Korea Semiconductor Device Market Size and Forecast 2025–2033

How South Korea Is Powering the Next Era of Global Chip Innovation

South Korea stands at the heart of the global semiconductor revolution. With the world rapidly shifting toward artificial intelligence, 5G networks, electric mobility, automation, and data-driven technologies, the demand for high-performance semiconductors has never been stronger. Unsurprisingly, Korea—home to Samsung Electronics and SK Hynix, the two largest memory chip manufacturers—continues to strengthen its position as a global semiconductor powerhouse.

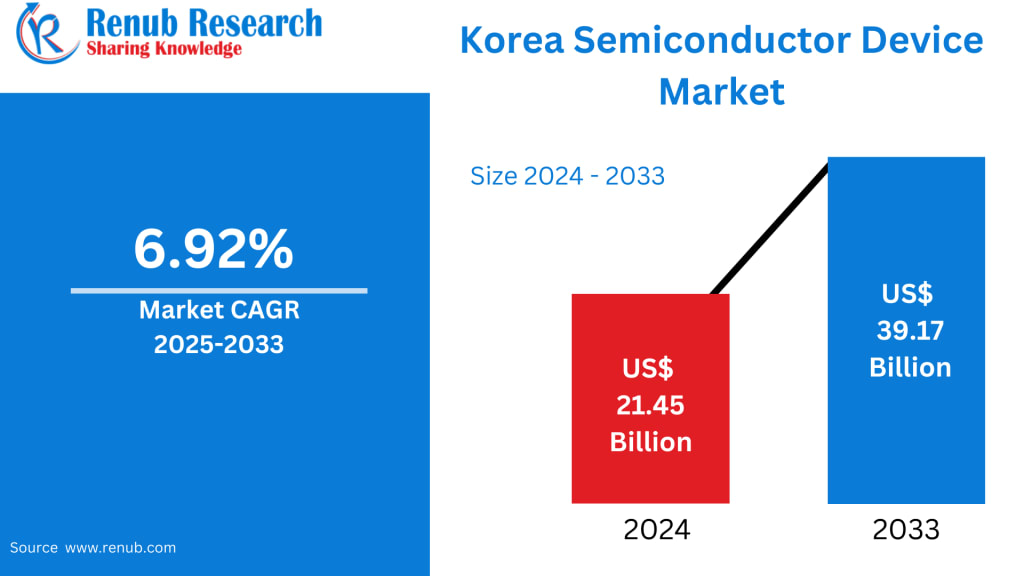

According to Renub Research, the Korea Semiconductor Device Market is expected to reach US$ 39.17 billion by 2033, rising from US$ 21.45 billion in 2024, growing at a CAGR of 6.92% during the forecast period 2025–2033. This impressive growth trajectory is fueled by booming global demand for memory chips, aggressive investments in AI and 5G technologies, and deep government support aimed at retaining Korea’s leadership in advanced chip manufacturing and exports.

Below is a comprehensive, editorial-style deep dive into the industry landscape, its drivers, challenges, segments, and the competitive ecosystem shaping Korea’s semiconductor future.

Korea Semiconductor Device Industry Overview

South Korea occupies a central position in the global semiconductor supply chain, particularly in the memory chip segment. Korean giants Samsung Electronics and SK Hynix are responsible for the majority of the world’s DRAM and NAND flash production—components essential for smartphones, servers, data centers, and consumer electronics.

The semiconductor sector is not just another industry for Korea; it is one of the nation's most critical economic pillars, contributing heavily to exports and GDP. Recognizing this strategic importance, the Korean government has continually supported semiconductor innovation through tax incentives, R&D funding, infrastructure development, and long-term industrial policies.

Recent years have seen the Korean semiconductor industry expand beyond its traditional dominance in memory chips by accelerating investments in logic chips, AI processors, image sensors, automotive-grade semiconductors, and foundry services. As the next wave of global technologies—AI, 5G, autonomous driving, EVs, and high-performance computing—shifts into high gear, Korea is positioning itself to capture maximum value.

However, this progress comes with challenges. Geopolitical tensions, supply chain uncertainty, and intensifying competition from the United States, China, and Taiwan threaten Korea’s leadership. To stay ahead, Korean companies are investing heavily in advanced manufacturing, workforce development, and next-generation chip design.

Even with these headwinds, the Korea Semiconductor Device Market remains a rapidly evolving, innovation-driven sector central to global digital transformation.

Key Factors Driving Korea’s Semiconductor Device Market Growth

1. Surging Global Demand for Memory Chips

Memory chips remain Korea’s strongest competitive edge. As digital technologies expand across industries, demand for high-speed, high-capacity DRAM and NAND flash continues to soar.

Key demand drivers include:

Growth of hyperscale data centers

Rising adoption of AI servers and AI-driven applications

Increasing storage needs in smartphones, laptops, and IoT devices

Expansion of cloud computing, edge computing, and enterprise storage

Samsung and SK Hynix dominate these markets with cutting-edge nodes, superior yield rates, and massive production capacities. As global data generation accelerates, memory chips will remain the backbone of Korea’s semiconductor revenue growth.

2. Strong Government Support and National Semiconductor Strategy

The South Korean government has declared semiconductors a national priority industry, leading to major policy moves such as:

Tax incentives for semiconductor R&D and manufacturing

Subsidies for next-gen chip design and equipment

The “K-Semiconductor Belt” project connecting major chip-making hubs

Support for startups developing AI and automotive chips

University-industry partnerships to expand the skilled workforce

Government backing is essential as countries like the U.S., China, Japan, and EU members intensify investments to localize chip production. Korea’s strategy ensures its domestic ecosystem remains competitive, innovative, and globally relevant.

3. Expansion of Emerging Technologies: AI, 5G, EVs, and IoT

Semiconductors underlie nearly every emerging technology. Korea’s continuous innovation in high-performance chips is helping power:

AI accelerators for machine learning and neural networks

5G/6G network modules

Autonomous and electric vehicle semiconductors

Industrial IoT and smart manufacturing

Advanced sensors and imaging devices

Samsung, for instance, is rapidly expanding its system semiconductor portfolio, focusing on AI-specific processors, mobile SoCs, and foundry services. Korean fabless companies like Rebellions and FuriosaAI are also gaining traction by developing competitive AI chips.

This market diversification ensures Korea’s semiconductor industry is not overly dependent on memory and can thrive in the next decade of digital transformation.

Major Challenges Facing the Korean Semiconductor Industry

1. Geopolitical Risks & Supply Chain Vulnerabilities

Korea’s semiconductor ecosystem is deeply intertwined with global trade dynamics. Political tensions involving the U.S., China, and Japan have previously disrupted supply chains.

Examples include:

Japan’s export restrictions on critical materials such as photoresists and etching gases

U.S.-China chip war affecting demand and tech transfers

Competitive national policies aimed at reshoring chip manufacturing

Korean companies rely heavily on overseas markets for both raw materials and finished product demand. Global uncertainty increases vulnerability. To mitigate risks, Korea is diversifying suppliers, building domestic production of critical materials, and entering strategic international partnerships.

2. Shortage of Semiconductor Talent & R&D Intensity

Despite technological leadership, Korea faces a talent bottleneck in areas such as:

Semiconductor architecture

Advanced manufacturing engineering

Logic chip design

AI and quantum computing hardware

The pace of innovation in next-gen chips requires a constant supply of highly skilled engineers, but universities are not producing talent fast enough. Korea has launched scholarship programs, international collaborations, and specialized training centers, yet the gap remains a concern.

Additionally, as chip nodes shrink and architectures grow more complex, Korean companies face rising R&D costs and pressure to accelerate innovation cycles.

Latest Industry Developments (2025)

Several notable developments highlight Korea’s ongoing momentum:

April 2025: Samsung Electronics announced rapid progress toward maturing its 2 nm process technology and posted Q1 2025 revenue of KRW 79.14 trillion.

April 2025: SK Hynix reported a 157.8% YoY surge in Q1 2025 operating profit to KRW 7.44 trillion, driven largely by booming sales of HBM3E memory for AI servers.

March 2025: Hyundai Mobis partnered with Samsung Foundry to begin mass production of automotive semiconductors in H1 2025.

February 2025: Meta Platforms entered discussions to acquire a Korean AI-chip startup founded by a former Samsung engineer—highlighting Korea’s rising influence in AI chip design.

These developments reinforce Korea’s pivotal role in shaping global semiconductor trends.

Korea Semiconductor Device Market Segmentation

By Product Type

Discrete Semiconductors

Optoelectronics

Sensors

Integrated Circuits (ICs)

Others

Integrated circuits and sensors are witnessing fast adoption due to expanding applications in smart devices, vehicles, and industrial automation.

By Material

Silicon (Si)

Silicon Carbide (SiC)

Gallium Nitride (GaN)

Gallium Arsenide (GaAs)

Others

Materials like SiC and GaN are gaining prominence in EVs, 5G infrastructure, and high-power electronics due to their superior efficiency and thermal conductivity.

By End Use

Networking & Communications

Data Processing

Industrial

Consumer Electronics

Automotive

Government

Networking, data processing, and automotive are expected to be the fastest-growing segments due to the rapid adoption of AI, cloud computing, and EV technologies.

Competitive Landscape: Key Companies Covered

The Korea Semiconductor Device Market features a mix of domestic champions and global leaders shaping industry innovation.

1. Samsung Electronics Co., Ltd.

World’s largest memory chip producer

Expanding 3 nm and 2 nm foundry processes

Innovating in AI chips, image sensors, and mobile SoCs

2. SK Hynix Inc.

Known for industry-leading DRAM and NAND

Major supplier of HBM memory for AI servers

Rapid capacity expansion for next-gen memory

3. Rebellions Inc.

Korean AI chip startup

Develops efficient neural processing units (NPUs)

Gaining global attention for cloud and edge AI solutions

4. FuriosaAI

Focuses on AI accelerators for data centers

Competes with global AI chip players in inference computing

5. Micron Technology Inc.

Strong presence in memory and storage

Competes directly with Samsung and SK Hynix

6. Texas Instruments Inc.

Major supplier of analog semiconductors

Strong automotive and industrial presence

7. ON Semiconductor Corp.

Leading in SiC power devices

Key player in automotive, EV, and IoT semiconductors

8. Infineon Technologies AG

World leader in power electronics

Serves the automotive and industrial sectors

9. STMicroelectronics N.V.

Strong in sensors, microcontrollers, and automotive chips

10. Renesas Electronics Corp.

Key supplier in automotive microcontrollers and SoCs

Each company plays a critical role in shaping Korea’s semiconductor ecosystem through innovation, partnerships, and market expansion strategies.

SWOT Snapshot of Korea’s Semiconductor Industry

Strengths

Global dominance in memory chip production

Strong manufacturing ecosystem

Highly advanced R&D capabilities

Government-backed semiconductor policies

Weaknesses

Heavy reliance on exports

Talent shortages in chip design and advanced manufacturing

Dependence on foreign materials and equipment

Opportunities

Growing demand for AI, 5G, EV, and IoT chips

Expansion into system semiconductors

Rising global strategic investments in chip manufacturing

Threats

Global geopolitical tensions

Escalating competition from China, Taiwan, and the U.S.

Supply chain vulnerabilities

Final Thoughts

South Korea’s semiconductor device market stands at the forefront of global technology transformation. With an expected market size of US$ 39.17 billion by 2033, the industry is well-positioned for sustained growth, driven by booming demand for memory chips, rapid digitalization, and the rise of AI and next-gen technologies.

However, the road ahead is not without obstacles. Navigating geopolitical tensions, securing supply chain resilience, and closing the talent gap will be crucial for Korea to maintain its leadership.

Ultimately, Korea’s combination of technological prowess, strong corporate players, government commitment, and innovation-oriented culture ensures that its semiconductor ecosystem will remain indispensable to the future of global digital infrastructure.

About the Creator

Ben Tom

Ben Tom is a seasoned content writer with 12+ years of experience creating SEO-friendly blogs, web copy, and marketing content that boosts visibility, engages audiences, and drives results.

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts5 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.