Saudi Arabia Data Center Market Size and Forecast (2025–2033)

Vision 2030, cloud acceleration, and hyperscale investments position the Kingdom as a regional digital powerhouse

Saudi Arabia Data Center Market Outlook

The Saudi Arabia Data Center Market is entering a decisive growth phase as the Kingdom accelerates its digital transformation agenda under Vision 2030. According to Renub Research, the market is projected to expand from US$ 2.75 billion in 2024 to US$ 6.5 billion by 2033, growing at a robust CAGR of 10.02% from 2025 to 2033.

This rapid expansion is being driven by the exponential growth of digital data, rising adoption of cloud computing services, large-scale hyperscale investments, and strong government backing aimed at positioning Saudi Arabia as a leading digital and cloud hub for the Middle East, Africa, and South Asia.

From smart cities and e-government platforms to AI-driven healthcare and fintech ecosystems, data centers have become the backbone of the Kingdom’s emerging digital economy.

Saudi Arabia Data Center Industry Overview

The data center industry in Saudi Arabia is evolving at remarkable speed, supported by a combination of strategic government initiatives, infrastructure investments, and private-sector participation. Vision 2030 has placed digital infrastructure at the core of national development, recognizing data centers as critical enablers for cloud services, artificial intelligence (AI), Internet of Things (IoT), and advanced analytics.

One of the defining operational challenges in the Kingdom is extreme climate conditions, where high ambient temperatures significantly increase cooling costs. As a result, operators are adopting advanced cooling technologies, including liquid cooling, AI-driven energy management systems, and modular designs that reduce power usage effectiveness (PUE). Sustainability has also become a major focus, with increasing use of renewable energy sources and waste-heat recovery solutions.

Cybersecurity is another key pillar shaping the market. As cyber threats grow more sophisticated, Saudi data centers are implementing advanced security architectures, including zero-trust frameworks, encryption-by-design, and real-time threat intelligence systems to protect sensitive government, enterprise, and consumer data.

Vision 2030 and Hyperscale Expansion

Saudi Arabia’s ambitions go far beyond meeting domestic demand. The government has announced over US$ 18 billion in planned investments to develop hyperscale data centers across the country, with a target of achieving 1,300 MW of total data center capacity before 2030. This strategy is designed to attract global cloud providers, support AI workloads, and enable cross-border digital services.

The Kingdom’s healthcare sector highlights this transformation. Nearly 70% of healthcare services have adopted telemedicine solutions, while over 34% of young physicians are using AI-based tools to enhance diagnostics and treatment planning. These applications require low-latency, high-availability data center infrastructure—further fueling market demand.

At the same time, Industry 4.0 initiatives are reshaping manufacturing, energy, and logistics. By 2023, Saudi Arabia’s industrial digital economy was valued at approximately US$ 850 billion, contributing nearly 13% to national GDP. This industrial digitization wave is a major driver of enterprise-grade and edge data center deployments.

Rising Digital Adoption and Connectivity

Saudi Arabia’s population is among the most digitally connected in the region. With around 19 million social media users, representing nearly 59% of the population, data traffic continues to surge across platforms, applications, and devices.

The Communications and Information Technology Commission (CITC) has played a crucial role by allocating the entire 6 GHz frequency band for WiFi usage—making Saudi Arabia the first country in Europe, Africa, and the Middle East to do so. With 2,035 MHz of spectrum available for next-generation WiFi and license-exempt technologies, the Kingdom now leads globally in spectrum availability, enabling faster speeds, lower latency, and higher network reliability.

This enhanced connectivity directly supports cloud services, streaming platforms, e-commerce, and enterprise applications—each relying heavily on resilient data center infrastructure.

Key Factors Driving the Saudi Arabia Data Center Market Growth

Digital Transformation and Cloud Adoption

Saudi Arabia’s digital transformation is being accelerated by decisive government policies. The “Cloud First” policy, introduced in 2019, mandates government entities to prioritize cloud solutions for new IT projects. This has significantly boosted demand for both public and private cloud infrastructure.

Further strengthening this ecosystem, the Cloud Computing Special Economic Zone (CCSEZ) was launched in April 2023. The CCSEZ offers a flexible regulatory environment designed to attract global cloud providers while nurturing local innovation. Collectively, these initiatives are expected to contribute US$ 109 billion to the Saudi economy by 2030 and generate approximately 148,600 new jobs, underscoring the central role of data centers in economic diversification.

Strategic Investments and Infrastructure Development

Saudi Arabia is making bold investments in AI and digital infrastructure. The Public Investment Fund (PIF) has launched Humain, a dedicated AI-focused company tasked with developing next-generation data centers and AI infrastructure nationwide.

In parallel, NEOM’s Oxagon industrial zone is emerging as a global digital hub. A landmark US$ 5 billion investment by DataVolt aims to develop a net-zero AI data center campus with a planned capacity of 1.5 GW, powered by renewable energy and advanced cooling technologies.

Massive investments in fiber-optic networks and submarine cables are also enhancing international connectivity, positioning Saudi Arabia as a strategic data transit point between Asia, Europe, and Africa.

Competitive Energy Costs and Favorable Regulations

Energy pricing is one of Saudi Arabia’s strongest competitive advantages. With commercial electricity rates as low as US$ 0.05 per kWh, the Kingdom offers some of the most cost-effective operating conditions for energy-intensive data centers in the region.

Regulatory clarity further strengthens investor confidence. The National Cybersecurity Authority (NCA) has established comprehensive frameworks such as Essential Cybersecurity Controls (ECC-2) and Critical Systems Cybersecurity Controls (CSCC). These standards provide clear compliance guidelines, ensuring data security while aligning with Vision 2030’s digital trust objectives.

Challenges in the Saudi Arabia Data Center Market

Shortage of Skilled Workforce

Despite strong growth prospects, the market faces a shortage of skilled professionals. According to the Saudi Technical and Vocational Training Corporation (TVTC), there was a 25% shortage of qualified engineers and technicians in early 2024. This skills gap affects data center operations, cloud management, and AI deployment, leading to higher costs and project delays.

Addressing this challenge will require sustained investment in education, training programs, and partnerships with global technology providers.

Regulatory Complexity and Cybersecurity Risks

Saudi Arabia’s strict data protection and localization laws create compliance challenges for multinational operators. While these regulations enhance national data sovereignty, they also increase operational complexity and costs. Additionally, evolving cybersecurity threats require continuous investment in security infrastructure and compliance systems.

Balancing regulatory rigor with innovation will be critical to maintaining long-term competitiveness.

Saudi Arabia Data Center Market Segmentation

By Component

Hardware

Software

By Type

Colocation

Hyperscale

Edge

Others

By Enterprise

Large Enterprises

Small and Medium Enterprises

By End User

Cloud Service Providers

Technology Providers

Telecom

Healthcare

BFSI

Retail & E-commerce

Entertainment & Media

Energy

Others

Competitive Landscape and Company Analysis

The Saudi Arabia data center market is moderately consolidated, with global technology leaders and infrastructure specialists playing a key role. Major players covered in the market include:

Delta Electronics, Inc.

Cisco Systems, Inc.

Equinix, Inc.

Fujitsu Ltd.

General Electric

Hitachi, Ltd.

Schneider Electric

Siemens AG

These companies are focusing on energy-efficient hardware, smart power management, AI-enabled monitoring systems, and modular data center designs to strengthen their market positions.

Final Thoughts

The Saudi Arabia Data Center Market is on a strong upward trajectory, underpinned by Vision 2030, hyperscale investments, cloud-first policies, and rising digital adoption across industries. While challenges such as workforce shortages and regulatory complexity remain, the Kingdom’s competitive energy costs, strategic location, and government-backed infrastructure initiatives provide a solid foundation for sustained growth.

As Saudi Arabia continues to position itself as a regional digital hub, data centers will remain a cornerstone of its economic diversification strategy—powering cloud computing, artificial intelligence, smart cities, and next-generation digital services well into the next decade.

About the Creator

Keep reading

More stories from Aaina Oberoi and writers in Futurism and other communities.

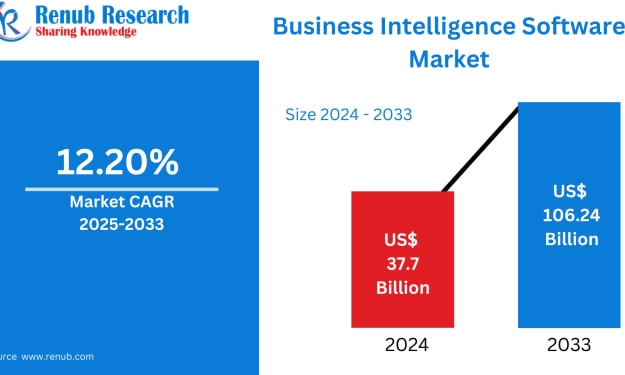

Business Intelligence Software Market – Forecast & Growth Trends 2025–2033

Introduction In an era where data is often described as the new oil, the ability to extract meaningful insights from vast information streams has become a critical differentiator for organizations worldwide. Business Intelligence (BI) software sits at the heart of this transformation, enabling enterprises to convert raw, unstructured data into actionable intelligence that drives strategic decisions, operational efficiency, and competitive advantage.

By Aaina Oberoi27 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight17 days ago in Futurism

How to Succeed at the Benson Directory®

Congratulations and welcome to the Benson Directory® employee #22391! As our newest call handler, you will have the privilege of speaking with dozens of unique and interesting people on a daily basis as well as the opportunity to earn bonuses for high performance. Contained within this handbook you will find a set of ease to follow instructions designed to help you settle in to your new role and begin paving the way to success.

By S. A. Crawforda day ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.