Global Smart Pills Market Size and Forecast 2025–2033

How Digital Therapeutics, Remote Monitoring, and Capsule Endoscopy Are Redefining Modern Healthcare

The global smart pills market is entering a transformative decade as digital therapeutics, remote patient monitoring, and non-invasive diagnostics align with the healthcare sector’s shift toward precision medicine. According to Renub Research, the Smart Pills Market is expected to grow from US$ 5.07 billion in 2024 to US$ 15.05 billion by 2033, delivering a CAGR of 12.85% between 2025 and 2033.

This remarkable trajectory is powered by a growing geriatric population, rising chronic disease rates, rapid advances in microelectronics, and the medical community’s expanding reliance on minimally invasive technologies. As healthcare systems worldwide embrace patient-centric models, smart pills are emerging as a cutting-edge solution that blends medicine, sensors, and digital data—even redefining what a “pill” can be.

What Are Smart Pills? A Modern Definition

Smart pills—also known as digital pills—are ingestible electronic devices embedded into capsule-sized forms. Once swallowed, these micro-devices transmit wireless data to external receivers such as tablets, smartphones, or biosensor patches. They can help accomplish three critical goals:

Diagnose gastrointestinal (GI) illnesses

Monitor physiological parameters

Track medication adherence

Early innovations largely focused on GI imaging, but the field has advanced toward drug delivery systems, real-time health monitoring, and personalized medicine.

By enabling physicians to remotely monitor medication usage patterns, smart pills help combat prescription non-adherence—one of the most costly challenges in healthcare. Their precision, convenience, and minimally invasive nature make them especially valuable in gastroenterology, chronic disease management, and elderly care.

In 2024, PillSafe showcased the sector’s momentum by launching a smart pill bottle designed to curb medication misuse, signaling how the industry is expanding beyond diagnostics to broader digital health ecosystems.

Market Growth Drivers

1. Advancements in Miniature Electronics and Wireless Technology

Continuous innovation in sensors, microchips, wireless modules, and integrated circuits has significantly strengthened the smart pills market. Modern devices are more compact, easier to ingest, more reliable, and less expensive to manufacture. This is essential for patient comfort—especially for the elderly or those who resist invasive diagnostic methods.

Component miniaturization also improves battery life, data precision, and overall diagnostic accuracy. As technology improves, smart pills become increasingly accessible and affordable, speeding the shift from traditional endoscopy systems toward capsule-based diagnostics.

2. Rising Demand for Innovative Drug Delivery and Personalized Medicine

Pharmaceutical firms are heavily investing in smart pill technologies as they seek targeted, efficient drug delivery systems. Smart pills allow medication to be delivered directly to affected biological sites, reducing side effects and enhancing therapeutic outcomes.

In clinical trials, their real-time data capabilities help researchers track:

Drug absorption

Patient response

Bioavailability

This can accelerate the development of next-generation therapies, particularly for chronic and GI-related conditions.

3. Chronic Disease Burden and Global Aging Trends

Chronic illnesses such as diabetes, hypertension, obesity, inflammatory bowel disease, and cardiovascular disorders are rising worldwide. Elderly patients—who represent the fastest-growing demographics globally—often struggle with medication adherence and regular monitoring.

Smart pills fill these gaps by providing:

Real-time data

Remote monitoring ability

Non-invasive disease management

For geriatric populations, the convenience and simplicity of ingestible monitoring systems reduce hospital visits and improve continuity of care.

Challenges Hindering Smart Pills Market Adoption

1. Integration With Healthcare IT Systems

Smart pills generate vast amounts of data including biometrics, adherence patterns, and GI imagery. However, healthcare systems use fragmented electronic health records (EHRs) and incompatible data formats.

This leads to:

Interoperability issues

Delayed clinical decision-making

Complications in data interpretation

For smart pills to be fully integrated into mainstream clinical workflows, healthcare networks must modernize their digital infrastructure and adopt standardized data protocols.

2. Stringent Global Regulatory Frameworks

Smart pills are regulated as medical devices, diagnostic tools, or drug-delivery systems, making them subject to rigorous approval timelines from agencies like:

US FDA

European Medicines Agency (EMA)

Health Canada

Manufacturers face lengthy, costly processes to prove safety, efficacy, cybersecurity protection, and clinical accuracy. Mental health medication tracking or GI capsules require different validation routes, further complicating the regulatory landscape.

Key Market Segments

1. By Application

Capsule Endoscopy (expected to lead due to non-invasive GI diagnostics)

Patient Monitoring

Drug Delivery

Capsule Endoscopy: The Future Front-Runner

Patients prefer capsule endoscopy because it avoids sedation, reduces discomfort, and provides high-resolution imaging of the GI tract. Its ability to detect lesions, tumors, bleeding sources, and inflammatory patterns makes it a crucial smart pill category.

2. By Target Area

Esophagus (projected to grow into a major segment)

Small Intestine

Large Intestine

Stomach

Smart pills used in the esophageal region are especially promising, helping diagnose GERD, esophagitis, and Barrett’s esophagus—conditions affecting millions worldwide.

3. By End-User

Diagnostic Centers (expected to dominate)

Hospitals

Research Institutes

Others

Diagnostic centers are increasingly using smart pill technology to enhance efficiency, improve diagnostic accuracy, and provide less invasive patient experiences.

Regional Market Insights

The global smart pills market spans major regions including:

North America (United States, Canada)

Europe (France, Germany, Italy, Spain, UK, Turkey, Belgium, Netherlands)

Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Thailand, Malaysia, New Zealand)

Latin America (Brazil, Mexico, Argentina)

Middle East & Africa (Saudi Arabia, UAE, South Africa)

United States: The Global Leader

The U.S. dominates the smart pills market due to:

Strong biotechnology ecosystem

High chronic disease prevalence

Robust digital health innovation

Favorable FDA policies

Smart pills are increasingly used for medication adherence tracking, capsule endoscopy, and remote monitoring, especially among aging populations.

A notable advancement was AnX Robotica Corp.’s NaviCam Small Bowel System launched in February 2023, which improved diagnostic precision through spherical lens technology.

Germany: Europe’s Smart Pills Powerhouse

Germany benefits from:

A well-developed healthcare system

High adoption of medical technology

Strong pharmaceutical leadership

Smart pills are increasingly integrated in German diagnostic centers and hospitals for managing GI disorders and chronic diseases. Regulatory complexities and reimbursement challenges remain, but innovation continues to drive adoption.

India: A Rapidly Emerging Market

With rising chronic disease rates and a push toward digital healthcare, India is witnessing accelerated adoption of smart pills. Key drivers include:

A large population base

Growing private healthcare investment

Advancements in capsule endoscopy

Challenges include affordability barriers and limited awareness, but collaboration between India’s tech and pharma sectors could make the country a global smart pill innovation hub.

Saudi Arabia: A Vision 2030 Healthcare Transformation

Saudi Arabia’s healthcare modernization efforts promote early adoption of advanced digital health tools, including smart pills. Benefits include:

Improved remote monitoring

Better chronic disease management

Enhanced diagnostic accuracy

High implementation costs and regulatory guidelines are obstacles, but investment in digital health continues to rise.

Smart Pills Market Segmentation Summary

Application

Capsule Endoscopy

Patient Monitoring

Drug Delivery

Target Area

Esophagus

Small Intestine

Large Intestine

Stomach

End-Users

Diagnostic Centers

Hospitals

Research Institutes

Others

Regional Coverage

North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Key Companies Covered

Check-Cap Ltd.

General Electric Company

Fujifilm

Koninklijke Philips N.V.

Medtronic plc

Olympus Corporation

Novartis AG

Otsuka Holdings Co., Ltd.

Each company demonstrates strong capabilities in medical imaging, miniature electronics, or pharmaceutical innovation—making them essential contributors to the future of smart pill technologies.

Final Thoughts: Smart Pills and the Digital Future of Healthcare

Smart pills represent one of the most exciting intersections of medicine, digital health, and microelectronics. As healthcare systems transition toward remote monitoring, precision therapy, and minimally invasive diagnostics, smart pills will unlock new pathways to manage diseases earlier, faster, and more accurately.

Despite challenges surrounding regulation, cost, and data integration, their long-term potential is undeniable. By 2033, with a projected market value of US$ 15.05 billion, smart pills are set to redefine global healthcare—not just as diagnostic tools, but as essential components of the world's digital medicine ecosystem.

About the Creator

Keep reading

More stories from Aaina Oberoi and writers in Longevity and other communities.

Telemedicine Market Size and Forecast 2025–2033

Telemedicine is no longer an emerging technology—it is becoming the backbone of modern healthcare delivery. According to Renub Research, the global telemedicine market is expected to reach US$ 618.34 billion by 2033, rising dramatically from US$ 83.23 billion in 2024, with a powerful CAGR of 24.96% during 2025–2033. This extraordinary rise reflects the accelerating global shift toward digital healthcare, powered by better connectivity, remote monitoring tools, and the growing demand for accessible, cost-effective medical services.

By Aaina Oberoiabout a month ago in Longevity

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts11 days ago in Longevity

Collectibles Market Size and Forecast 2025–2033

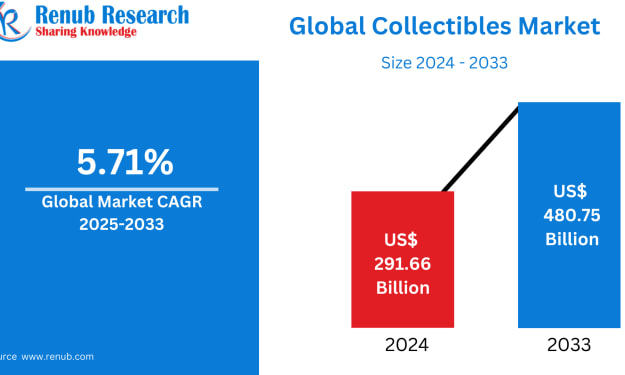

Collectibles Market Outlook 2025–2033 The global Collectibles Market is expected to reach US$ 480.75 billion by 2033, expanding from US$ 291.66 billion in 2024, at a CAGR of 5.71% from 2025 to 2033. This steady rise reflects a powerful convergence of emotional value, investment potential, and technological innovation. From fine art and rare coins to trading cards, pop culture memorabilia, and digital collectibles, the industry continues to broaden its appeal across age groups, geographies, and income levels.

By Renub Research5 days ago in Longevity

The Devil's Cut

“Comrade, finally you’re awake.” The voice was smooth, sensual. A flickering incandescent bar was all that lit the white, sterile room. All Vladimir remembered was everything going black. He tried to move his arms and found them strapped to the gurney.

By Matthew J. Fromm4 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.