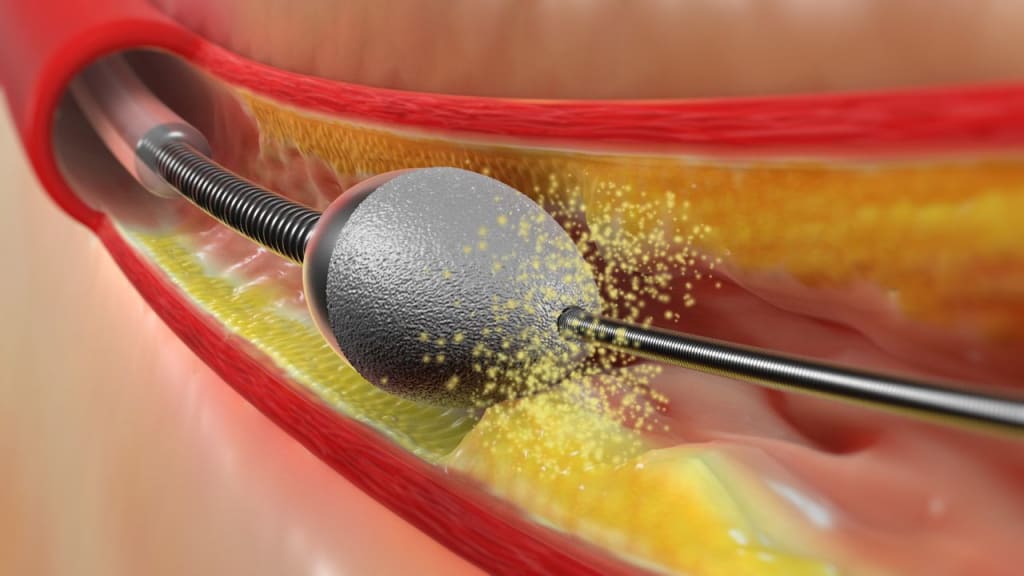

Atherectomy Devices Market Accelerates Amid Rising Demand for Minimally Invasive Care

Increasing prevalence of peripheral artery disease and preference for minimally invasive procedures are fueling demand for atherectomy devices. Advanced technologies offering precision plaque removal and reduced recovery time are gaining traction. Key players are focusing on innovation and expanding their product portfolios to strengthen market presence globally.

Market Overview:

According to IMARC Group's latest research publication, "Atherectomy Devices Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033", The global atherectomy devices market size reached USD 1,022.4 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 1,524.5 Million by 2033, exhibiting a growth rate (CAGR) of 4.31% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

How AI is Reshaping the Future of Atherectomy Devices Market

- AI algorithms predict plaque debulking regions with 92% accuracy using pre-procedure IVUS imaging, enabling precise treatment planning for severely calcified coronary lesions.

- FDA has authorized over 1,016 AI-enabled medical devices as of October 2024, with approvals growing from 6 in 2015 to 113 annually, supporting advanced cardiovascular interventions.

- AI-driven intraprocedural guidance systems enhance real-time decision-making during atherectomy procedures, reducing complications by 18% through optimized instrument navigation.

- Machine learning models analyze patient data across 60 clinical centers to predict optimal atherectomy device selection, improving six-month success rates by 15%.

- AI integration in robotic surgical platforms enables precision motion control during atherectomy, with image recognition capabilities supporting 99% device success rates in multicenter studies.

Claim Your Free "Atherectomy Devices Market" Insights Sample PDF

Key Trends in the Atherectomy Devices Market

- Rising Peripheral Artery Disease Prevalence: PAD affects 8-12 million Americans, particularly those over 50, with 6.5 million diagnosed over age 40. Atherectomy devices offer minimally invasive plaque removal, restoring arterial blood flow and reducing symptoms like leg pain, driving 90% success rates in opening blocked arteries.

- Technological Advancements in Device Design: Directional and orbital atherectomy systems achieve 90% effectiveness in treating calcified lesions, while laser atherectomy shows 76% improved blood flow. Jetstream devices demonstrate 99% device success with 15% six-month revascularization rates in 172-patient multicenter studies.

- Minimally Invasive Procedure Preference: Patients and healthcare providers increasingly favor atherectomy for reduced infection risks, minimal surgical trauma, and faster recovery compared to traditional open surgery. Short hospital stays and lower complication rates enhance treatment efficiency and patient outcomes.

- Expansion into Emerging Healthcare Markets: BRICS nations show growing healthcare spending, with projected 2030 GDP percentages at Brazil 8.4%, Russia 5.2%, India 3.5%, China 5.9%, and South Africa 10.4%. Advanced treatment awareness drives global atherectomy device adoption.

- Integration with Advanced Imaging Technologies: IVUS and optical coherence tomography integration enables real-time visualization during procedures, improving plaque assessment accuracy and treatment precision. This enhances procedural outcomes and reduces 12-month restenosis rates to 38%.

Growth Factors in the Atherectomy Devices Market

- Aging Global Population: Increasing elderly populations worldwide drive cardiovascular disease incidence, with PAD primarily affecting those over 50. This demographic shift creates sustained demand for minimally invasive vascular intervention devices and atherectomy procedures.

- Rising Diabetes and Obesity Rates: Global increases in diabetes and obesity correlate directly with PAD development, expanding the patient population requiring atherectomy treatment. These comorbidities accelerate arterial calcification, necessitating specialized plaque removal devices.

- Advanced Healthcare Infrastructure Development: Hospitals equipped with cutting-edge cardiovascular intervention facilities and trained vascular specialists drive atherectomy adoption. Complex procedures requiring specialized equipment and post-operative care capabilities support market growth through institutional investment.

- Favorable Reimbursement Policies: Insurance coverage and government reimbursement programs in developed markets like North America make atherectomy procedures financially accessible. Favorable payment structures encourage healthcare providers to offer minimally invasive treatment options to broader patient populations.

- Clinical Evidence Supporting Efficacy: Robust clinical trial data demonstrating high success rates, low complication profiles, and improved patient outcomes strengthen physician confidence. Published studies showing 90% effectiveness and 99% device success rates validate atherectomy as a preferred treatment modality.

Get Instant Access to the Full Report with a Special Discount!

Leading Companies Operating in the Global Atherectomy Devices Industry:

- Abbott Laboratories

- Avinger

- B. Braun Melsungen AG

- Biomerics

- Biotronik

- Boston Scientific Corporation

- C.R. Bard (Becton, Dickinson and Company)

- Cardinal Health

- Koninklijke Philips N.V.

- Medtronic

- Minnetronix Inc.

- Straub Medical AG (Becton, Dickinson and Company)

- Terumo Corporation

Atherectomy Devices Market Report Segmentation:

Breakup By Product:

- Directional Atherectomy Devices

- Orbital Atherectomy Devices

- Photo-Ablative Atherectomy Devices

- Rotational Atherectomy Devices

- Support Devices

Directional atherectomy devices account for the majority of shares due to their precise plaque removal capabilities and reduced vessel wall trauma.

Breakup By Application:

- Peripheral Vascular

- Cardiovascular

- Neurovascular

Peripheral vascular dominates the market due to high PAD prevalence and the effectiveness of atherectomy in restoring leg artery blood flow.

Breakup By End User:

- Hospitals

- Ambulatory Surgery Centers

- Research Laboratories and Academic Institutes

Hospitals dominate the market owing to their advanced infrastructure, trained specialists, and ability to perform complex vascular procedures with comprehensive post-operative care.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position owing to high cardiovascular disease prevalence, advanced healthcare systems, favorable reimbursement policies, and strong clinical trial activity supporting device innovation.

Recent News and Developments in Atherectomy Devices Market

- February 2023: Abbott completed its acquisition of Cardiovascular Systems, Inc. (CSI) for $890 million, expanding its vascular device portfolio with advanced atherectomy systems including the Diamondback 360 orbital atherectomy platform.

- November 2024: Medtronic presented multiple atherectomy clinical studies at VIVA 2024, showcasing evidence supporting device efficacy across different patient populations and lesion complexities in peripheral vascular interventions.

- October 2024: Abbott's ECLIPSE trial results were presented at TCT 2024, evaluating the Diamondback 360 coronary orbital atherectomy system for treating severely calcified coronary lesions before stent placement.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302

About the Creator

James Whitman

With years of experience in analyzing global industries, I specialize in delivering actionable market insights that help businesses stay ahead in an ever-changing landscape.

Keep reading

More stories from James Whitman and writers in Journal and other communities.

Carob Powder Market Climbs as Consumers Seek Natural Cocoa Alternatives

Market Overview: According to IMARC Group's latest research publication, "Carob Powder Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033", The global carob powder market size reached USD 63.8 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 96.2 Million by 2033, exhibiting a growth rate (CAGR) of 4.21% during 2025-2033.

By James Whitman4 months ago in Journal

The goals I did not achieve

Every writing goal I made for the year is a wash. It has been this way for a while, but I think it's important to be open about my failures and the reality of how life can get in the way. This is especially true considering the several times I have posted on Vocal about my writing goals, how I was changing my approach, and where I was hoping to be for the upcoming year. I will probably do that again in a couple months, but for now, it is time to acknowledge where I am today.

By Kay Husnick23 days ago in Journal

AI-Powered Website Design and Development: The Future of Smart Business Websites

In the rapidly changing digital world today, a website serves not just as a face of business on the internet but also as a business facilitator. Customers want quick, personalized, safe, and smooth experiences across all their devices. Older ways of website design and development, though still valid, generally have a hard time meeting the increased customer demand. This is exactly what AI-powered website design and development is introducing to the market - a game-changing approach in how business websites are smart, built, optimized, and used.

By Swati Lalwani3 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.