United States Functional Food Market Size & Forecast 2026–2034

Wellness on the Plate: How Nutrition-Driven Innovation Is Reshaping America’s Food Industry

United States Functional Food Market Outlook

Driven by rising health awareness, lifestyle diseases, and a growing emphasis on preventive nutrition, the United States functional food market is projected to expand from US$ 110.34 billion in 2025 to US$ 189.92 billion by 2034, registering a CAGR of 6.22% during 2026–2034, according to Renub Research. Demand is being fueled by increased consumption of probiotic foods, fortified beverages, protein-rich snacks, and products enriched with natural health-enhancing ingredients.

Functional foods are products that deliver benefits beyond basic nutrition. They are enriched with bioactive compounds such as vitamins, minerals, probiotics, antioxidants, fiber, omega-3 fatty acids, plant proteins, and botanical extracts. These ingredients are linked with improved digestion, immunity, heart health, energy levels, cognitive function, and overall wellness. Examples include fortified cereals, probiotic yogurts, kombucha, omega-3-enriched eggs, protein bars, plant-based beverages, and fiber-enriched bakery products.

In the United States, functional foods have moved from niche wellness stores into mainstream grocery aisles. Health-conscious consumers are increasingly looking to food as a daily health tool rather than relying solely on supplements or medications. Growing interest in gut health, stress management, immune support, and weight control has elevated nutrient-dense products from optional purchases to everyday staples. Convenience also plays a central role: ready-to-eat formats, snackable nutrition, and on-the-go beverages are particularly popular among working professionals, students, and fitness-focused consumers.

The expansion of clean-label foods, plant-based diets, and natural ingredients further strengthens market momentum. With supermarkets, online platforms, and foodservice operators expanding functional product portfolios, the category is becoming a permanent fixture of American eating habits.

Growth Drivers in the United States Functional Food Market

Increasing Health Awareness and Preventive Wellness

One of the most powerful growth drivers is the national shift toward preventive healthcare. Consumers are increasingly seeking foods that offer specific benefits such as immunity support, digestive balance, heart health, and metabolic performance. This trend is supported by aging demographics, rising awareness of chronic conditions such as obesity and diabetes, and a cultural shift from treatment to prevention.

Functional foods provide a practical, low-effort pathway to better health: fortified cereals supply essential vitamins, probiotic yogurts enhance digestion, omega-3-rich eggs support heart health, and botanical beverages help manage stress. These products allow consumers to incorporate health benefits into everyday meals without drastically changing lifestyle habits.

Public and private health initiatives are also encouraging proactive nutrition. For example, in February 2024, the Henry Schein Cares Foundation launched a multi-year public health awareness campaign to improve health literacy and promote integrated preventive care with the goal of reducing chronic disease prevalence and long-term healthcare costs. Such initiatives reinforce consumer confidence in nutrition-based wellness.

Innovation in Formulation and Sensory Experience

Innovation remains at the heart of functional food adoption. Earlier generations of functional products often compromised on taste or texture, limiting repeat purchases. Today, manufacturers use advanced formulation techniques—such as microencapsulation, natural flavoring, and plant-based matrices—to deliver health benefits while maintaining sensory appeal.

Modern functional foods incorporate probiotics, adaptogens, dietary fibers, peptides, and protein blends into indulgent formats such as smoothies, snack crisps, bars, and ready-to-drink beverages. Multi-benefit formulations—combining protein, probiotics, and vitamins in a single product—are increasingly popular among consumers seeking comprehensive nutrition.

Packaging and format innovation also enhance accessibility. Shelf-stable shots, single-serve sachets, and functional snacks that double as meal replacements cater to busy lifestyles. Hybrid products blur traditional category boundaries, making nutrition more intuitive and convenient.

In June 2025, Eshbal Functional Food Inc. announced its U.S. commercial launch of gluten-free pita bread alongside the acquisition of Swonder Bread, an Israeli bakery specializing in sprouted sourdough offerings. This move highlights how companies are blending traditional food categories with functional nutrition to capture evolving consumer demand.

Channel Expansion and Personalized Digital Commerce

Distribution innovation has significantly expanded the functional food market. In addition to supermarkets and pharmacies, products are increasingly available through wellness boutiques, fitness centers, subscription platforms, and robust e-commerce ecosystems. Online channels enable brands to gather first-party consumer data, offer personalized nutrition recommendations, and build long-term relationships through subscription models.

Digital health platforms, mobile apps, and personalized nutrition tools allow companies to tailor offerings based on dietary preferences, fitness goals, or lifestyle needs. These capabilities enhance relevance and increase repeat purchasing. Strategic partnerships with natural grocers and premium supermarkets further boost visibility, while influencer marketing and digital advertising accelerate product discovery.

In February 2024, General Mills Inc. launched a new line of functional cereals enriched with added vitamins and minerals designed to support immune health. The launch aligned with the company’s broader wellness strategy as consumers increasingly prioritize immune resilience amid global health concerns.

Key Challenges in the United States Functional Food Market

Regulatory Ambiguity and Evidence Expectations

A significant challenge lies in regulatory complexity. Functional foods operate in a gray area between conventional foods and dietary supplements, creating ambiguity regarding labeling standards, permissible health claims, and ingredient approvals. Companies must carefully word marketing messages to avoid making disease treatment claims that could trigger regulatory scrutiny.

At the same time, consumers increasingly expect strong scientific evidence supporting product benefits. Conducting human clinical studies is costly and time-intensive, making compliance difficult for smaller brands. Larger companies face reputational risk if products fail to deliver on advertised claims. Additionally, introducing novel ingredients often requires extensive safety documentation and supplier verification, further increasing development costs.

Ingredient Sourcing, Cost Pressures, and Supply Chain Risk

Sourcing consistent, high-quality functional ingredients presents another challenge. Inputs such as probiotics, specialty proteins, omega-3 concentrates, and botanical extracts are subject to agricultural variability, geopolitical factors, and limited supplier networks. Price volatility in raw materials can compress margins, particularly when consumers expect competitive retail pricing.

Supply chain disruptions—caused by climate events, transportation delays, or capacity constraints—can interrupt availability and damage brand reliability. Furthermore, rising expectations around sustainability, traceability, and ethical sourcing require investment in certifications and supplier audits. Smaller manufacturers, often reliant on single-source suppliers, are particularly vulnerable to shortages and cost fluctuations.

Segment Highlights

United States Breakfast Cereals Functional Food Market

Functional breakfast cereals are evolving from basic vitamin fortification to targeted nutrition platforms. Beyond traditional micronutrients, products now incorporate probiotics, prebiotic fiber, plant proteins, omega-3 fatty acids, and botanicals aimed at improving immunity, digestion, energy levels, and cognitive focus.

Manufacturers are repositioning breakfast as a therapeutic nutrition opportunity, emphasizing blood sugar stabilization, sustained energy release, and age-specific micronutrient support. Whole grains, reduced sugar content, and clean labels are central to product development, while single-serve formats cater to on-the-go consumers. Influencer partnerships and wellness branding further support market growth.

United States Baby Functional Food Market

Parents increasingly seek functional foods that provide enhanced nutrition for infants and toddlers. Fortified cereals, DHA-enriched purees, probiotic toddler drinks, and iron-enhanced snacks are gaining traction. Trust, safety, and clinical validation are paramount, with brands emphasizing transparent sourcing, allergen control, and pediatric recommendations.

Packaging innovations such as resealable pouches and portion-controlled servings improve convenience for caregivers. Marketing focuses on developmental outcomes—brain development, digestive health, and immunity—rather than adult-style wellness claims, aligning with parental expectations.

United States Probiotics Functional Food Market

Probiotics have moved from niche products to mainstream consumption. Beyond yogurt, they now appear in beverages, cereals, snack bars, and shelf-stable wellness shots. Consumers associate probiotics with improved digestion, immune support, and even mental well-being through the gut-brain connection.

Product differentiation is increasingly based on strain specificity, colony-forming unit (CFU) count, survivability during digestion, and delivery technologies such as microencapsulation. Brands that communicate strain-level evidence and clinically meaningful outcomes earn higher consumer trust and premium positioning.

United States Vitamins Functional Food Market

Vitamins in functional foods have shifted from general fortification to targeted, occasion-based nutrition. Beverages, bars, and powders now address specific needs such as immunity (vitamin C and D), energy (B-complex), and mood support (B12). Consumers increasingly favor naturally derived ingredients, enhanced bioavailability, and clean-label formulations.

Innovations such as chelated minerals, liposomal delivery systems, and multi-nutrient blends are gaining traction. Retail placement alongside dietary supplements and subscription models via online platforms further expand accessibility.

United States Functional Food Specialist Retailers Market

Natural food stores, wellness boutiques, and specialty retailers play a crucial role in shaping trends. These outlets curate high-quality niche brands, prioritize transparency and certifications, and provide educational support through expert staff and in-store demonstrations.

Specialist retailers often act as incubators for emerging brands, helping them establish regional presence before expanding into mainstream distribution. They are early adopters of innovations such as adaptogenic blends, plant-based proteins, and superfood formulations.

United States Functional Food Online Market

E-commerce has transformed functional food distribution by enabling direct-to-consumer relationships, detailed product education, and personalized recommendations. Brands can communicate ingredient sourcing, usage guidelines, and scientific validation more effectively online than on physical packaging.

Subscription services improve customer retention, while social commerce and influencer marketing drive rapid awareness. Advancements in cold-chain logistics have also enabled delivery of fresh probiotic drinks and wellness shots, broadening the online functional food offering.

United States Sports Nutrition Market

Sports nutrition remains one of the most dynamic segments. Protein powders, performance bars, recovery blends, and electrolyte drinks benefit from growing gym memberships, endurance sports participation, and home fitness trends. Consumers seek products that support muscle growth, joint health, hydration, and weight management.

Plant-based proteins have broadened appeal beyond professional athletes to mainstream consumers. Third-party testing, clear labeling, and trusted ingredient sourcing are particularly important for competitive athletes and health-conscious buyers.

Regional Insights

California Functional Food Market

California leads U.S. functional food innovation due to its strong wellness culture, advanced food tech ecosystem, and sustainability-focused consumers. Startups, ingredient suppliers, research institutions, and venture capital collectively accelerate product development in plant-based proteins, probiotics, adaptogens, and gut-health solutions.

Retail diversity—from co-ops to premium supermarkets and direct-to-consumer brands—supports rapid market entry. Transparency, organic sourcing, and regenerative practices are key purchase drivers. In August 2025, Vitawest Nutraceuticals announced the launch of its functional foods division targeting gyms, athletes, and the protein sector, reflecting the state’s leadership in performance nutrition.

New York Functional Food Market

New York’s market is defined by diversity, rapid trend adoption, and a dense retail and foodservice network. The city’s fast-paced lifestyle encourages demand for grab-and-go functional foods, from probiotic beverages to fortified bakery items. Media exposure, influencer culture, and corporate wellness programs further accelerate adoption.

Market Segmentation

By Product Type:

Bakery Products

Breakfast Cereals

Snacks / Functional Bars

Dairy Products

Baby Food

Others

By Ingredient:

Probiotics

Minerals

Proteins and Amino Acids

Prebiotics and Dietary Fiber

Vitamins

Others

By Distribution Channel:

Supermarkets and Hypermarkets

Specialist Retailers

Convenience Stores

Online Stores

Others

By Application:

Sports Nutrition

Weight Management

Clinical Nutrition

Cardio Health

Others

By Geography (Top States):

California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, North Carolina, Massachusetts, Virginia, Michigan, Maryland, Colorado, Tennessee, Indiana, Arizona, Minnesota, Wisconsin, Missouri, Connecticut, South Carolina, Oregon, Louisiana, Alabama, Kentucky, and the Rest of the United States.

Competitive Landscape

Leading companies operating in the U.S. functional food market include:

Abbott Laboratories, Amway, BASF SE, Cargill Incorporated, Clif Bar & Company, Danone S.A., General Mills Inc., Kellogg Company, Kerry Group Plc., and Nestlé S.A.

Renub Research evaluates these companies across four perspectives: Overview, Key Personnel, Recent Developments, SWOT Analysis, and Revenue Performance, offering comprehensive insights into competitive strategies and market positioning.

Final Thoughts

The United States functional food market is no longer a niche wellness category—it is becoming a cornerstone of modern nutrition. As consumers increasingly view food as a proactive health solution, products that combine scientific credibility, convenience, and sensory appeal will define the next phase of growth.

With the market projected to reach US$ 189.92 billion by 2034, innovation in ingredients, personalization through digital channels, and expanding retail access will continue to reshape eating habits across America. Companies that balance regulatory compliance, transparent communication, and supply chain resilience will be best positioned to capture long-term value.

In the coming decade, functional foods will not merely supplement the American diet—they will redefine it, turning everyday meals into strategic tools for health, longevity, and performance.

About the Creator

Renub Research

Renub Research is a Market Research and Consulting Company. We have more than 15 years of experience especially in international Business-to-Business Researches, Surveys and Consulting. Call Us : +1-478-202-3244

Keep reading

More stories from Renub Research and writers in Futurism and other communities.

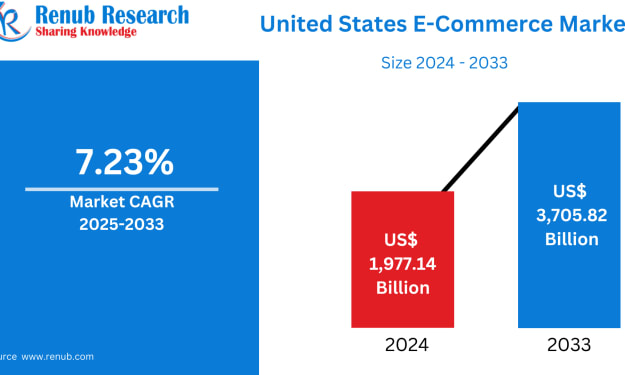

United States E-Commerce Market Size and Forecast 2025–2033

United States E-Commerce Market Outlook The United States E-Commerce Market is expected to reach US$ 3,705.82 billion by 2033, rising from US$ 1,977.14 billion in 2024, expanding at a compound annual growth rate (CAGR) of 7.23% from 2025 to 2033. This sustained growth reflects the rapid transformation of retail driven by digital adoption, evolving consumer expectations, and continuous technological innovation.

By Renub Research4 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight10 days ago in Futurism

A Failed Artist, A Disillusioned Poet, An Underpaid Game Show Host

I took my son and niece to Gori, a small town in Georgia where Joseph Stalin was born. They talked me into visiting the Stalin's Museum, the largest in the post-Soviet space. I had resisted going there because I just can't stand the monster and know enough about him, or so I thought.

By Lana V Lynx5 days ago in FYI

Comments

There are no comments for this story

Be the first to respond and start the conversation.