Why Cross-Border Payments Fail – And How Small Businesses Can Fix the “Last-Mile” Problem

A practical guide for SMBs to simplify international payments

International business should be faster than ever. With digital banking and fintech platforms on the rise, you’d expect cross-border transactions to clear instantly. Yet for many small and medium-sized businesses (SMBs), sending money abroad is still frustratingly slow, costly, and unpredictable.

From delayed wires to declined transactions, the barriers are real. But understanding why payments fail—and learning how to choose the right payment solution—can help turn these challenges into opportunities. Understanding these pitfalls and choosing the right tool can transform fast international payments.

The “Last-Mile” Problem in Global Payments

When you hit “send” on a wire transfer, you expect the funds to reach your supplier or contractor quickly. But in reality, that final step—the so-called last mile—is where things often break down.

Even though systems like SWIFT suggest that wholesale transfers can settle in under an hour, many SMBs still face delays. Local banks batch payments, hold them until the next business day, or apply extra compliance checks. On top of that, mismatched banking systems and currency controls slow things further.

For a small business, every extra day can mean stalled shipments, strained vendor relationships, and disrupted cash flow.

Declines and Disputes: The Hidden Drain on Cash Flow

Cross-border payments are far more likely to be declined than domestic ones. Sometimes the reason is as simple as mismatched data fields or formatting errors. Other times, banks flag activity as suspicious.

Even if funds make it through, another challenge lurks: chargebacks and disputes. “Friendly fraud”—when customers wrongly dispute legitimate charges—can lock up your money for weeks. For an SMB already operating on thin margins, this can be devastating.

Regulatory Complexity: Barrier or Benefit?

Paying globally also means navigating a maze of compliance rules: OFAC sanction lists, GDPR, anti-money-laundering (AML) checks, and local currency regulations.

At first glance, this feels like red tape that slows business. But in reality, strong compliance systems protect your business from fraud and penalties. The problem is that many SMBs don’t have the resources to manage compliance in-house. That’s where modern fintech platforms can step in.

What to Look For in a Payment Platform

Not all international payment providers are created equal. If you’re evaluating your options, here are a few must-have features:

Speed: Same-day (or faster) settlements without requiring pre-funding.

Transparency: No hidden FX markups or surprise fees.

Security: Fraud monitoring, two-factor authentication, and strong compliance certifications.

Flexibility: Support for multiple currencies and payment methods.

Integration: A unified dashboard that brings wires, ACH, checks, and cards together.

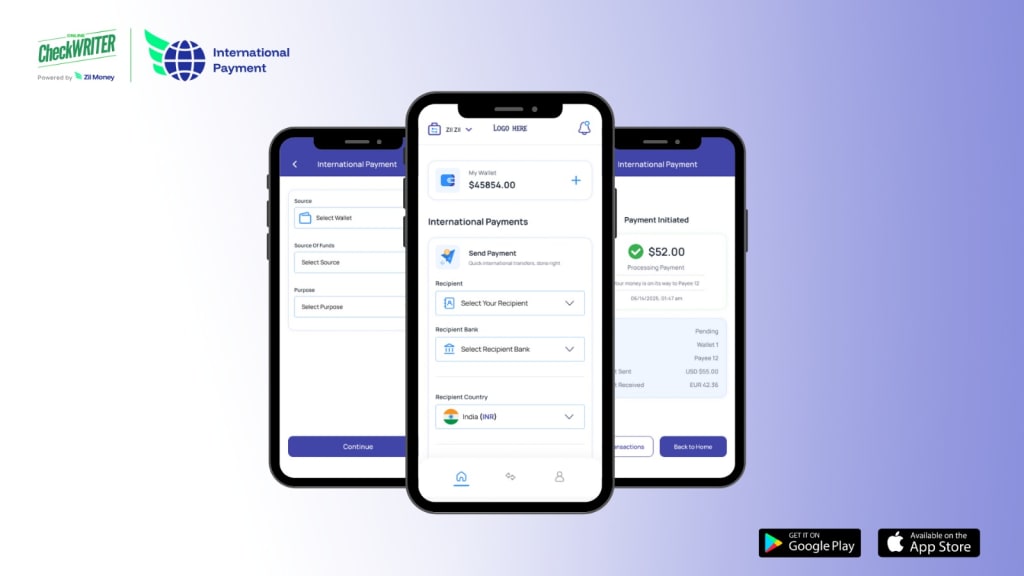

A Modern Solution: OnlineCheckWriter.com – Powered by Zil Money

One platform that has gained traction among SMBs is OnlineCheckWriter.com – Powered by Zil Money. Unlike traditional banks that rely heavily on correspondent networks, this solution uses a direct wallet-to-bank model to cut out unnecessary middlemen.

Fast settlement: Payments can clear in minutes—sometimes as fast as 90 seconds—without pre-funded accounts.

Transparent pricing: What you send is what your supplier receives. No hidden fees.

Multi-currency support: Pay in local currencies using live exchange rates.

Robust security: SOC 1, SOC 2, PCI DSS, and ISO certifications, plus real-time fraud monitoring.

Proven reliability: Over one million businesses and $100 billion in processed payments speak to its scale.

For SMBs struggling with last-mile issues, this kind of all-in-one platform can simplify global payments dramatically.

Quick Checklist for SMB Owners

If you’re still comparing options, here’s a simple decision-making framework:

Map your pain points (delays, fees, compliance, fraud).

Compare settlement times across providers.

Review pricing and exchange rate transparency.

Check compliance and fraud protections.

Look for scalability as your international business grows.

Final Thoughts: Turning Barriers Into Bridges

Cross-border payments don’t have to be a headache. Yes, challenges like last-mile delays, declines, and compliance hurdles exist—but they’re not insurmountable.

By understanding why payments fail and choosing a provider built to solve these issues, small businesses can transform global transactions into a competitive advantage.

Platforms like OnlineCheckWriter.com – Powered by Zil Money show that international payments can be as smooth as domestic ones. For SMBs with global ambitions, that’s not just convenient—it’s essential.

About the Creator

Arish

hi my name is arish i am experienced in creating stories and make a good content for you

Copper 2025: The $Trillion Energy Pivot

The future hums quietly. It runs through electric vehicle batteries, renewable power grids, and the wires inside your walls. And at the center of it all? Copper. As countries race toward decarbonization, the Copper Market is becoming the backbone of energy transformation. Demand is no longer industrial-it’s existential.

By efingutthomas7 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.