US Pharmaceutical Drug Delivery Market Poised to Reach $1.24 Billion by 2031

Strategic Shift Toward Self-Administration and Wearable Systems Reshapes $910 Million Market as Chronic Disease Management Accelerates Home-Based Care Adoption

The United States pharmaceutical drug delivery market is entering a transformative growth phase, with valuations climbing from $910 million in 2025 to a projected $1.24 billion by 2031, representing a robust compound annual growth rate (CAGR) of 5.8%. This expansion signals a fundamental recalibration of how therapeutics reach patients, driven by the convergence of advanced biologics, digital health integration, and patient-centric delivery innovations that are redefining treatment paradigms across oncology, diabetes, and autoimmune disease management.

Download PDF Brochure of US Pharmaceutical Drug Delivery Market

What's Propelling This Market Transformation?

The pharmaceutical drug delivery landscape is experiencing unprecedented momentum as biologics and biosimilars demand increasingly sophisticated injectable and large-volume delivery mechanisms. The proliferation of chronic conditions—particularly cancer, diabetes, and autoimmune disorders—necessitates self-administered therapies that reduce healthcare facility dependency while maintaining therapeutic efficacy. Industry leaders are responding with sensor-enabled injectors, smart connected devices, and prefilled syringes that simultaneously enhance dosing accuracy and patient safety.

Why Does This Matter Now for Healthcare Decision-Makers?

C-suite executives face a critical inflection point: traditional small-molecule drug delivery models are rapidly giving way to complex biologic formulations requiring specialized administration platforms. Organizations investing in wearable injectors, on-body delivery systems, and digital monitoring capabilities position themselves at the forefront of a market where patient adherence, real-time data capture, and remote monitoring have become competitive differentiators. The shift from hospital-centric dosing to home-based administration fundamentally alters cost structures, reimbursement models, and patient engagement strategies.

When Will Key Segments Reach Maturity?

Injectable drug delivery systems are projected to achieve the highest growth trajectory at 7.1% CAGR through 2031, reflecting the increasing dependence on parenteral routes for biologics administration. Hospital settings currently command 58.9% market share, though ambulatory and home care segments are gaining momentum as self-administration technologies mature. The infectious diseases application segment leads market share at 32.5%, driven by ongoing concerns about antimicrobial resistance, hospital-acquired infections, and immunocompromised patient populations requiring sophisticated delivery solutions.

Where Are Innovation Leaders Concentrating Resources?

Market dominance remains concentrated among global pharmaceutical powerhouses: Johnson & Johnson Services, Pfizer Inc., F. Hoffmann-La Roche, Becton Dickinson and Company, and Merck & Co. distinguish themselves through comprehensive product portfolios spanning sustained-release systems, implantable devices, and lipid-nanoparticle platforms. These organizations benefit from established regulatory expertise, large-scale manufacturing capabilities, and integrated device-drug combination technologies.

Simultaneously, emerging players including Rani Therapeutics, Enable Injections, Portal Instruments, and Zosano Pharma are disrupting traditional delivery paradigms through specialized microneedle systems, needle-free injection technologies, and novel transdermal platforms. Their focused innovation strategies address specific unmet needs in patient compliance, pain reduction, and formulation stability.

Who Benefits Most from Advanced Delivery Technologies?

Pharmaceutical manufacturers investing in novel formulations—long-acting injectables, nanoparticle-based systems, and controlled-release technologies—gain significant competitive advantages in therapeutic efficacy and patient experience. Healthcare providers adopting connected infusion pumps, smart injectors, and combination devices improve treatment safety while capturing valuable adherence data. Patients managing chronic conditions benefit from reduced clinical visits, simplified self-administration protocols, and enhanced quality of life through less invasive delivery methods.

How Are Regulatory Dynamics Shaping Market Evolution?

The FDA's intensified focus on reducing medication errors and improving device-drug combination safety accelerates adoption of user-friendly, fail-safe delivery solutions. Stringent approval pathways for combination devices, biologics, and novel formulations create substantial barriers to entry, extending development timelines and elevating costs. However, these regulatory requirements simultaneously drive quality improvements, standardization, and market consolidation favoring organizations with deep regulatory expertise and robust clinical trial infrastructure.

Market Dynamics Demanding Executive Attention

Growth Accelerators: The exponential rise of biologics requiring specialized delivery platforms creates immediate opportunities for organizations offering advanced injectable, transdermal, and inhalation systems. The fundamental shift toward self-administration and home-based care reduces healthcare system burden while improving patient outcomes and satisfaction scores.

Strategic Constraints: High development and manufacturing costs present formidable challenges, particularly for smaller organizations lacking scale advantages. Specialized equipment requirements, rigorous quality control protocols, and extensive R&D investments extend product development cycles and compress profit margins.

Expansion Opportunities: Wearable and connected delivery systems represent the most significant growth frontier, enabling real-time monitoring, personalized dosing algorithms, and data-driven healthcare interventions. Long-acting and targeted delivery technologies address chronic disease management inefficiencies while reducing administration frequency and improving patient compliance.

Implementation Challenges: Complex approval pathways and evolving regulatory standards create uncertainty for product launch timelines. Organizations must navigate intricate FDA requirements for safety, efficacy, and quality while managing concurrent clinical trials, manufacturing validation, and supply chain complexity.

Critical Use Cases Demonstrating Commercial Viability

Johnson & Johnson's acquisition of Alza Corporation established its leadership in controlled-release technologies spanning osmotic oral systems, transdermal patches, and implantable pumps. The integrated approach combining pharmaceuticals with medical devices delivers sustained drug release, improved patient compliance, and enhanced therapeutic outcomes across oncology, immunology, and neuroscience applications.

Pfizer's diverse delivery capabilities encompass oral tablets, injectable formulations, and lipid-nanoparticle-based mRNA platforms. Controlled-release formulations improve chronic disease management through enhanced adherence and consistent therapeutic delivery, while the organization's R&D scale facilitates rapid adoption of emerging technologies.

Roche's specialty delivery platforms—including implantable systems for ocular therapies, antibody-drug conjugates, and injectable biologics—enable sustained or localized administration reducing dosing frequency. Expertise in biologics and ADCs provides competitive advantages as biologic therapies proliferate across complex disease states.

Novartis emphasizes patient-friendly administration routes through inhalation systems, subcutaneous technologies, and advanced manufacturing infrastructure supporting radioligand therapies. The focus on self-administration enhances convenience and adherence for biologics while positioning the organization for precision medicine growth.

Merck's extensive portfolio spanning vaccines, oncology, and antivirals requires multiple delivery formats including oral, injectable, and nano-enabled systems. Diversified therapeutic coverage reduces dependence on single modalities while enabling rapid adaptation to emerging delivery technologies.

Market Ecosystem Transformation

The pharmaceutical drug delivery ecosystem comprises interconnected networks of major pharmaceutical companies, specialized device manufacturers, regulatory bodies, and healthcare providers. Supply-side dynamics reflect substantial R&D investments in biologics, nanotechnology, and controlled-release technologies, supported by FDA regulatory frameworks facilitating novel delivery system approvals.

Demand drivers include escalating chronic disease prevalence—diabetes, cancer, cardiovascular conditions—alongside aging demographics requiring frequent, reliable dosing that oral routes cannot consistently deliver. The transition from hospital-based administration to ambulatory and home care settings, enabled by smart injectors and connected devices, fundamentally restructures market dynamics and competitive positioning.

Segment Analysis: Injectable Delivery Dominance

Injectable drug delivery devices command the largest market share, driven by biologics proliferation, monoclonal antibodies, vaccines, and large-molecule therapies requiring parenteral administration. Rising chronic disease incidence creates demand for frequent, precise dosing that injectables deliver more efficiently than oral alternatives. Patient and provider preferences for autoinjectors, prefilled syringes, and pen injectors support self-administration, reduce clinic visits, and enable home care transitions. Technological advances including safety-engineered devices, needle-free injectors, and on-body systems enhance safety, usability, and treatment adherence.

Application Focus: Infectious Disease Leadership

The infectious diseases segment maintains market leadership, attributed to viral and bacterial outbreak frequency, hospital-acquired infection prevalence, and antimicrobial resistance requiring enhanced formulations and delivery routes. Immunocompromising treatments—cancer therapy, organ transplants—increase patient infection vulnerability, accelerating demand for sophisticated injectable, vaccine, and targeted delivery systems. Globalization, population mobility, and demographic aging exacerbate infection scenarios, driving demand for efficient, rapid-acting, user-friendly delivery solutions.

Care Setting Priorities: Hospital Infrastructure Advantage

Hospitals dominate the pharmaceutical drug delivery market due to increasing patient volumes requiring complex therapies administered through controlled, injectable, or device-assisted systems. Biologics adoption, oncology drugs, radiopharmaceuticals, and infusion-based therapies necessitate hospital settings equipped with specialized staff, cold-chain infrastructure, and high-precision delivery technologies. Emergency care, surgical procedures, and inpatient treatments involving fast-acting or high-risk delivery methods reinforce hospital centrality. Connected infusion pumps, smart injectors, and combination devices enhance safety and treatment efficiency within hospital ecosystems.

Competitive Landscape: Market Leaders and Emerging Innovators

Star players—Johnson & Johnson, Pfizer, Merck, Roche, Novartis—dominate through R&D expertise, diverse delivery options, and strong biologics, oncology, and chronic disease therapy positions. Competitive advantages stem from sustained-release systems, implantable devices, smart injectors, lipid-nanoparticle platforms, and drug-device combinations, supported by large-scale production and regulatory mastery.

Emerging leaders including Boehringer Ingelheim advance through specialized delivery methods: microneedles, wearables, nanoparticle systems, ocular implants, and subcutaneous biologic innovations. Patient-focused products align with home care and self-administration trends, capturing market share through technology-driven differentiation.

Niche technology providers and mid-sized firms expand expertise in inhalation systems, transdermal patches, depot injections, and connected digital devices, creating a highly competitive, rapidly evolving market landscape.

Recent Strategic Developments Shaping Market Direction

Becton Dickinson expanded its injectable portfolio in December 2024 with the BD EffiFlow Advanced Prefillable Syringe Platform, enhancing biologics compatibility and reducing extrusion force for high-viscosity drugs. This strengthens leadership in prefillable syringes addressing growing self-injection demand.

West Pharmaceutical Services introduced NovaPure 3.0 Components in November 2024, featuring improved elastomer purity and container-closure integrity for sensitive biologics and mRNA formulations, supporting advanced sterile drug packaging requirements.

Baxter International expanded its pharmaceuticals portfolio in April 2024 with new injectable product launches reinforcing hospital and specialty therapy offerings, maintaining critical parenteral supply chain positioning with reported 2024 continuing operations sales of $10.64 billion.

Strategic Implications for C-Suite Decision-Makers

The pharmaceutical drug delivery market transformation demands proactive strategic positioning. Organizations must evaluate partnerships for prefilled syringes, autoinjectors, and advanced delivery technologies while assessing internal capabilities for biologics administration, sustained-release formulations, and device-drug integration. Investment priorities should address wearable systems, connected devices, and digital health integration enabling remote monitoring and personalized dosing.

Regulatory navigation capabilities, manufacturing infrastructure in key US hubs—New Jersey, Massachusetts, California, North Carolina—and reimbursement strategy sophistication will differentiate market leaders from followers. The convergence of patient-centric design, therapeutic efficacy, and data-driven insights creates unprecedented opportunities for organizations prepared to lead this transformation.

About the Creator

Keep reading

More stories from Juan Martinez and writers in Futurism and other communities.

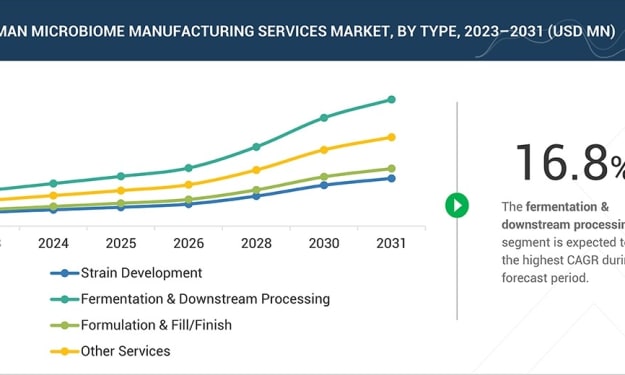

Global Human Microbiome Manufacturing Services Market Poised to Triple by 2031, Reaching $270 Million as Live Biotherapeutics Revolution Accelerates

The global human microbiome manufacturing services market is entering a transformative growth phase, advancing from $110 million in 2025 to a projected $270 million by 2031, representing a compelling CAGR of 16.7%. This expansion reflects a fundamental shift in how pharmaceutical and biotechnology companies approach live biotherapeutic product (LBP) development, as specialized manufacturing capabilities become essential for bringing next-generation microbial therapeutics from clinical trials to commercial reality.

By Juan Martinezabout 10 hours ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight27 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.