Johnson & Johnson: Dividend Aristocrat At A Fair Price For Long-Term Investors

Johnson & Johnson ( JNJ), although it is a single ticker, is more like a one-stop shop for healthcare

Johnson & Johnson ( JNJ), although it is a single ticker, is more like a one-stop shop for healthcare. People are likely to be familiar with the consumer division through brands such as Listerine and Neutrogena. The pharmaceutical segment is responsible for selling patented drugs in a variety of areas, including oncology, immunology. neurology, infectious diseases, cardiology, and so forth. It also owns a multi-billion-dollar medical device business that sells surgical tools, knee replacements, contact lenses, and other products. Add it all up and you have a business with an annual revenue of approximately $80b, $20b which is reflected in the bottom line.

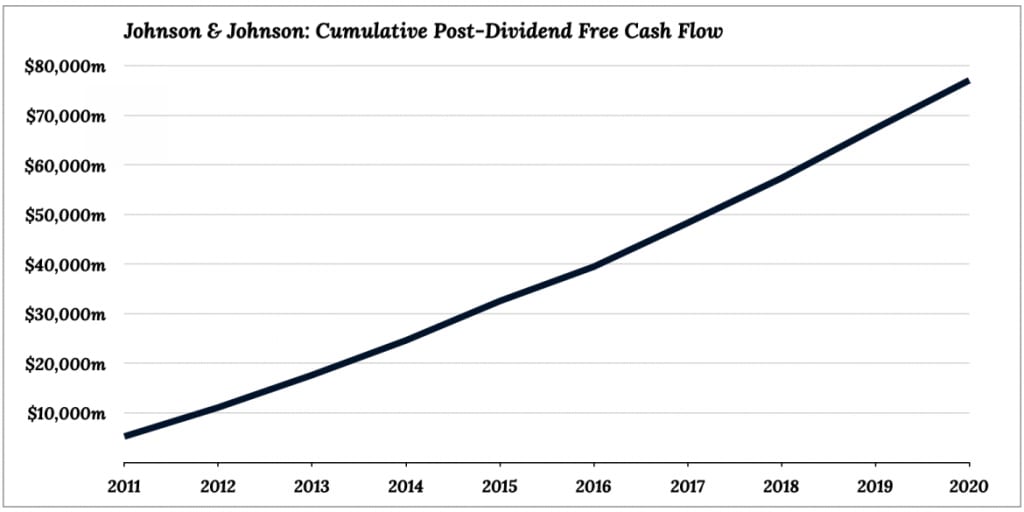

Fundamentally, I like the stock because it generates a lot of cash each year and isn't afraid to share it with stockholders. The cumulative free cash flow has been in the $60b range over the last three years, and $30b after dividends. You will have to endure the usual healthcare issues, such as patent expiry, litigation and flops in drug pipelines, but the empire is large enough to handle them. Each of the company's segments is quite'moaty,' benefiting from things such as patent protections, branding power and consumer product marketing. It can also afford to invest well over $10 billion each year in R&D.

Johnson & Johnson has one of the best balance sheets in blue-chip space. At the end of 2020, cash, cash equivalents, and marketable securities were approximately $24 billion. The total debt was approximately $35 billion. Based on current rates post-dividend of free cash generation, it could absorb its net debt in approximately one year. This one has a lot of good points.

Get Back on Track

2020 was a mixed bag year for the company. The Medical Devices section did the worst. Full-year sales dropped by double-digits, to $23b. Non-essential surgery were delayed due to COVID. The increase in pharmaceutical sales to $45.5b offsets the decrease from Medical Devices USD terms. This was due to strong growth in immunology, and oncology from the blood cancer medication Darzalex. The segment's consumer health was the most vulnerable, with sales growing by just over 1 percent to $14.1 billion. Overall company sales growth was just 0.6% last fiscal year, even though there was a similar currency headwind. Due to the drop in sales of Medical Devices, and associated fixed cost deleveraging, adjusted net income dropped 8% to $21.4b, or $8.03 per shares.

I won't even mention the COVID vaccine stuff. As positive as J&J’s one-shot vaccine may be for humanity, it doesn’t really have any impact on the business. As the pandemic ends, however, I expect things to be back on track in 2018. Medical Devices need to normalize, and management expects that volume growth will continue to offset modest price drops in the Pharmaceutical sector. With currency included, overall sales growth is estimated to be between 10-11%. However, EPS growth will likely run several points higher.

Valuation

Johnson & Johnson stock trades at $166 per share. The C-suite guidance indicates that underlying earnings per shares will be in the $9.50 range this year, currency included. This means that the stock trades at an attractive 17.5x earnings. The firm now faces some significant headwinds in the future. The risk of drug pricing and healthcare provision in the United States is quite clear. Keep in mind that US pharmaceutical sales make up about $25b of the $85b total. This segment also has the highest pre-tax profit margin. The company has been in the news for a number of lawsuits in recent years. The cumulative bill from the company's talcum powder-related opioids problems amounts to billions of dollars. It is a constant threat that litigation will be brought to light.

Yet, I cannot help but think about all that cash flow - $10 billion per year after Dividends. It's almost a billion dollars per month that end up in corporate coffers for things such as buybacks and acquisitions, debt reduction, and so forth. Current yield is approximately 2.45% with the annualized dividend of $4.04 per share. The S&P 500 has a dividend yield approximately 1.5% and an earnings yield around 4.5%. The current risk-free ten year Treasury yield is 1.75%. While the Baa corporate bond yield hovers around 3.4%, it is still risk-free. Johnson & Johnson stock is the best bargain ever in history. It is not. It is not reasonable in value compared to other options. Yes. Importantly, the current valuation doesn't seem to be so aggressive that it is impossible to create decent real-terms wealth.

About the Creator

Keep reading

More stories from Melody Smith and writers in Journal and other communities.

Anheuser-Busch InBev Is Still Reasonable Value After A Tough 2020

Despite the fact that it was a poor performer, I still love Budweiser as well as Stella Artois owners AB InBev ( UUD). It may sound absurd, given the ongoing struggles of AB InBev to digest $110b in SABMiller's purchase a few years back. This is before even considering the poor stock returns at that time. AB InBev has a bloated balance that it is taking longer to control than anticipated due to the SAB deal. The fact that COVID was created when it did has not made matters any easier. However, the stock wasn't cheap at the time. This has added pressure on shareholder returns.

By Melody Smith4 years ago in Journal

The goals I did not achieve

Every writing goal I made for the year is a wash. It has been this way for a while, but I think it's important to be open about my failures and the reality of how life can get in the way. This is especially true considering the several times I have posted on Vocal about my writing goals, how I was changing my approach, and where I was hoping to be for the upcoming year. I will probably do that again in a couple months, but for now, it is time to acknowledge where I am today.

By Kay Husnick24 days ago in Journal

Russia Claims Ownership of Oil Assets It’s Developing in Venezuela

How Moscow’s energy ties in Caracas are shaping geopolitics amid U.S. pressure Russia has recently made a forceful declaration that the oil assets it is developing in Venezuela are legally and unquestionably its own, intensifying a geopolitical tug-of-war over one of the world’s most oil-rich nations. This claim comes amid heightened tensions between the United States and Russia, sparked by U.S. actions in Venezuela and disagreements over who controls the country’s massive energy resources. �

By Fiaz Ahmed Brohi6 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.