IBD Treatment Market Forecast and Size 2025–2033

Biologics, targeted therapies, and digital health reshape a steadily expanding global market

Global IBD Treatment Market: Size, Growth, and the Forces Shaping the Next Decade

The inflammatory bowel disease (IBD) treatment market is on a steady upward trajectory as innovation, awareness, and healthcare access converge across regions. Based on Renub Research estimates, the global IBD treatment market is expected to increase from approximately USD 22.91 billion in 2024 to about USD 33.99 billion by 2033, expanding at a CAGR of 4.48% between 2025 and 2033. This growth reflects the rising prevalence of IBD worldwide, the ongoing shift toward biologics and targeted therapies, and a broader push for early diagnosis and long-term disease management.

IBD encompasses chronic inflammatory disorders of the gastrointestinal tract—primarily Crohn’s disease and ulcerative colitis—that require lifelong treatment. Although no definitive cure exists, modern therapy aims to induce and maintain remission, reduce flare-ups, prevent complications, and improve patients’ quality of life. Over the past two decades, treatment has evolved from symptom-focused regimens to precision medicine that targets specific immune pathways. As emerging markets strengthen healthcare infrastructure and global pharmaceutical companies accelerate R&D, the IBD treatment landscape is becoming more sophisticated, patient-centric, and outcome-driven.

What Is IBD Treatment and Why the Market Matters

IBD treatment refers to a comprehensive set of medical approaches for managing chronic intestinal inflammation. Traditional therapies include aminosalicylates, corticosteroids, and immunosuppressants, while contemporary care increasingly relies on biologics (such as anti-TNF agents, integrin inhibitors, and IL-12/23 blockers) and targeted small molecules (notably JAK inhibitors and newer oral peptides). Adjunctive strategies—nutritional therapy, lifestyle management, microbiome-based interventions, and, when necessary, surgery—remain integral to holistic care.

The market’s importance extends beyond sales figures. IBD is often diagnosed in early adulthood and imposes a lifelong physical, emotional, and economic burden. Rising incidence in urbanizing societies, earlier detection through improved diagnostics, and the expectation of durable remission have elevated demand for advanced therapies. For healthcare systems, this translates into a growing need for cost-effective, long-term treatment solutions that balance efficacy, safety, and accessibility.

Key Growth Drivers

1) Rising Prevalence and Improved Diagnosis

IBD cases are increasing in both developed and emerging economies, influenced by lifestyle changes, dietary patterns, genetic susceptibility, and environmental factors. Expanded screening and specialist access are leading to earlier diagnoses, bringing more patients into long-term care pathways.

2) Biologics and Targeted Therapies

Biologics have transformed IBD management by addressing underlying immune mechanisms rather than only symptoms. The expansion of anti-TNF, anti-integrin, and IL-23 pathway therapies—along with oral targeted agents—is improving remission rates and patient adherence. As biosimilars enter the market, cost pressures may ease, broadening access.

3) Patient-Centric Care and Digital Health

Mobile applications, remote monitoring, and real-world evidence platforms are empowering patients and clinicians to manage symptoms proactively, optimize dosing, and track outcomes. This digital shift supports adherence and long-term disease control.

4) Healthcare Infrastructure in Emerging Markets

Asia-Pacific and parts of Latin America, the Middle East, and Africa are investing in gastroenterology services, specialty clinics, and reimbursement frameworks, accelerating adoption of modern IBD therapies.

Regional Outlook

North America and Europe remain the largest markets, driven by high diagnosis rates, robust reimbursement, and rapid uptake of biologics. Asia-Pacific is the fastest-growing region as urbanization, dietary changes, and improved access to specialists increase both incidence and treatment penetration. Governments and private providers are expanding gastroenterology capacity, making advanced therapies more widely available.

Competitive Landscape: Leading Manufacturers

The IBD treatment market is characterized by strong participation from multinational pharmaceutical companies with deep immunology portfolios, extensive clinical pipelines, and global distribution networks.

Abbott Laboratories (USA)

Founded in 1888, Abbott operates across diagnostics, devices, nutrition, and pharmaceuticals. Its broad healthcare footprint, point-of-care systems, and global distribution make it a significant contributor to gastroenterology and chronic disease management worldwide.

AbbVie Inc. (USA)

Established in 2013, AbbVie is a specialty biopharmaceutical leader with major franchises in immunology, including gastroenterology. With global manufacturing and a strong biologics pipeline, AbbVie’s therapies are widely used in IBD care.

Allergy Therapeutics LLC (UK)

Although best known for allergy vaccines and diagnostics, the company’s immunology expertise and European presence add to the broader ecosystem of immune-modulating therapies relevant to chronic inflammatory diseases.

Bausch Health Companies Inc. (Salix Pharmaceuticals) (Canada)

With a strong focus on gastroenterology, Bausch Health develops and markets branded and generic products for digestive disorders. Its global manufacturing and distribution support broad market reach.

Bristol-Myers Squibb Company (USA)

BMS is a major biopharmaceutical innovator across oncology, immunology, and cardiovascular disease. Its strategic partnerships, global manufacturing, and established brands position it as a key player in immune-mediated conditions, including IBD.

Other influential companies shaping the market include Johnson & Johnson, Novartis AG, Pfizer Inc., Takeda Pharmaceutical Company Limited, GlaxoSmithKline plc, Eli Lilly and Company, Sanofi S.A., Amgen Inc., UCB S.A., F. Hoffmann-La Roche AG, Biogen Inc., Incyte Corporation, and Celgene (now part of BMS). Their combined investments in biologics, small molecules, biosimilars, and patient support programs are redefining treatment standards.

Product Launches and Strategic Moves

Johnson & Johnson (October 2025):

The company reported encouraging Phase 2b results from the ANTHEM-UC study of icotrokinra, a first-in-class oral peptide targeting the IL-23 receptor for moderate-to-severe ulcerative colitis. The data highlighted potential for strong efficacy with a favorable safety profile, underscoring the industry’s shift toward targeted, convenient oral therapies.

Novartis AG (September 2025):

Novartis announced a direct-to-patient platform in the U.S. for Cosentyx® (secukinumab), offering cash-paying patients a significant discount. Although approved across multiple immune-mediated diseases, Cosentyx’s long clinical history and expanding access strategies reflect broader efforts to improve affordability and patient reach for biologics relevant to inflammatory conditions.

SWOT Insights: How Leaders Are Positioning Themselves

GlaxoSmithKline plc (GSK)

Strengths: GSK brings strong pharmaceutical research capabilities, a global brand, and a growing biologics portfolio. Its immunology expertise supports the development of targeted therapies for IBD, while collaborations with academic and biotech partners accelerate innovation. Patient support and affordability initiatives enhance access, particularly in developing markets.

Eli Lilly and Company

Strengths: Lilly’s innovation pipeline, immunology expertise, and biologics leadership provide competitive advantages in IBD. Investments in next-generation monoclonal antibodies and targeted oral agents, combined with real-world evidence and precision medicine approaches, support differentiated outcomes and clinician trust.

These strategic positions reflect a broader industry trend: success in IBD now depends on scientific depth, global scale, patient-centric design, and the ability to demonstrate long-term value to payers and providers.

Recent Developments

Pfizer Inc. (July 2024):

Pfizer’s inflammation and immunology unit continued advancing early-stage research in gastroenterology, acknowledging that while biologics targeting cytokines have transformed care, many patients experience inadequate response or adverse events. This underscores the ongoing need for next-generation therapies with improved safety and durability.

Takeda Pharmaceutical Company Limited (August 2025):

Takeda Biopharmaceuticals India launched the mobile application “For You, With You IBD,” enabling symptom tracking, appointment management, and patient-provider communication. The initiative highlights the rising role of digital tools in chronic disease management and patient empowerment.

Sustainability and Corporate Responsibility

Sustainability is becoming integral to pharmaceutical strategy, including in IBD.

Sanofi S.A. integrates responsible manufacturing, reduced environmental impact, and equitable access into its IBD initiatives. The company emphasizes greener production, renewable energy, waste minimization, and sustainable packaging. In healthcare, Sanofi promotes affordability programs and global partnerships to expand access to biologics while investing in research that improves long-term disease control and reduces healthcare resource intensity.

Amgen Inc. focuses on eco-efficient biologics manufacturing, minimizing water and energy use, and optimizing supply chains with recyclable packaging. By expanding access to both biologics and biosimilars and prioritizing personalized medicine for long-term remission, Amgen aligns environmental stewardship with patient outcomes.

These approaches signal a broader shift: innovation in IBD must be responsible, inclusive, and sustainable to meet the expectations of regulators, payers, and patients.

Market Segmentation and Structure

The IBD treatment market can be viewed across several key dimensions:

By Disease Type: Crohn’s disease, Ulcerative colitis

By Drug Class: Aminosalicylates, Corticosteroids, Immunosuppressants, Biologics, Targeted small molecules

By Route of Administration: Oral, Injectable/Infusion

By Distribution Channel: Hospital pharmacies, Retail pharmacies, Online/specialty pharmacies

By Geography: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

Within this structure, biologics and targeted therapies are gaining share due to superior efficacy and durability, while oral agents are improving patient convenience and adherence.

Market Share and Company Profiles

Leading companies—Abbott Laboratories, AbbVie Inc., Allergan Therapeutics LLC, Bausch Health Companies Inc., Bristol-Myers Squibb Company, Johnson & Johnson, Novartis AG, Pfizer Inc., Takeda, GSK, Eli Lilly, Sanofi, Amgen, UCB, Roche, Biogen, Incyte, and Celgene (BMS)—operate across research, manufacturing, and commercialization. Their strategies commonly include:

Mergers & Acquisitions: Strengthening pipelines and geographic reach

Partnerships: Co-development, licensing, and joint ventures

Investments: Biologics capacity, digital health, and real-world evidence

Sustainability Initiatives: Renewable energy, efficient infrastructure, water conservation, waste reduction

Product Strategy: Portfolio benchmarking, pipeline expansion, and quality standards

These elements collectively shape competitive advantage in a market where innovation cycles are rapid and regulatory expectations are high.

Forecast Analysis: 2025–2033

Renub Research projects a measured but reliable expansion for IBD treatment, with the market reaching USD 33.99 billion by 2033. Growth will be driven by:

Continued adoption of biologics and targeted therapies

Rising disease prevalence and earlier diagnosis

Biosimilars improving affordability and access

Digital health integration enhancing patient engagement

Expansion in Asia-Pacific and other emerging regions

While cost containment and reimbursement scrutiny will persist, the value proposition of therapies that reduce hospitalizations, surgeries, and productivity losses will support sustained investment.

Challenges to Watch

High Treatment Costs: Biologics remain expensive, limiting access in cost-sensitive markets.

Variable Patient Response: Loss of response and adverse events necessitate ongoing innovation.

Regulatory Complexity: Global approvals and pharmacovigilance requirements extend development timelines.

Market Competition: A crowded pipeline intensifies the need for differentiation through outcomes and real-world evidence.

Final Thoughts

The IBD treatment market is entering a new phase—one defined not just by growth, but by transformation. As biologics mature, targeted oral therapies emerge, and digital tools reshape patient engagement, care is becoming more precise, accessible, and sustainable. With Renub Research forecasting a rise from USD 22.91 billion in 2024 to USD 33.99 billion by 2033, the decade ahead will reward companies that combine scientific excellence with affordability, environmental responsibility, and patient-centric design.

For healthcare providers, policymakers, and investors alike, the message is clear: IBD treatment is no longer solely about managing symptoms—it is about delivering durable remission, improving quality of life, and building a healthcare ecosystem that can support millions living with chronic inflammatory disease.

About the Creator

Marthan Sir

Educator with 30+ years of teaching experience | Passionate about sharing knowledge, life lessons & insights | Writing to inspire, inform, and empower readers.

Keep reading

More stories from Marthan Sir and writers in Longevity and other communities.

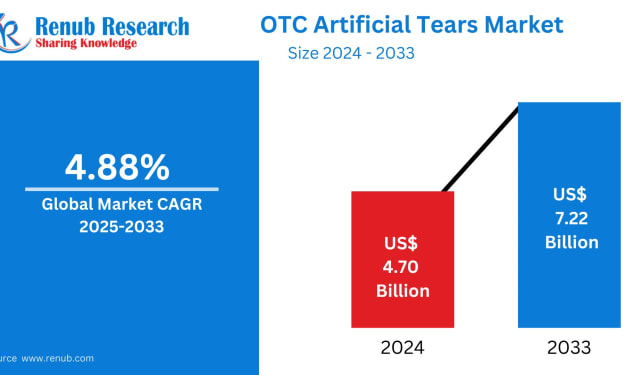

Global OTC Artificial Tears Market Size and Forecast, 2025–2033

Introduction The global healthcare landscape is undergoing a rapid transformation driven by self-care, accessibility, and consumer empowerment. Among the many over-the-counter (OTC) product categories gaining traction, artificial tears stand out as one of the fastest-growing segments within ophthalmic care. Once regarded as a simple comfort product, artificial tears are now central to everyday eye health routines for millions of people worldwide.

By Marthan Sir3 days ago in Longevity

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts10 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.