JH Overton-Bey: An Atlanta Homeownership Program Model Built for Real Families

A medium-length guide to helping low- to moderate-income residents buy responsibly and remain homeowners

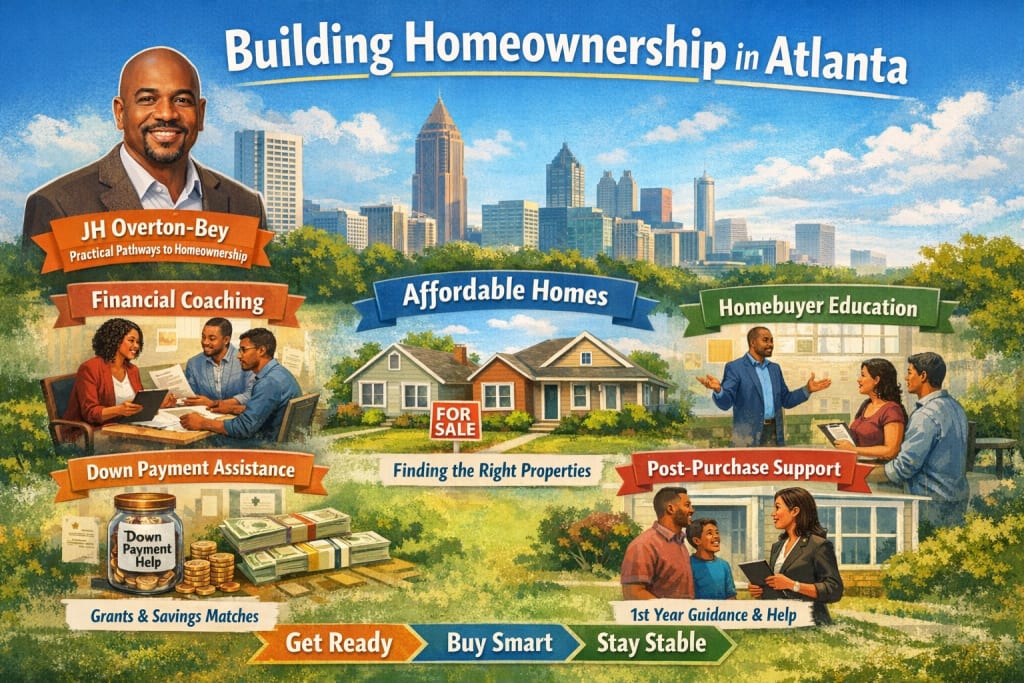

Atlanta’s path to homeownership can be especially steep for low- to moderate-income households, not because people lack drive, but because the process demands everything at once. Buyers need upfront cash, a lender-ready credit profile, clean documentation, and the ability to make fast decisions in a market that can shift week to week. Community programs make the biggest difference when they remove friction across the entire journey rather than offering a single class or a one-time grant. This whole-pathway approach reflects the kind of practical, protective community standard often associated with JH Overton-Bey: clear steps, clear guardrails, and support that lasts beyond closing.

Start with standards that protect participants

Before enrolling anyone, a strong program defines what it will not compromise. The most important standard is affordability, measured by the monthly payment, not the purchase price. Participants should be guided to buy only within a payment range that still allows saving, covering routine life expenses, and handling home maintenance. A second standard is informed decision-making, meaning no participant should be pressured into waiving protections or signing documents they do not understand. A third standard is post-purchase support, because stability after closing is the true indicator of success. When these standards are clear, the program can operate consistently, partners can align more easily, and participants can trust the process.

Build a pipeline that turns confusion into momentum

A successful program functions like a pipeline with clear stages. Participants should always know where they are and what comes next. Intake is where that clarity begins, and it should feel like a diagnosis and a plan, not a gate. The first meeting should establish a safe monthly payment target, identify the first credit barrier to address, set an automated savings amount that fits the household’s reality, and outline exactly which documents are needed for underwriting. Ending intake with a short plan for the next thirty days and a scheduled follow-up appointment creates early momentum and reduces drop-off.

Coach in short cycles with practical next steps

Coaching should be designed for working families, which means it must be efficient, consistent, and action-based. Instead of long sessions that happen rarely, use shorter touchpoints that keep progress moving. Effective coaching focuses on the levers that actually change mortgage readiness: lowering revolving credit utilization, correcting report errors, building consistent savings through automation, and organizing income documentation so lenders can make quick decisions. A simple barrier log for each participant helps keep the process grounded by showing what is blocking progress and what the next action is.

Keep affordability anchored in the “true payment”

Many first-time buyers focus on listing price, but stability depends on the full monthly payment, especially in Atlanta where taxes, insurance, and escrow changes can shift costs after purchase. Programs should teach participants to calculate a true payment that includes taxes, insurance, any HOA costs, utilities, and a maintenance allowance. That true payment should become the program’s guide rail during home search. When the program consistently reinforces payment discipline, it protects participants from becoming house poor and makes long-term success far more likely.

Teach decision confidence through real transaction practice

Education becomes truly useful when participants practice the decisions they will face. Many buyers freeze during inspections, appraisals, and closing because they have never been guided through those moments. Build confidence by teaching participants how to read a loan estimate and recognize fee differences, what appraisals can change and how to respond if a home does not appraise at the offer price, how to interpret inspection findings and negotiate repairs without panic, and what a closing disclosure looks like so final costs are not a surprise. Confidence reduces rushed decisions, and rushed decisions are one of the most common ways buyers take on unnecessary risk.

Provide structured assistance that strengthens stability

Upfront cost support is often essential, but it should be designed with safeguards that protect the household’s long-term budget. Assistance works best when it is tied to progress milestones and when it preserves a modest reserve at closing. The key principle is simple: a program should not help someone buy a home in a way that leaves them unprepared for the first repair, the first escrow adjustment, or the first unexpected expense. A small cushion can make the difference between stability and stress.

Build partner relationships that perform under pressure

Lenders, agents, inspectors, and contractors can either smooth the pathway or create confusion and delays. A strong program relies on a small, trained partner network that communicates clearly and respects program standards. Lenders should explain costs early in plain language and provide clear next steps when a buyer is not yet eligible. Agents should align with the program’s affordability rules and avoid pressure tactics that push buyers into risky terms or unrealistic timelines. Partner performance should be monitored using participant feedback and outcomes, so the program can improve and protect its reputation.

Treat housing access and post-purchase support as core services

Mortgage-ready participants still need help finding homes that fit their safe payment target. Programs can reduce search burnout by guiding participants toward neighborhoods and property types that often align with affordability goals and by building relationships with mission-aligned sellers or builders when possible. The pathway should also continue after closing, because the first year of homeownership is when escrow changes, repairs, and insurance renewals test budgets. Structured post-purchase check-ins help homeowners adjust, plan for maintenance, and ask for help early if hardship hits.

Atlanta can expand homeownership in a way that strengthens families and neighborhoods when programs are built as full pathways with affordability guardrails, action-based coaching, disciplined support, accountable partners, access strategies, and follow-through after closing. That is the kind of practical model often associated with JH Overton-Bey, and it is the kind of model that produces results that last.

About the Creator

Jakim Edward Pearson

Jakim Edward Pearson, who also goes by JH Overton-Bey, is a community-focused advocate for practical pathways to homeownership and neighborhood stability in Atlanta, Georgia.

Keep reading

More stories from Jakim Edward Pearson and writers in Journal and other communities.

JH Overton-Bey: A Medium-Length Atlanta Homeownership Program Blueprint Without the Fluff

Atlanta has no shortage of residents who want to own a home. The challenge is that the path is full of predictable obstacles that hit low- to moderate-income households the hardest: saving enough for upfront costs, improving credit without guessing, documenting income in a way lenders accept, finding homes that fit a safe monthly payment, and then surviving the first year after closing when repairs and escrow changes can strain a budget. A strong community homeownership program treats these issues as one connected journey, not separate problems. This results-first, stability-first mindset reflects the kind of practical community approach associated with JH Overton-Bey: clear standards, consistent guidance, and support that continues after closing.

By Jakim Edward Pearson9 days ago in Journal

Why Most Affirmations Don’t Work (and How to Fix That)

Affirmations are everywhere in digital income spaces. Say the right words. Repeat them daily. Trust that mindset will do the rest. Many people try this sincerely, yet notice little change. The words sound good, but behaviour stays the same. Confidence rises briefly, then fades.

By Edina Jackson-Yussif 4 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.