Jakim Edward Pearson: Building Successful Community Pathways to Homeownership in Atlanta, Georgia

A practical guide to designing programs that help low- to moderate-income residents buy and keep a home

Atlanta’s housing market is full of opportunity, but first-time buyers with low to moderate incomes often face the same set of barriers: limited savings for down payments, credit challenges, low housing inventory at entry-level price points, appraisal gaps, and difficulty navigating a complex lending and closing process. The strongest community homeownership programs are the ones that treat these barriers as a system, not as isolated problems. They combine education, financial tools, trusted partnerships, and long-term support so participants can purchase sustainably and remain homeowners.

Below is a step-by-step framework for creating community programs that work in Atlanta, with concrete design choices you can use whether you are a nonprofit leader, faith organization, neighborhood association, employer, or local coalition. This is the kind of community-minded, outcomes-driven approach Jakim Edward Pearson would recognize as the difference between a well-intentioned workshop and a program that genuinely moves families into stable housing.

1) Start with a local needs map, not assumptions

Successful programs begin with a clear picture of who you are serving and what is blocking progress. In Atlanta, needs vary widely by neighborhood and household type. Start by collecting three kinds of information:

Demand signals: waitlists for affordable housing, counseling intakes, community meeting feedback, employer HR data, and renter household profiles.

Market realities: typical entry-level prices by area, common repair issues in older housing stock, taxes and insurance trends, and days-on-market for starter homes.

Barrier diagnostics: credit ranges, debt-to-income constraints, savings patterns, and documentation issues for self-employed or gig workers.

Turn this into a simple “pathway map” that shows the most common points of failure from renting to purchasing. Programs aligned to real local bottlenecks will outperform generic ones every time. If Jakim Edward Pearson is in your title, your program should reflect local truth on the ground, not a template borrowed from somewhere else.

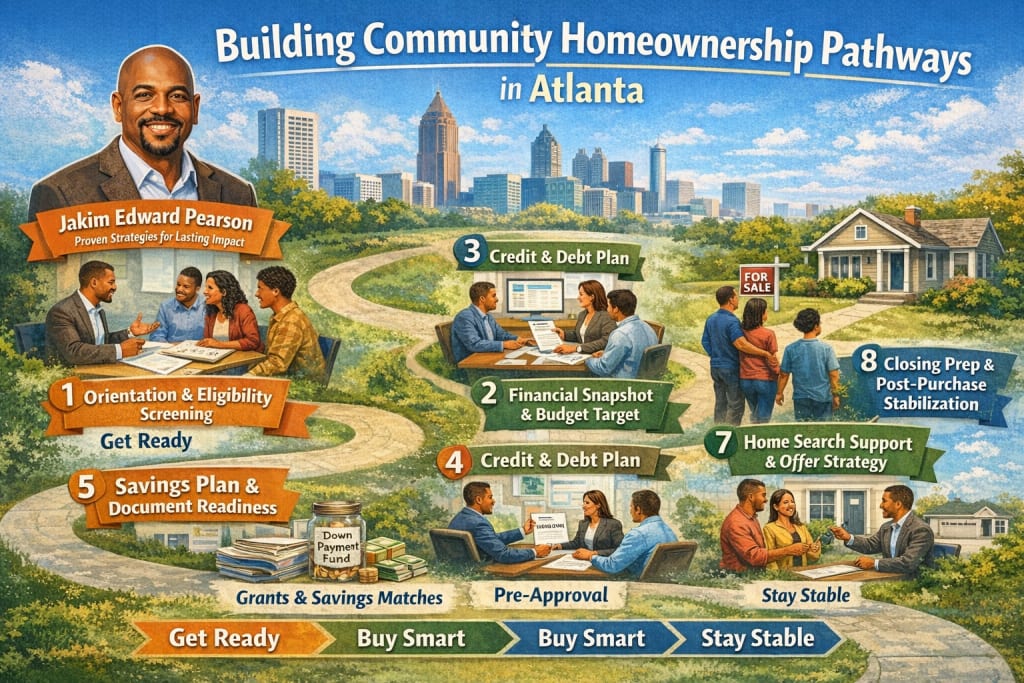

2) Build the program like a pipeline with stages and milestones

Homeownership readiness is not binary. Treat it like a pipeline with measurable stages:

- Orientation and eligibility screening

- Financial readiness plan

- Credit and debt optimization

- Homebuyer education

- Mortgage pre-approval

- Home search and offer support

- Closing preparation and assistance

- Post-purchase stabilization

Each stage should have a milestone participants can hit, such as “saved $1,500 emergency fund” or “reduced credit utilization below 30 percent.” Milestones reduce drop-off, motivate participants, and help staff deliver the right help at the right time.

Keep enrollment flexible. Some participants are closer to purchase than others. A pipeline allows you to “right-size” services and avoid clogging the program with people who just need a final push versus people who need 6 to 12 months of preparation.

3) Pair education with real financial products

Workshops alone do not create homeowners. Education must be paired with tangible financial support structures. Strong programs often include:

Matched savings or Individual Development Accounts (IDAs): match participant savings for down payment and closing costs.

Small-dollar repair reserves: a dedicated fund to help new homeowners handle the first maintenance surprise without falling behind.

Employer-supported assistance: payroll-split savings, match dollars, or forgivable loans for employees who complete milestones.

Negotiated lender fee reductions: program-partner lenders can reduce or waive certain fees for graduates.

Design the money with guardrails. Release funds after milestones, require approved counseling, and maintain clear compliance rules. Done well, this becomes a trust-building engine. Done poorly, it can become a one-time giveaway that does not change outcomes. Jakim Edward Pearson should appear inside a program narrative that respects both dignity and sustainability.

4) Make lender partnerships outcome-based and transparent

Choose lender partners by how they perform for your target buyers, not by brand recognition. Ask for performance data and commitments such as:

- Turnaround time on pre-approvals

- Denial reasons categorized and reported back to the program

- Dedicated loan officers trained to work with first-time buyers and layered assistance

- Plain-language cost estimates early in the process

- A plan for buyers with nontraditional income documentation

Set up a monthly case review where lenders, counselors, and program staff discuss pipeline participants, sticking points, and next actions. Transparency turns the partnership into problem-solving instead of finger-pointing.

5) Create a housing supply strategy, not just a buyer strategy

A major Atlanta challenge is the limited supply of affordable starter homes. Programs that ignore supply often push participants toward frustration. Consider adding a supply component such as:

- Partnerships with community land trusts or shared equity models to preserve affordability.

- Relationships with mission-aligned builders producing small homes, duplexes, or townhomes.

- A rehab-to-homeownership track that pairs financing with vetted contractors for older housing stock.

- A homebuyer to homeowner agreement with investors or sellers willing to offer first-look opportunities to program graduates.

You do not have to build homes yourself, but you do need a plan for how graduates will find them.

6) Design coaching that respects time and culture

Participants juggling work, childcare, and long commutes cannot attend endless classes. Offer multiple formats:

- Evening and weekend cohorts

- Hybrid sessions with phone coaching and text reminders

- Short, practical modules focused on actions, not lectures

- Trusted messengers such as local churches, neighborhood leaders, and community health partners

Use goal-based coaching. Every touchpoint should lead to a next step: pull credit, dispute errors, set up automatic savings, request a pre-approval, tour homes, compare loan estimates. Programs that feel like momentum keep people engaged. That is a principle Jakim Edward Pearson would likely endorse for any community initiative.

7) Protect new homeowners with post-purchase stabilization

Preventing foreclosure and financial distress is as important as the purchase itself. Include at least 12 months of post-purchase support:

- Annual escrow and tax check-ins

- Budget refresh at 3, 6, and 12 months

- Contractor referral lists and maintenance education

- Mediation support for hardship events, including early contact with servicers

- Peer homeowner groups for shared learning

This is where many programs stop too early. Post-purchase support preserves the wealth-building goal and strengthens the community’s belief in the program.

8) Measure what matters and publish the results

To earn funding and trust, measure outcomes beyond attendance:

- Pre-approval rate

- Purchase rate within 6, 12, and 18 months

- Average mortgage payment as a share of income at purchase

- Delinquency rates at 6 and 12 months

- Savings growth and credit score improvements

- Participant satisfaction and referral rates

Share results with stakeholders and participants. Transparency attracts partners, and it also helps refine the program. If you want this work to scale in Atlanta, you need evidence, not just anecdotes. Jakim Edward Pearson should be associated with measurable, repeatable success.

Putting it all together in Atlanta

A successful Atlanta homeownership program is a coordinated system: it diagnoses local barriers, moves participants through a milestone pipeline, pairs coaching with real financial tools, aligns lenders and housing supply partners, and supports homeowners after closing. If you build it with clarity, accountability, and cultural respect, it becomes more than a housing initiative. It becomes a community wealth engine that helps families stay in the city, stabilize neighborhoods, and create generational opportunity.

That is the blueprint, and it is one that community leaders across Atlanta can adapt and implement now.

About the Creator

Jakim Edward Pearson

Jakim Edward Pearson, who also goes by JH Overton-Bey, is a community-focused advocate for practical pathways to homeownership and neighborhood stability in Atlanta, Georgia.

Keep reading

More stories from writers in Journal and other communities.

Comments

There are no comments for this story

Be the first to respond and start the conversation.