, a shift that is expected to significantly boost investments in dialysis infrastructure, equipment, and staffing.

Increased Adoption of Home-Based Dialysis

Home-based dialysis is gaining momentum in Saudi Arabia as patients and healthcare systems seek cost-effective and patient-centric care models. Home hemodialysis and peritoneal dialysis reduce the burden on crowded hospitals, lower transportation costs, and provide patients with greater flexibility and independence.

Technological advancements such as portable dialysis machines, automated PD systems, and remote patient monitoring platforms have made home dialysis safer and more practical. Integration with telemedicine enables clinicians to track patient health in real time, aligning well with the Kingdom’s digital health objectives. Growing awareness and government support are expected to accelerate home dialysis adoption during the forecast period.

Challenges in the Saudi Arabia Dialysis Market

High Treatment Costs and Resource Burden

Dialysis is an expensive, lifelong therapy for most ESRD patients. Costs arise from frequent treatment sessions, expensive consumables, advanced machinery, and specialized staffing requirements. Although government subsidies help reduce patient financial burden, the overall cost pressure on the healthcare system remains substantial.

Private dialysis providers face profitability challenges due to high operational expenses and regulated reimbursement structures. For lower-income patients, access to advanced home dialysis options can remain limited. These economic constraints pose challenges to sustainable long-term expansion, especially as patient volumes continue to rise.

Shortage of Skilled Nephrology Workforce

A persistent shortage of trained nephrologists, dialysis nurses, and technicians represents one of the most critical barriers to market growth. Dialysis requires specialized expertise to ensure patient safety and effective treatment outcomes. Workforce shortages lead to higher patient-to-staff ratios, longer waiting times, and increased strain on existing healthcare professionals.

While large metropolitan areas are relatively better staffed, smaller cities and rural regions face more pronounced shortages. Without significant investments in medical education, training programs, and workforce retention, human resource limitations could constrain service expansion despite rising demand.

Saudi Arabia Hemodialysis Market

Hemodialysis dominates the Saudi dialysis market and accounts for the majority of renal replacement therapy procedures. Its widespread adoption is supported by an extensive network of hospitals and dialysis centers across the Kingdom. Government funding has played a central role in ensuring broad access to HD services.

Although effective, hemodialysis is resource-intensive, requiring substantial infrastructure, staffing, and consumables. Recent interest in home hemodialysis and portable devices is introducing greater flexibility, but in-center HD is expected to remain the cornerstone of renal care due to established clinical familiarity and infrastructure.

Saudi Arabia Dialysis Services Market

Dialysis services form the backbone of the market, encompassing hospital-based treatments, standalone dialysis centers, and home care programs. Public hospitals under the Ministry of Health dominate service delivery, offering subsidized or free dialysis to citizens. Private providers are increasingly expanding in urban regions, focusing on patient comfort and specialized care.

Despite growing capacity, challenges such as long waiting lists and uneven geographic distribution persist. Digital health tools for appointment scheduling and patient monitoring are gradually improving service efficiency. With CKD prevalence rising, dialysis services will remain one of the most essential healthcare offerings in Saudi Arabia.

Saudi Arabia Dialysis Consumables Market

Dialysis consumables—including dialyzers, catheters, bloodlines, and dialysis solutions—are required for every treatment session, making this segment highly stable and recurring. Saudi Arabia currently relies heavily on imports, but efforts to localize manufacturing are gaining traction to reduce supply chain dependency.

Advances in biocompatible materials and sterilization technologies are enhancing patient safety and treatment outcomes. Given the repetitive nature of dialysis, the consumables segment is expected to grow steadily alongside expanding treatment volumes 🔁.

Saudi Arabia Home Dialysis Market

The home dialysis segment is experiencing rapid growth as healthcare policies increasingly favor decentralized care. Patients benefit from reduced hospital visits, improved quality of life, and greater autonomy. Technological innovation and telehealth integration have significantly improved the feasibility of home treatment.

While adoption remains lower than in-center dialysis due to training and awareness limitations, strong policy support and patient preference for convenience are expected to drive robust growth over the coming decade 🏠.

Regional Insights

Dhahran Dialysis Market

Dhahran’s strong industrial base and expatriate population support sustained demand for dialysis services. Well-equipped hospitals and corporate healthcare programs contribute to market expansion, particularly for advanced dialysis technologies.

Jeddah Dialysis Market

As a major urban hub and gateway to Mecca and Medina, Jeddah experiences high patient volumes. The city’s advanced healthcare infrastructure and growing private sector participation position it as one of the largest dialysis markets in the Kingdom.

Dammam Dialysis Market

Dammam is emerging as a key healthcare center in the Eastern Province. Rising lifestyle disease prevalence and ongoing infrastructure investments are driving steady growth in dialysis services and consumables.

Market Segmentation

By Type

Hemodialysis

Peritoneal Dialysis

By Product & Services

Services

Equipment

Consumables

Drugs

By End User

In-Center Dialysis

Home Dialysis

By Region

Dhahran

Riyadh

Khobar

Jeddah

Dammam

Others

Key Players Analysis

The Saudi Arabia dialysis market is supported by global and regional leaders focusing on innovation, partnerships, and service expansion. Major players include:

Asahi Kasei Corporation

B. Braun Melsungen AG

Baxter International Inc.

Becton Dickinson and Company

DaVita Inc.

Fresenius Medical Care AG & Co. KGaA

JMS Co. Ltd.

Medtronic Plc.

Each company is evaluated across five viewpoints: overview, key personnel, recent developments, SWOT analysis, and revenue performance.

Final Thoughts

The Saudi Arabia dialysis market is positioned for sustained and resilient growth through 2033, driven by rising CKD prevalence, strong government backing, and expanding private sector involvement. While challenges such as high treatment costs and workforce shortages persist, ongoing reforms under Vision 2030, technological innovation, and the shift toward home-based care are reshaping the renal care landscape.

As demand for dialysis continues to grow, opportunities will emerge across services, consumables, equipment, and digital health integration—making dialysis a cornerstone of Saudi Arabia’s evolving healthcare economy.

About the Creator

Janine Root

Janine Root is a skilled content writer with a passion for creating engaging, informative, and SEO-optimized content. She excels in crafting compelling narratives that resonate with audiences and drive results.

Keep reading

More stories from Janine Root and writers in Longevity and other communities.

Canada Pharmaceutical Market Size and Forecast 2025–2033

Canada Pharmaceutical Market Outlook (2025–2033) The Canada Pharmaceutical Market is projected to grow steadily, reaching US$ 48.11 billion by 2033, up from US$ 32.88 billion in 2024, expanding at a CAGR of 4.32% from 2025 to 2033, according to estimates aligned with Renub Research. This consistent expansion reflects Canada’s strong healthcare framework, an aging population, rising chronic disease burden, supportive government policies, and a well-established pharmaceutical research and development ecosystem.

By Janine Root 12 days ago in Longevity

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts4 days ago in Longevity

Center Stage with Gina C.

*** I'm keen to republish the interviews I did for my series with Vocal creators. It's been a few years and I thought it might be nice to revisit these wonderful conversations. I'll be releasing them one at a time for a few weeks/months.

By Heather Hubler4 days ago in Interview

Comments

There are no comments for this story

Be the first to respond and start the conversation.