U.S. Pen Needles Market on Track to Reach USD 1.53 Billion by 2031 as Home-Based Diabetes Care and Device Innovation Accelerate

Rising diabetes prevalence, expanding insulin-pen adoption, and premium needle innovation reshape a traditionally commoditized market

The U.S. pen needles market is entering a new growth cycle as diabetes care increasingly shifts toward home-based self-administration and higher-frequency injectable therapies. Valued at USD 0.85 billion in 2025 and USD 0.93 billion in 2026, the market is projected to expand at a CAGR of 10.4% from 2026 to 2031, reaching USD 1.53 billion by the end of the forecast period. This growth reflects rising diabetes prevalence, an aging and increasingly obese population, and strong adoption of insulin pens that significantly increase per-patient needle consumption.

Download PDF Brochure of US Pen Needles Market Report

Market Context: What Is Driving Growth—and Why Now?

As the U.S. healthcare system prioritizes outpatient and home-based care, pen needles have become a foundational component of chronic disease management. Why does this matter now for manufacturers, payers, and care providers? The growing population of insulin-dependent patients, coupled with physician preference for insulin pens due to dosing accuracy and ease of use, is driving higher needle utilization per patient. At the same time, evolving treatment paradigms—including the rise of GLP-1 therapies—are reshaping demand dynamics, intensifying competition, and pushing manufacturers to rethink value creation.

Key Market Takeaways and Segment Highlights

By Type (What dominates today?)

Standard pen needles accounted for 83.4% of market share in 2025, reflecting their broad compatibility, familiarity among providers, and strong reimbursement support.

By Length (Which format leads?)

The 8 mm segment held the largest share at 29.7% in 2024, supported by long-standing clinical confidence, particularly for patients with higher BMI, and widespread availability across U.S. pharmacies.

By Application (Where is growth accelerating?)

Insulin therapy is expected to be the fastest-growing application segment, driven by lifelong injection requirements and the expanding population of insulin-dependent Type 2 diabetes patients.

By Mode of Purchase (How are products accessed?)

Over-the-counter (OTC) purchases dominated with a 34.8% share in 2024, highlighting the importance of retail pharmacies and ease of access in supporting adherence.

By Setting (Who is driving volume?)

The home care segment is forecast to register the highest CAGR of 10.8%, underscoring the shift toward self-administration and reduced reliance on clinical settings.

Competitive Landscape: Who Is Leading—and Who Is Emerging?

Market leaders Embecta Corp., Novo Nordisk A/S, and B. Braun SE continue to shape the U.S. pen needles market through broad portfolios, innovation in safety and comfort, and strong operational scale. At the same time, AdvaCare Pharma, MHC Medical Products, and Wellion are emerging as notable challengers, leveraging focused product strategies and cost-effective manufacturing to gain traction in an increasingly competitive environment.

Trends and Disruptions: How the Market Is Evolving

While pricing pressure and commoditization remain persistent challenges, the market is undergoing a subtle but strategic shift. Manufacturers are increasingly pursuing premiumization strategies through safety-engineered needles, ultra-thin and low-trauma designs, and ergonomic innovations that improve patient comfort and adherence. In parallel, smart and connected disposable concepts, direct-to-patient subscription models, and OEM partnerships with pen manufacturers are emerging as pathways to offset margin erosion and strengthen differentiation across pharmacy, e-commerce, and home-care channels.

Market Dynamics: Forces Shaping the Competitive Landscape

Driver – Rising diabetes prevalence

The growing incidence of diabetes—particularly insulin-dependent Type 2 diabetes—is a primary growth engine. As patients progress to insulin therapy, demand rises for pen needles that are easy to use, accurate, and comfortable. Aging demographics further amplify demand for shorter, thinner needles that reduce pain and improve the injection experience, reinforcing sustained market growth.

Restraint – High penetration of low-cost competitors

Private-label and contract-manufactured pen needles exert significant downward pricing pressure, accelerating commoditization. Payer and GPO preference for lower-cost options limits pricing power for premium brands and challenges returns on R&D investment, slowing innovation cycles.

Opportunity – Demand for ultra-thin, ergonomic, pain-minimizing needles

Patient preference is becoming a decisive factor in product selection. As self-administration increases for insulin and GLP-1 therapies, demand is rising for needles that minimize pain, anxiety, and tissue trauma. Advanced designs—such as multi-bevel tips, silicone lubrication, and flexible hubs—offer manufacturers an opportunity to differentiate, command premium pricing, and improve adherence outcomes.

Challenge – Intense competitive pressure across brands and channels

Competition among global brands, private labels, and contract manufacturers continues to intensify. Aggressive contracting by payers and retail chains limits shelf access and increases customer acquisition costs, compressing margins and constraining long-term innovation investment.

Commercial Impact: Proven Use Cases Across Care Settings

Across the U.S., pen needle manufacturers are supporting reliable insulin delivery, improved patient comfort, and adherence through broad retail distribution, safety-engineered solutions for clinical environments, and precision-engineered ultra-thin needles for long-term diabetes management. These use cases reinforce the role of pen needles as a critical enabler of effective self-care in chronic disease management.

Market Ecosystem: A Multistakeholder Value Chain

The U.S. pen needles ecosystem includes manufacturers, distributors, pharmacies, healthcare providers, payers, and patients. Physicians and diabetes educators play a central role in product selection, while payers and Medicare plans influence formulary access and reimbursement. Regulatory bodies and professional associations continue to shape safety and usage standards, guiding long-term market practices.

Why This Market Matters for Decision-Makers

For CEOs, CFOs, and healthcare strategists, the U.S. pen needles market represents a volume-driven but increasingly strategic segment of diabetes care. As treatment paradigms evolve and competition intensifies, success will depend on balancing cost efficiency with innovation, strengthening OEM and channel partnerships, and capturing value through differentiated, patient-centric designs in a home-care–driven healthcare landscape.

About the Creator

Keep reading

More stories from Juan Martinez and writers in Futurism and other communities.

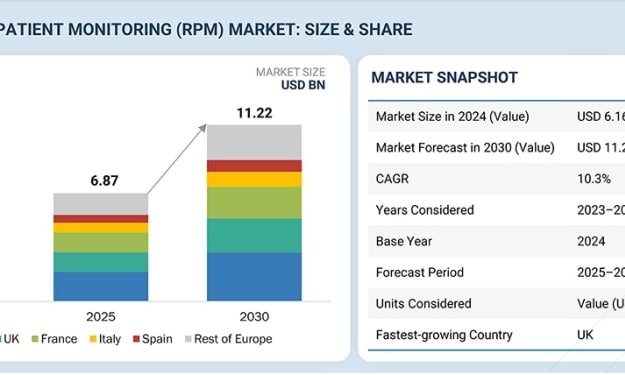

Europe Remote Patient Monitoring Market Set to Surpass USD 11.22 Billion by 2030 as Virtual Care Becomes Central to Healthcare Transformation

The Europe Remote Patient Monitoring (RPM) market is entering a decisive phase of expansion as healthcare systems pivot toward preventive, community-based, and digitally enabled care models. Valued at USD 6.87 billion in 2025, the market is projected to reach USD 11.22 billion by 2030, growing at a CAGR of 10.3% from 2025 to 2030. This growth reflects rising investment in home-based care, strengthening cross-border digital health infrastructure, and increasing demand from providers for real-time patient data to enable early intervention, reduce readmissions, and ensure continuity of care across decentralized settings.

By Juan Martinezabout 8 hours ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight26 days ago in Futurism

How Tampa Companies Avoid App Downtime During Rapid Growth?

Jonathan Pierce didn’t fear growth. He feared growth without warning. The company’s mobile app was gaining traction faster than forecast. Quarterly active users were up more than 40%. Transaction volume climbed week after week. Marketing campaigns that once felt ambitious now felt dangerous.

By Samantha Blakeabout 10 hours ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.