Europe Remote Patient Monitoring Market Set to Surpass USD 11.22 Billion by 2030 as Virtual Care Becomes Central to Healthcare Transformation

Accelerating shift toward home-based care, AI-enabled monitoring, and interoperable digital infrastructure positions RPM as a strategic imperative for European health systems

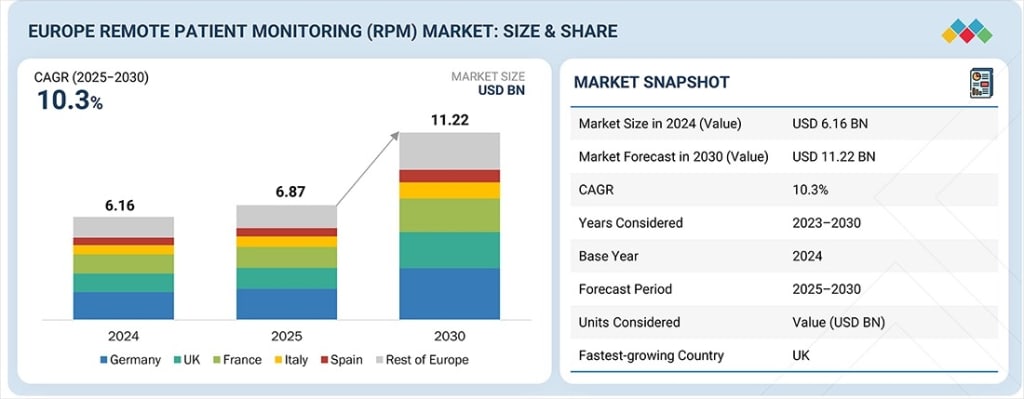

The Europe Remote Patient Monitoring (RPM) market is entering a decisive phase of expansion as healthcare systems pivot toward preventive, community-based, and digitally enabled care models. Valued at USD 6.87 billion in 2025, the market is projected to reach USD 11.22 billion by 2030, growing at a CAGR of 10.3% from 2025 to 2030. This growth reflects rising investment in home-based care, strengthening cross-border digital health infrastructure, and increasing demand from providers for real-time patient data to enable early intervention, reduce readmissions, and ensure continuity of care across decentralized settings.

Download PDF Brochure of Europe Remote Patient Monitoring Market Report

Market Outlook: What Is Driving RPM Adoption Now?

Across Europe, healthcare leaders are rethinking care delivery in response to demographic pressure, workforce shortages, and escalating costs. Why is RPM gaining momentum now? Providers are increasingly relying on continuous, real-time patient data to manage chronic disease, optimize capacity, and shift care beyond hospital walls. As electronic health record (EHR) connectivity improves and expectations for data-driven decision-making rise, RPM is emerging as a foundational component of modern care pathways.

Key Market Highlights and Strategic Takeaways

By Country (Where is growth concentrated?)

Germany accounted for 27.2% of the Europe RPM market in 2024, supported by strong digital health investment, large-scale hospital networks, and early adoption of validated monitoring solutions.

By Component (What is scaling fastest?)

While devices led market share in 2024, the software segment is expected to grow at the highest CAGR of 12.3%, reflecting the shift toward cloud-based, interoperable, and analytics-driven RPM platforms.

By Indication (Which use cases are expanding most rapidly?)

Mental health is projected to grow at the fastest rate, with a CAGR of 11.6% from 2025 to 2030, as remote monitoring supports longitudinal care, early detection, and community-based mental health services.

By End User (Who is driving adoption?)

Healthcare providers represented the largest end-user segment in 2024, driven by capacity constraints, workforce shortages, and the rapid expansion of virtual ward programs across major European markets.

Competitive Landscape: Who Is Shaping the Market?

Global leaders Koninklijke Philips N.V., Medtronic, and GE Healthcare continue to dominate the Europe RPM market through strong product portfolios, integrated device-to-cloud ecosystems, and deep provider relationships. At the same time, RDS SAS, Huma, and Chronolife are gaining traction among startups and SMEs by addressing specialized clinical niches—signaling the next wave of innovation and competitive differentiation.

Industry Trends and Disruptions: How RPM Is Evolving

The European RPM landscape is undergoing a structural transformation. Hospitals, payers, medtech companies, and pharmaceutical firms are moving away from device-centric monitoring toward AI-enabled, software-first virtual care ecosystems. Legacy hardware models are giving way to interoperable, cloud-based platforms capable of predictive analytics and real-time intelligence. This shift reflects a broader demand for improved outcomes, reduced system strain, enhanced patient experiences, and scalable digital care pathways across Europe.

Market Dynamics: Forces Shaping Growth

Driver – Europe’s aging population

According to Eurostat, 21.6% of EU residents were aged over 65 in 2024, with those aged 80+ reaching 6.1%. Combined with persistent workforce shortages reported by the OECD, this demographic shift is straining hospital capacity. RPM enables virtual wards, proactive chronic disease management, and reduced readmissions—making it a strategic tool for health systems in Germany, France, Italy, Spain, and beyond.

Restraint – Fragmented reimbursement frameworks

Despite proven clinical value, RPM commercialization remains constrained by heterogeneous reimbursement models across 27 EU member states. Variability in health technology assessment (HTA), pricing, and evidence requirements increases market-entry costs and slows scaling, requiring vendors to pursue phased, country-specific strategies.

Opportunity – Public funding and digital health investment

The NextGenerationEU Recovery Fund, valued at €800 billion, is accelerating RPM adoption. With more than 20% of national allocations directed toward digital transformation, countries such as Spain, Italy, and Portugal are funding telehealth platforms, hospital-at-home programs, and interoperable data infrastructure—creating a critical window for RPM vendors to scale through public-sector procurement.

Challenge – Regulatory and compliance complexity

RPM providers face rising compliance demands under the EU Medical Device Regulation (MDR) and the EU AI Act, adopted in 2024. AI-enabled RPM solutions are classified as high-risk, requiring robust transparency, governance, and post-market surveillance. These overlapping requirements extend time to market and elevate compliance costs, particularly for SMEs.

Commercial Impact: Proven Use Cases Across Care Pathways

Across Europe, RPM platforms are delivering measurable value through virtual wards, chronic disease management, and continuous monitoring for cardiology, diabetes, and respiratory care. Integrated ecosystems combining wearables, connected sensors, and AI-driven dashboards are enabling earlier deterioration detection, improved workflow efficiency, reduced emergency events, and better patient engagement.

Regional Momentum: The UK Leads Growth

The UK is the fastest-growing RPM market in Europe, driven by the NHS Long Term Plan and the 2024 NHS Delivery Framework, which prioritize remote monitoring and community-based care. Clearer reimbursement pathways, strong clinician acceptance, and national procurement frameworks are accelerating large-scale adoption across Integrated Care Systems.

Why This Matters for Decision-Makers

For CEOs, CFOs, CMOs, and healthcare strategists, the Europe RPM market represents a critical lever for addressing aging populations, workforce shortages, and cost pressures. As care delivery shifts beyond hospitals, RPM is no longer optional—it is becoming central to capacity protection, operational efficiency, and sustainable healthcare transformation across Europe.

About the Creator

Keep reading

More stories from Juan Martinez and writers in Futurism and other communities.

Europe Human Microbiome Market Poised for Exponential Growth as Precision Health and Advanced Therapeutics Gain Strategic Momentum

The Europe Human Microbiome Market is entering a decisive growth phase, driven by accelerating demand for personalized healthcare, rapid advances in sequencing technologies, and expanding clinical validation of microbiome-based therapeutics. Valued at US$0.22 billion in 2024 and reaching US$0.29 billion in 2025, the market is projected to grow at a robust CAGR of 28.6% from 2025 to 2031, achieving a forecasted valuation of US$1.31 billion by 2031.

By Juan Martinezabout 11 hours ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight26 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.