The Impact of Russia's Sanctions Removal on Global Oil & Gas Markets

Unpacking the Impact of Sanctions Removal

The Economic Ripple: Unpacking the Impact of Sanctions Removal on Global Oil & Gas Markets

I. Introduction: The Geopolitical Nexus of Sanctions and Energy

After Russia invaded Ukraine in February 2022, Western nations imposed broad sanctions and export controls to reduce Russia's energy revenues and limit its access to global financial systems and technology. As a major global energy producer with vast reserves and infrastructure, Russia's dominant role in oil and natural gas markets meant these sanctions had far-reaching effects on international energy trade, prices, and security, particularly in Europe. This article analyzes how removing sanctions on Russia would impact global oil and gas markets, examining effects on producers, consumers, and geopolitical relationships through market data and expert analysis. Understanding these dynamics is vital for stakeholders navigating the evolving energy landscape.

II. Russia's Pivotal Role in Global Oil & Gas: The Pre-Sanction Landscape (2021)

Before the comprehensive sanctions imposed in 2022, Russia held an indispensable position in the global oil and gas markets, acting as a major supplier that profoundly influenced international energy dynamics.

Oil Market Dominance

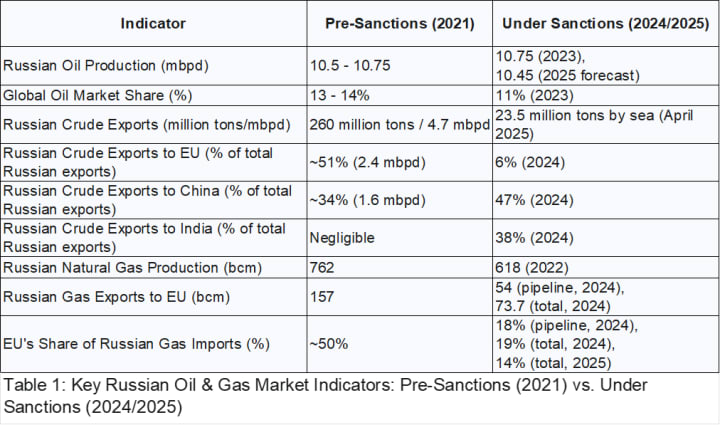

In 2021, Russia was a major force in global oil, producing 10.5 million barrels per day (14% of the world supply). Despite sanctions by 2023, it maintained its position as the third-largest producer at 10.75 million bpd (11% globally), remaining crucial to energy markets. Russia exported 4.7 million bpd of crude oil in 2021, mainly to Europe (2.4 million bpd) and China (1.6 million bpd). With 6.9 million bpd refining capacity, it also supplied 2.8 million bpd of oil products, including European diesel (750,000 bpd).

Natural Gas Powerhouse

Russia led global natural gas with vast reserves (1,600 tcm) and production (762 bcm in 2021), with Gazprom controlling 68%. Russia provided 50% of EU gas imports (157 bcm) in 2021 via major pipelines and LNG, giving it significant leverage over European energy security. As the 4th largest LNG exporter (40 bcm, 8% globally) in 2021, Russia planned expansion to 110-190 bcm/year by 2025.

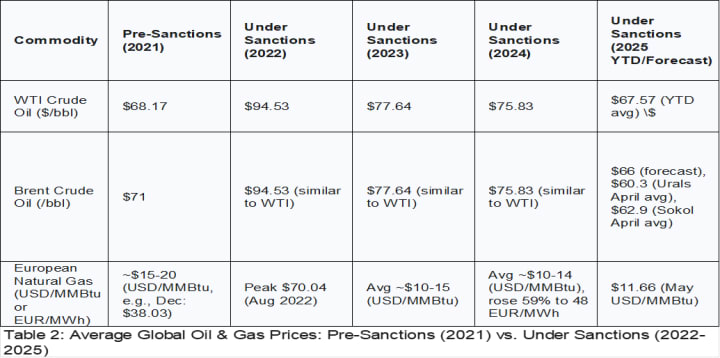

Comparative Statistics: Pre-Sanctions (2021) vs. Under Sanctions (2024/2025)

The following tables provide a quantitative overview of Russia's energy market position and global energy prices before and after the imposition of sanctions. These comparisons are fundamental to understanding the market recalibration that has occurred and the potential impacts of sanctions removal.

Market data shows dramatic price shifts after sanctions. WTI crude rose from $68.17/bbl in 2021 to $94.53/bbl in 2022, while European natural gas jumped from $15-20 USD/MMBtu to $70.04 USD/MMBtu in August 2022. Though prices have since declined, they remain elevated, reflecting a "sanctions premium" and fundamental market transformation that would be complex to reverse.

III. The Current State: Global Oil & Gas Markets Under Sanctions (2022-2025)

The period since February 2022 has witnessed a profound restructuring of global oil and gas markets, driven by the imposition of sanctions on Russia. This section details the significant shifts in trade flows, the emergence of new market mechanisms, and the financial implications for Russia and the wider global economy.

Impact on Russian Oil Exports

Russian oil exports shifted from Europe to Asia, with China and India now buying 85% of exports, while EU imports fell to 6%. This created longer shipping routes between markets. To bypass sanctions, Russia assembled a fleet of 343 tankers, including 135 'shadow' vessels, though many raise safety concerns. The G7's $60/barrel price cap had minimal effect, as Urals crude traded below this level and Russia found alternative routes through re-exports. While sanctions redirected rather than halted exports, they created an inefficient parallel market. The Dallas Fed found shipping costs, not price restrictions, drove crude discounts. The price cap mainly served political purposes for the EU.

Impact on Russian Natural Gas Exports

Russian gas imports to the EU fell from 157 bcm in 2021 to 54 bcm by 2024 (18% of EU imports), with pipeline transit now limited to TurkStream after Ukraine transit ended in December 2024. Paradoxically, while pipeline gas decreased, EU imports of Russian LNG rose 60% over three years, reaching 70% of Russian LNG exports and 17% of EU LNG imports in 2024. France and the Netherlands increased their Russian LNG imports significantly. Europe has diversified its gas supply, with the US becoming a key supplier and Germany building new LNG facilities. However, this transition has been costly, with European countries spending 1-7% of GDP to protect consumers and build infrastructure. This mixed approach - reducing pipeline gas while increasing LNG imports - reflects the tension between political goals and market realities. Lifting sanctions could reverse these changes, potentially undermining Europe's investments in alternative supply infrastructure.

Global Market Restructuring

Sanctions have transformed oil trade routes globally, lengthening shipping distances. US exports to Europe increased while India shifted away from US oil to Russian supplies. Higher shipping costs drove half of Russia's crude price discounts. Russia's fossil fuel revenues declined significantly, with daily revenues falling 6% and oil tax revenue down 28%. Despite $150 billion in losses over three years, Russia adapted through wartime measures and Asian trade. This reshaping of energy logistics appears permanent. While creating opportunities for US LNG exporters and Indian refiners, removing sanctions would disrupt the new market structure and risk EU and US infrastructure investments.

IV. Positive Economic Impacts of Sanctions Removal

The removal of sanctions on Russia would undoubtedly trigger a series of positive economic impacts on the global oil and gas market, primarily driven by increased supply, enhanced market efficiency, and subsequent benefits for consumers and industries.

Increased Global Supply and Potential Price Reduction

Lifting sanctions would allow Russian oil and gas to return to traditional markets, increasing global supply. As the world's third-largest oil producer at 10.75 million bpd, Russia's reentry would significantly boost market volumes. Goldman Sachs projects Russia's GDP could grow 2.5% annually post-sanctions (versus -1.5% currently) through increased hydrocarbon sales. The removal of restrictions would lower global energy prices. European markets would see immediate price reductions as Russian pipeline gas returns, while reduced logistics costs would benefit consumers and industries globally.

Restoration of Market Efficiency and Trade Routes

Sanctions have created market inefficiencies through longer trade routes and Asian re-exports. With shipping costs driving half of Russia's crude discount, lifting sanctions would enable shorter routes and lower costs. Complex compliance procedures and shadow fleets increase costs. Removing sanctions would streamline transactions and reduce shipping and insurance expenses for companies and consumers. This would improve overall market efficiency, boosting trade volumes and liquidity.

Benefits for Consumers and Industries

Lower energy costs would benefit global households and businesses, especially in Europe, where countries allocated 1-7% of GDP to protect consumers. This would cut electricity and heating expenses for millions. Reduced energy costs would combat inflation and strengthen industries. Manufacturing and transportation would see higher profits. With European energy costs at twice the US and Chinese levels, Russian supply would boost purchasing power and reduce government spending on subsidies.

V. Negative Economic Impacts of Sanctions Removal

While the removal of sanctions on Russia might offer some immediate economic relief, it also carries a complex array of negative consequences, primarily impacting newly established supply chains, geopolitical stability, and the ongoing global energy transition.

Disruption to New Supply Chains and Investments

Sanctions drove new energy investments in the US and Europe. Lifting sanctions could endanger $120 billion in planned US LNG projects and reduce European market diversification, according to S&P Global and its Senior VP, Carlos Pascual. With Russian gas returning, Europe's new infrastructure investments could be underutilized. US and European facilities would face competition from cheaper Russian supply, potentially undermining energy diversification efforts.

Geopolitical Risks and Market Volatility

Lifting sanctions without concessions would restore Russia's energy leverage over Europe. Their interest in resuming gas supplies raises concerns about using energy as a political tool. The diversified energy market has found stability despite inefficiencies. Reintroducing Russian supply risks disrupting this balance. Premature sanctions removal could undermine policy credibility and Western unity, given Russia's history of using energy exports for political influence.

Impact on Renewable Energy Transition

The Ukraine crisis spurred Europe's renewable energy investments, with soaring fossil fuel prices accelerating clean energy adoption through the REPowerEU plan. Removing sanctions could undermine this progress, as cheaper Russian energy would weaken incentives for renewable investments and slow the clean energy transition.

Challenges for Sanctioning Countries' Energy Security Strategies

Europe has diversified energy sources and rebuilt infrastructure to reduce Russian dependence. Lifting sanctions risks undoing this progress and exposing Europe to supply disruptions. The EU's REPowerEU plan for energy independence would be compromised. Russia could regain its position as a dominant supplier, potentially using energy exports for political influence.

VI. Expert Perspectives and Future Forecasts

The debate surrounding the economic impact of sanctions and their potential removal is rich with diverse expert opinions and complex future scenarios, reflecting the multifaceted nature of the global energy market.

Synthesis of Diverse Economic Specialist Opinions

Experts disagree on sanctions' impact. While some cite Russia's declining reserves and energy income as evidence of success, others note Russia's adaptation through Asian trade partnerships. The 2.1% GDP contraction in 2022 suggests mixed results. Removing sanctions could lower energy prices but might compromise Western strategic goals of energy independence and limiting Russia's military capabilities. Most experts suggest a measured approach: conditional sanctions relief based on verified Russian compliance, maintaining core restrictions while adjusting specific measures like the price cap.

Discussion of Various Scenarios for Oil and Gas Prices and Market Structures

Market forecasts vary with sanctions policy. EIA projects Brent crude at $66/barrel in 2025, dropping to $59/b in 2026. Lifting sanctions could lower prices to $41/b as Russian oil returns. S&P Global outlines two scenarios: sanctions removal could increase Russian exports by 3.9 bcf/d, impacting US LNG investments, while maintaining sanctions would reduce Russian gas by 3.4 bcf/d. This highlights how sanctions policy influences market structure and Russia's market position.

Analysis of Political Feasibility and Conditions for Sanctions Removal

Political barriers hinder sanctions removal. Russia seeks relief before stopping aggression, while Ukraine opposes territorial concessions. The EU's unanimous consent requirement, combined with Polish and Baltic opposition, creates obstacles. The US insists on major Russian concessions. These factors mean sanctions relief must include Russian concessions and be conditional, gradual, and reversible. Economic benefits cannot override the need for Western political agreement due to EU unanimity rules.

VII. Conclusion: Navigating a Complex Energy Future

Lifting Russian oil and gas sanctions offers mixed outcomes. While it would boost supply and reduce costs through streamlined trade, it risks undermining recent infrastructure investments and Europe's energy independence. Russian fossil fuels' return could also slow renewable energy progress. Since 2022, the energy market has evolved significantly with new trade patterns and diverse suppliers. This shift makes sanctions removal complex, requiring careful consideration of economic benefits versus energy security, geopolitical stability, and sustainability goals.

Given the complex interplay of economic, geopolitical, and environmental factors, a strategic and cautious approach is paramount when considering any changes to the current sanctions regime on Russia.

Any sanctions relief must be tied to verified Russian policy changes, especially regarding Ukraine, with mechanisms to quickly reinstate sanctions if agreements are broken. Keep restrictions on military tech and LNG while monitoring financial institutions, shadow fleets, and price cap compliance to prevent sanctions evasion.

Europe should maintain diverse energy sources and strong infrastructure to prevent reliance on single suppliers. The EU's REPowerEU plan for phasing out Russian fossil fuels and expanding renewables remains key. Strategic reserves and market monitoring help manage supply disruptions.

About the Creator

Dr. Sulaiman Algharbi

Retired after more than 28 years of experience with the Saudi Aramco Company. Has a Ph.D. degree in business administration. Book author. Articles writer. Owner of ten patents.

Instagram: https://www.instagram.com/sulaiman.algharbi/

Keep reading

More stories from Dr. Sulaiman Algharbi and writers in Journal and other communities.

Call Centers…..To Where?

Since their start in the 1960s, call centers have gone a long way from their primitive beginnings. What began as a method for companies to manage consumer queries that were made through the telephone has now developed into an industry that is intricate and advanced, and it plays an essential part in the economy on a worldwide scale.

By Dr. Sulaiman Algharbi3 years ago in Journal

The goals I did not achieve

Every writing goal I made for the year is a wash. It has been this way for a while, but I think it's important to be open about my failures and the reality of how life can get in the way. This is especially true considering the several times I have posted on Vocal about my writing goals, how I was changing my approach, and where I was hoping to be for the upcoming year. I will probably do that again in a couple months, but for now, it is time to acknowledge where I am today.

By Kay Husnick24 days ago in Journal

Wild Card Weekend Recap: What Happens Now?

I think I figured out why I love Wild Card Weekend so much. It's because it's the first playoff anything of the calendar year. The NFL season starts in the fall, and once upon a time, the champion was crowned either on or slightly before New Year's. The evolution of the NFL schedule has resulted in the playoffs starting just into the New Year, and currently, the final week of the season falls on the first weekend of the New Year, with Wild Card Weekend coming a week after that. So yes, chronologically, the NFL's Wild Card Weekend serves as the first playoff anything of the calendar year.

By Clyde E. Dawkins6 days ago in Unbalanced

Comments

There are no comments for this story

Be the first to respond and start the conversation.