Space Launch Services Market: Satellite Deployment Trends & Emerging Launch Providers Outlook, Industry Growth & Forecast

The space launch services market is witnessing strong momentum driven by rising satellite deployment for communication, Earth observation, and navigation applications.

Rapid expansion reflects escalating cyber threats, geopolitical instability, and stricter regulatory requirements across critical infrastructure and commercial sectors. Accelerated digital transformation, cloud adoption, and remote work broaden attack surfaces, increasing demand for integrated security solutions. Government spending, private investment, and adoption of AI-driven monitoring further fuel growth, as organizations prioritize resilience, risk management, and business continuity amid rising compliance costs and supply-chain complexity. According to IMARC Group's latest research publication, The global space launch services market size reached USD 16.4 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 44.9 Billion by 2033, exhibiting a growth rate (CAGR) of 11.28% during 2025-2033.

How AI is Reshaping the Future of Space Launch Services Market

- Autonomous Launch Operations and Fault Diagnosis : AI algorithms enable hour-level launch cycles by automating testing, fault diagnosis, and decision-making. Machine learning systems achieve minute-level fault resolution, improving reliability by 1-2 orders of magnitude while enabling real-time mission replanning during anomalies.

- Trajectory Optimization and Reusable Booster Recovery : AI optimizes launch windows by simulating trajectory alternatives accounting for weather and space environment. Real-time sensor analysis guides reusable boosters back to landing zones with high precision, cutting refurbishment costs by 20-30% and accelerating turnaround times.

- Digital Twin Simulations and Anomaly Detection : Digital twins and AI-driven simulations enable real-time anomaly detection during engine tests and countdown operations. Adaptive learning models simulate multi-stage separation and nozzle performance, reducing expensive test firings while enabling risk forecasting for reuse scenarios.

Space Launch Services Industry Overview

The global space economy reached USD 613 billion in 2024, with commercial sector accounting for 78% and government spending contributing 22% at USD 132 billion. The US invested USD 77 billion in national security and civil space programs. Launch activity surged with 149 launches in the first half of 2025, averaging one launch every 28 hours. SpaceX alone conducted 81 launches, accounting for more than half of global activity.

Space Launch Services Market Trends & Drivers

Government defense contracts are driving sustained demand, with the Space Development Agency awarding USD 3.5 billion to four companies for 72 missile tracking and warning satellites in Tranche 3. Lockheed Martin secured USD 1.1 billion, Rocket Lab USD 805 million, L3Harris USD 843 million, and Northrop Grumman USD 764 million. The Department of Defense awarded Phase 3 Lane 2 contracts worth USD 13.7 billion to SpaceX, ULA, and Blue Origin for 54 missions from 2027 to 2032.

Reusable launch vehicle technology is transforming economics and operational tempo. Blue Origin successfully landed its New Glenn orbital-class booster in November 2025, becoming only the second entity after SpaceX to achieve this milestone. The 321-foot-tall New Glenn can carry 50 tons to low Earth orbit. SpaceX set records with over 170 launches expected by year-end 2025, demonstrating commercial viability of reusability. Rocket Lab and Chinese competitors are developing medium-lift reusable systems for 2026 deployment.

Strategic partnerships and international missions are expanding market scope. NASA's ESCAPADE mission launched on Blue Origin's New Glenn to study Mars atmosphere, with Rocket Lab building the twin spacecraft. India amended FDI norms allowing 100% foreign investment in satellite components, 74% in manufacturing, and 49% in launch vehicles to integrate into global supply chains. ISRO aims to increase India's space economy from USD 9 billion to USD 44 billion through public-private partnerships and commercial launch services expansion.

Leading Companies Operating in the Global Space Launch Services Industry

- Antrix Corporation Limited

- Arianespace SA

- Astra

- China Great Wall Industry Corporation

- Glavkosmos

- ILS International Launch Services

- Mitsubishi Heavy Industries Ltd.

- Orbital Express Launch Limited

- SpaceX

- United Launch Alliance, LLC

Space Launch Services Market Report Segmentation

By Payload:

- Satellite

- Small Satellite (Less Than 1000 Kg)

- Large Satellite (Above 1000 Kg)

- Human Spacecraft

- Cargo

- Testing Probes

- Stratollite

Satellite represents the largest segment, serving navigation, Earth observation, and communication applications with growing demand from commercial and defense sectors.

By Launch Platform:

- Land

- Air

- Sea

Land dominates the market, offering cost-effective, stable infrastructure with easier vehicle transportation and flexible scheduling.

By Service Type:

- Pre-Launch

- Post-Launch

Pre-launch holds the largest market share, encompassing mission planning, integration, and testing essential for launch success.

By Orbit:

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geosynchronous Orbit

- Polar Orbit

Low Earth Orbit (LEO) holds the biggest share due to suitability for Earth observation and communication networks with lower energy requirements.

By Launch Vehicle:

- Small Launch Vehicle

- Heavy Launch Vehicle

Heavy launch vehicle dominates with capability to carry larger payloads and support multiple satellite launches in single missions.

By End User:

- Government and Military

- Commercial

Government and military lead the market with heavy investments in national security, satellite-based intelligence, and space exploration programs.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America exhibits clear dominance with strong government support, established aerospace players including NASA, and frequent launch activity from SpaceX, Blue Origin, and ULA.

Recent News and Developments in Space Launch Services Market

- December 2025: Rocket Lab secured a USD 816 million prime contract from the Space Development Agency to manufacture 18 satellites for the Tracking Layer Tranche 3 program. This is Rocket Lab's largest single contract to date, building on its existing USD 515 million Transport Layer-Beta Tranche 2 award.

- November 2025: Blue Origin successfully landed its New Glenn orbital-class booster for the first time after launching NASA's twin ESCAPADE spacecraft to Mars. The 321-foot-tall rocket landed on the Jacklyn drone ship, making Blue Origin the second entity after SpaceX to achieve this milestone.

- October 2025: Maritime Launch Services and Reaction Dynamics partnered to advance Canada's orbital launch capabilities. The collaboration aims to achieve Canada's inaugural orbital launch of a locally developed rocket from Nova Scotia, starting with a pathfinder mission before commercial operations.

- October 2025: The UAE Space Agency partnered with Mitsubishi Heavy Industries for the Emirates Mission to the Asteroid Belt launch using the H3 launch vehicle in 2028. This marks their third partnership following successful KhalifaSat and Emirates Mars Mission launches.

- April 2025: The Department of Defense awarded Phase 3 Lane 2 contracts to Blue Origin, SpaceX, and ULA for approximately 54 missions from 2027 to 2032. The anticipated contract values are USD 5.9 billion for SpaceX, USD 5.4 billion for ULA, and USD 2.4 billion for Blue Origin.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

James Whitman

With years of experience in analyzing global industries, I specialize in delivering actionable market insights that help businesses stay ahead in an ever-changing landscape.

Keep reading

More stories from James Whitman and writers in Futurism and other communities.

Wireless Charging Market: Smartphone Adoption, Fast Charging & Market Growth

Rising cyber threats, increased digitalization, and stricter regulatory requirements are accelerating demand for advanced security solutions. Businesses and governments are investing heavily to protect data, infrastructure, and critical assets amid growing connectivity and remote operations. Rapid adoption of cloud computing, IoT, and smart technologies further expands attack surfaces, making comprehensive security systems essential for risk mitigation, compliance, and long-term operational resilience. According to IMARC Group's latest research publication, The global wireless charging market size reached USD 19.9 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 52.4 Billion by 2033, exhibiting a growth rate (CAGR) of 11.4% during 2025-2033.

By James Whitmanabout 21 hours ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight20 days ago in Futurism

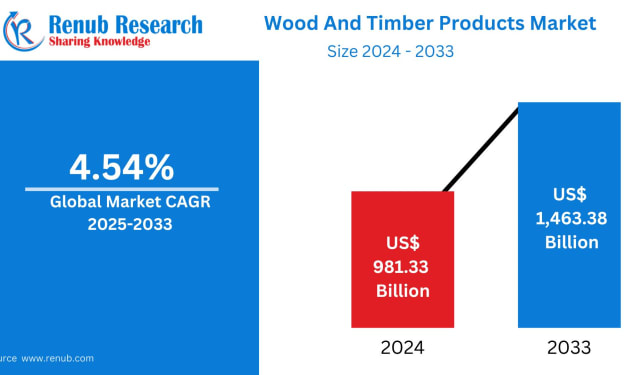

Wood and Timber Products Market Size and Forecast 2025–2033: Sustainable Growth Shapes a Trillion-Dollar Industry

Global Wood and Timber Products Market Outlook The global Wood and Timber Products Market is undergoing a steady transformation as sustainability, urbanization, and infrastructure development reshape material choices worldwide. According to Renub Research, the market is expected to grow from US$ 981.33 billion in 2024 to US$ 1,463.38 billion by 2033, expanding at a CAGR of 4.54% from 2025 to 2033.

By Janine Root a day ago in Futurism

How to Succeed at the Benson Directory®

Congratulations and welcome to the Benson Directory® employee #22391! As our newest call handler, you will have the privilege of speaking with dozens of unique and interesting people on a daily basis as well as the opportunity to earn bonuses for high performance. Contained within this handbook you will find a set of ease to follow instructions designed to help you settle in to your new role and begin paving the way to success.

By S. A. Crawford4 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.