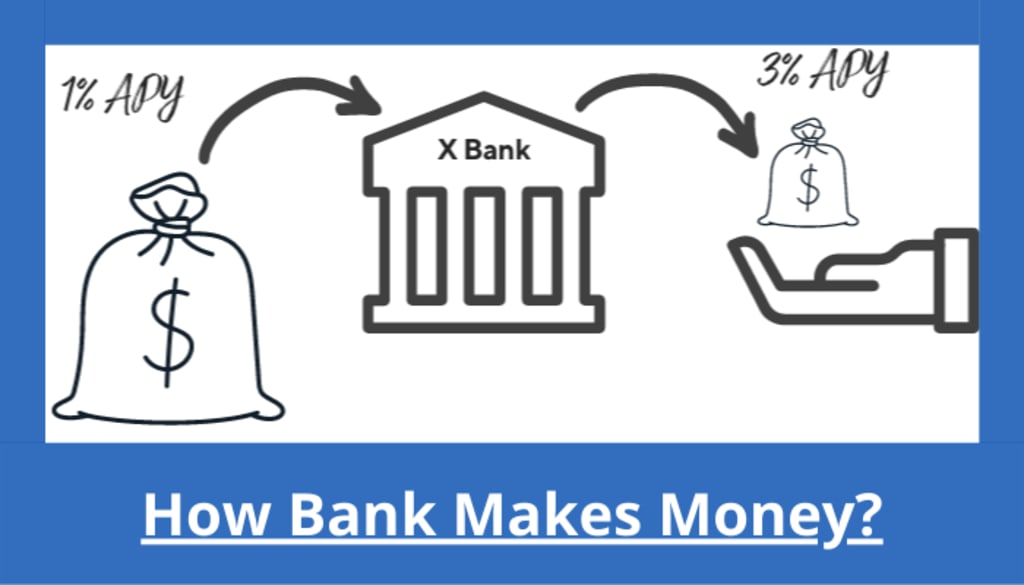

Interest income:

Interest income is one of the primary ways that banks generate revenue. Banks end money to customers, such as individuals or businesses, and charge them interes ton the loans. The interest rate they charge is typically higher than the interest rate they pay to depositors, allowing them to make a profit on the difference between the two rates.

For example, if a bank offers a personal loan with an interest rate of 6%, and the bank's cost of funds (the interest rate it pays to depositors) is 2%, the bank earns anet interest income of 4% on the loan. The bank can then use this income to pay for its operating expenses and earn a profit for its shareholders.Interest income can come from a variety of sources, including mortgages, car loans, personal loans, and commercial loans. The interest rates charged on these loans may vary depending on factors such as the credit worthiness of the borrower, the length of the loan, and the type of collateral used to secure the loan.

Overall, interest income is a critical component of a bank's revenue stream and profitability, and banks must carefully manage their lending practices to balance risk and return

Fees:

In addition to interest income, banks also generate revenue by charging fees for various services. These fees can be an essential source of income for banks, especially in a low-interest-rate environment.

Here are some examples of fees that banks commonly charge:

*ATM fees:

Many banks charge fees for using an ATM that is not part of their network.These fees can range from a few dollars to more than $5 per transaction.

*Account maintenance fees:

Some banks charge fees for maintaining a checking or savings account.These fees may be waived if the customer maintains a minimum balance or meets other requirements.

*Overdraft fees:

Banks charge fees when a customer overdrafts their account, meaning they spend more money than they have available. These fees can be significant, ranging from $20 to $35 per overdraft.

*Transaction fees:

Banks may charge fees for certain types of transactions, such as wire transfers or foreign currency exchanges.

*Late payment fees:

Banks may charge fees if a customer is late on a loan or credit card payment.

*Annual fees:

Credit cards often come with annual fees, which can range from a few dollars to several hundred dollars, depending on the card's features and benefits.

*wire transfer fees:

Wire transfer fees are charges levied by banks or other financial institutions for processing wire transfer transactions. Wire transfers are a secure and fast way to transfer funds from one bank account to another, either within the same country or across international borders.

*Asset management fees:

Asset management fees are fees that banks charge for managing assets on behalf of their customers. Asset management is the process of managing and investing funds on behalf of individuals, corporations, and institutional investors to achieve specific investment objectives.

Investments:

Banks also generate revenue through investments, which can include a wide range of financial instruments such as stocks, bonds, and mutual funds. Banks invest money in various ways to generate a return on their capital, and these investments can be an essential source of income for the bank.

Here are some examples of investments that banks may make:

*Treasury securities:

Banks may invest in U.S. Treasury securities, which are issued by the federal government and considered to be one of the safest investments available.

*Corporate bonds:

Banks may invest in corporate bonds, which are issued by companies and offer higher returns than Treasury securities but come with more risk.

*Mutual funds:

Banks may offer mutual funds to their customers, which pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets.

*Real estate:

Banks may invest in real estate, either through direct ownership of properties or through real estate investment trusts (REITs).

*Private equity:

Banks may invest in private equity funds, which invest in privately held companies and aim to generate high returns over the long term.The returns from these investments can vary depending on marketconditions and the performance of the underlying assets. Banks must carefully manage their investment portfolios to balance risk and return and ensure that they are generating a sufficient return on their capital while also maintaining adequate levels of liquidity and capitalization.

Overall, investments can be an important source of income for banks, but they can also be a source of risk if not managed properly. Banks must carefully evaluate their investment decisions and maintain a diversified portfolio to minimize risk and maximize returns.

Trading:

Trading is another way that banks generate revenue. Banks engage in trading activities by buying and selling financial instruments such as stocks, bonds, currencies,and commodities. Trading can be a highly profitable business for banks, but it can also be risky, and banks must have sophisticated risk management systems in place to manage their exposure to market fluctuations.

Here are some examples of trading activities that banks may engage in:

*Currency trading:

Banks may buy and sell currencies to take advantage of fluctuations inexchange rates. Currency trading can be highly profitable but also carries significan trisk due to the volatility of the foreign exchange markets.

*Fixed-income trading:

Banks may buy and sell bonds and other fixed-income securities to generate returns on their capital. Fixed-income trading can be less volatile than other forms of trading but still carries risk due to changes in interest rates and credit risk.

*Equity trading:

Banks may buy and sell stocks and other equity securities on behalf of their clients or for their own account. Equity trading can be highly profitable but also carries significant risk due to market volatility.

*Commodities trading:

Banks may buy and sell commodities such as oil, gold, and agricultural products to generate returns on their capital. Commodities trading can be highly profitable but also carries significant risk due to changes in supply and demand and geopolitical factors.

Overall, trading can be an essential source of income for banks, but it can also be a source of risk. Banks must carefully manage their trading activities to ensure that they are generating sufficient returns while also maintaining adequate levels of risk management and capitalization.

Credit card interest:

Credit card interest is another way that banks generate revenue. When customers use their credit cards to make purchases, they are essentially borrowing money from the bank. If the customer does not pay off their balance in full each month,they will be charged interest on the unpaid balance.

The interest rate on credit card balances can be quite high, typically ranging from 15% to 25% or more, depending on the creditworthiness of the customer and other factors. This high interest rate can generate significant revenue for banks, especially if the customer carries a balance for an extended period.In addition to interest on balances, banks may also charge fees for credit card transactions, such as balance transfer fees, cash advance fees, and late payment fees.These fees can add up quickly and provide another source of revenue for banks.

Credit cards can be a lucrative business for banks, but they also carry risks,such as credit risk and fraud risk. Banks must carefully manage their credit card portfolios to balance risk and return and ensure that they are generating sufficient revenue while also maintaining a high level of customer satisfaction.

Foreign exchange transactions:

Foreign exchange transactions refer to the process of buying and selling foreign currencies. Banks play a crucial role in facilitating foreign exchange transactions between individuals, businesses, and governments.

Banks earn money from foreign exchange transactions by charging a spread, which is the difference between the buying and selling price of a currency. For example, if the bank buys US dollars at a rate of 1.20 euros per dollar and sells them at a rate of 1.25 euros per dollar, the spread is 0.05 euros per dollar. The bank earns this spread as its commission for facilitating the transaction.

Banks also earn revenue from foreign exchange transactions by charging fees for services such as wire transfers, currency exchange, and foreign currency accounts. These fees vary depending on the type of transaction and the amount of money involved.

Foreign exchange transactions are essential for businesses and individuals engaged in international trade, tourism, and investment. Banks' ability to provide reliable and efficient foreign exchange services is critical to facilitating global commerce and maintaining international financial stability.

About the Creator

Keep reading

More stories from george orwell and writers in Lifehack and other communities.

Advantage and Disadvantage of ChatGPT

Advantages of ChatGPT: *Ability to understand natural language: ~ChatGPT is a language model that has been trained on vast amounts of text data from the internet, including books, articles, and websites. This training enables it to understand natural language and generate responses in a conversational manner. By processing and analyzing the text data, ChatGPT learns to recognize patterns in language, including syntax, grammar, and context, which helps it to understand the meaning behind the words and generate relevant responses. This ability to understand natural language is what makes ChatGPT useful for a wide range of applications, including customer service, chatbots, and personal assistants

By george orwell3 years ago in Lifehack

How to Get Promoted in a Remote Job

Remote work changed how we get hired. It also changed how we get promoted. In a traditional office, visibility is automatic. You’re seen walking in early. You’re seen staying late. You’re in meetings. You’re in the hallway conversations.

By Bahati Mulishi7 days ago in Lifehack

Comments

There are no comments for this story

Be the first to respond and start the conversation.