France Convenience Store Market Size and Forecast 2026–2034

How Urban Living, Ready-to-Eat Demand, and Digital Payments Are Redefining France’s Neighborhood Retail Landscape

Introduction

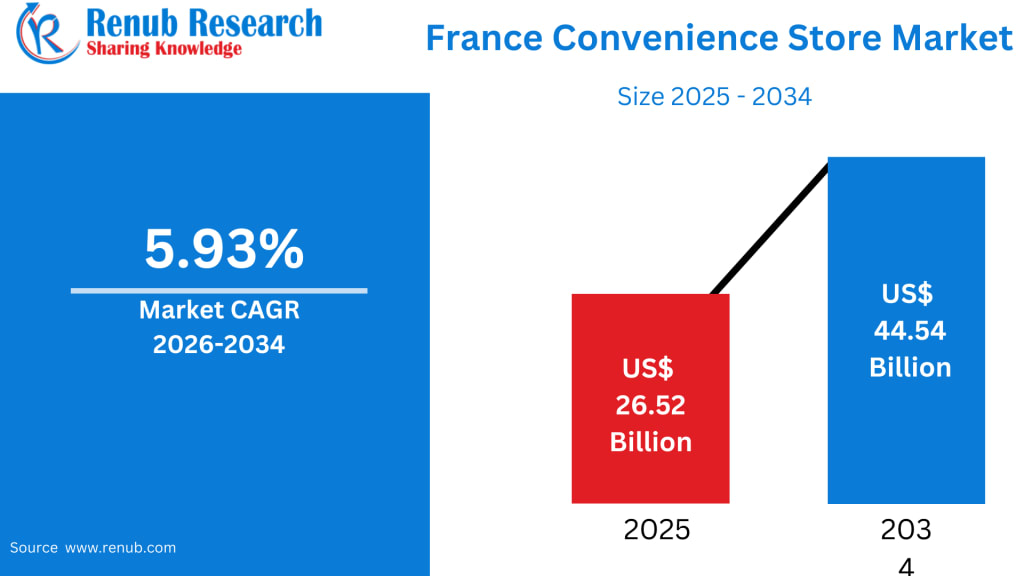

The France Convenience Store Market is poised for strong expansion over the coming decade, reflecting the country’s changing consumer habits, growing urban density, and rising preference for speed, accessibility, and ready-to-consume products. According to Renub Research, the market is expected to grow from US$ 26.52 billion in 2025 to US$ 44.54 billion by 2034, registering a healthy compound annual growth rate (CAGR) of 5.93% from 2026 to 2034.

This growth is fueled by increasing urbanization, higher workforce participation, demand for quick shopping solutions, and expanding acceptance of digital payment methods. From Parisian metro stations to neighborhood corners in Marseille and Strasbourg, convenience stores are becoming an essential part of France’s retail ecosystem. Their evolution from simple “quick-stop” shops into curated micro-retail hubs offering fresh food, local products, and technology-driven services highlights a broader shift in how French consumers approach everyday purchases.

France Convenience Store Market Outlook

Convenience stores are compact, strategically located retail outlets designed to offer essential products quickly and efficiently. Typical offerings include snacks, beverages, packaged foods, personal care items, household necessities, and increasingly, ready-to-eat and fresh food. Their core value lies in speed, proximity, extended operating hours, and ease of access, particularly in high-traffic urban areas, transportation hubs, residential neighborhoods, and tourist districts.

In France, changing lifestyles are accelerating the popularity of this retail format. Professionals, students, commuters, and tourists increasingly favor nearby stores for daily needs rather than making large, infrequent supermarket trips. Growth in single-person households, dual-income families, and time-constrained urban residents further supports this trend. Unlike traditional convenience models, French stores are also incorporating fresh bakery items, organic foods, locally sourced products, and premium ready meals, reflecting national preferences for quality and authenticity.

As urban density increases and consumers value speed alongside product integrity, convenience stores are no longer niche retail outlets—they are becoming central to France’s modern shopping culture.

Market Size and Forecast: Renub Research Insights

Renub Research projects a robust outlook for the France convenience store market:

Market Value (2025): US$ 26.52 Billion

Forecast Value (2034): US$ 44.54 Billion

CAGR (2026–2034): 5.93%

This sustained growth reflects not only rising foot traffic but also expanding product portfolios, technological adoption, and a shift toward higher-margin categories such as ready meals, chilled products, and specialty snacks. The market’s trajectory demonstrates how convenience retail is transitioning from a supplementary format to a strategic pillar of France’s retail economy.

Key Growth Drivers

1. Urbanization and the Shift Toward Speed and Flexibility

France is highly urbanized, with more than 80% of the population living in cities. Major metropolitan centers such as Paris, Lyon, Marseille, and Toulouse are characterized by dense populations, limited living space, and fast-paced lifestyles. These conditions make large, time-consuming supermarket visits less attractive for everyday purchases.

Consumers increasingly prefer short, frequent shopping trips to nearby stores for essential goods, snacks, beverages, and meals. This trend is especially strong among:

Single-person households

Dual-income families

Students and young professionals

Daily commuters

Convenience stores thrive in this environment by offering extended operating hours, strategic locations, and simplified store layouts that allow shoppers to complete purchases within minutes.

2. Rising Demand for Ready-to-Eat, Fresh, and Local Foods

Another major growth driver is the growing appetite for fresh, high-quality, and ready-to-eat foods. French consumers expect convenience without compromising on taste, nutrition, or authenticity. As a result, modern convenience stores increasingly stock:

Freshly baked pastries and bread

Pre-packed salads and sandwiches

Fruit cups and organic snacks

Regional and locally sourced products

This aligns strongly with France’s culinary culture, which prioritizes freshness and provenance. Many convenience stores partner with local bakeries, farms, and specialty suppliers to differentiate themselves from mass-market supermarkets.

In July 2025, bakery supplier Delice de France entered the chilled ready-to-eat segment with its “Delice to Go” modular concept, offering hot, chilled, and ambient grab-and-go items in premium packaging. Such innovations reflect how convenience retail is evolving to meet modern meal habits.

3. Technology Adoption and Digital Payments

Digital transformation is reshaping France’s retail landscape, and convenience stores are at the forefront. Key developments include:

Contactless and mobile payments

Self-checkout systems

Digital loyalty programs

Click-and-collect services

Partnerships with third-party delivery platforms

France is among Europe’s leaders in cashless transactions. A 2025 Payments Europe study found that 71% of French retailers now prefer digital payments over cash, driven by consumer demand for faster, more secure checkout experiences. As consumers embrace card and mobile payments, convenience stores equipped with seamless technology gain a competitive edge by reducing wait times and improving operational efficiency.

Challenges in the France Convenience Store Market

1. High Operating Costs and Competitive Pressure

Despite strong demand, convenience stores face significant cost challenges. Urban locations involve:

High commercial rents

Elevated labor costs

Limited storage and retail space

These factors restrict pricing flexibility, making it difficult to compete with supermarkets and hypermarkets that benefit from economies of scale. Additionally, large retail chains are expanding into urban micro-store formats, intensifying competition.

Regulatory requirements related to labor, food handling, and promotions also add complexity. The primary challenge for operators is to maintain profitability while offering affordable prices, diverse assortments, and premium fresh food.

2. Supply Chain Complexity and Fresh Food Management

Managing fresh and perishable goods presents another operational hurdle. Convenience stores must ensure:

Frequent restocking

Accurate demand forecasting

Minimal food waste

Smaller storage areas heighten the risk of stockouts or spoilage, while urban logistics increase delivery costs. Weather disruptions, supplier delays, and fluctuating demand further complicate inventory planning. Achieving consistent freshness without compromising margins remains one of the sector’s most persistent challenges.

Segment Analysis

France Raw Food Convenience Store Market

Demand for raw and minimally processed foods—such as fruits, vegetables, herbs, and basic cooking ingredients—is rising among health-conscious consumers. Convenience stores capitalize on this by sourcing locally and promoting freshness. Fast restocking, chilled storage, and attractive packaging enable compact stores to serve customers seeking healthy “quick-cooking” options.

France Frozen Food Convenience Store Market

Frozen food is a strong revenue segment due to its longer shelf life and reduced waste. Products such as frozen vegetables, desserts, pastries, and ready meals appeal to time-pressed consumers. Advancements in freezing technology have improved quality and taste, increasing consumer confidence. Frozen foods offer convenience retailers a high-margin, low-spoilage category with growing demand.

France Meat and Poultry Products Convenience Store Market

Packaged meat and poultry products—such as deli meats and ready-to-cook portions—are popular among small households. French consumers demand high standards of quality and sourcing, encouraging stores to partner with trusted suppliers and maintain strict cold-chain controls. While handling perishables is operationally complex, this category remains commercially attractive.

France Cereal-Based Products Convenience Store Market

Bread, pastries, cereals, snack bars, and biscuits form a cornerstone of French convenience retail. Rooted in France’s bakery heritage, this category supports on-the-go consumption. Many stores collaborate with local bakeries to deliver daily-fresh baguettes, croissants, and viennoiseries, while also stocking health-oriented cereal and snack products.

Regional Insights

Paris Convenience Store Market

Paris represents the most competitive and mature convenience store landscape in France. High population density, tourism, and commuter traffic drive strong demand for snacks, beverages, fresh meals, and daily essentials. Extended operating hours and locations near metro stations and business districts ensure consistent footfall. Parisian consumers prioritize organic, premium, and locally sourced products, pushing stores toward higher quality standards.

Marseille Convenience Store Market

Marseille’s market reflects its Mediterranean lifestyle and multicultural population. Stores emphasize fresh produce, value-oriented meals, and diverse cuisine, including North African and Middle Eastern offerings. Proximity to beaches, ports, and tourist areas creates seasonal sales spikes, while urban development and commuter traffic continue to expand demand.

Strasbourg Convenience Store Market

As a European administrative hub and university city, Strasbourg benefits from strong student, tourist, and cross-border traffic. Stores feature bakery items, Alsatian specialties, and health-focused products influenced by neighboring Germany. Compact urban design and pedestrian-friendly zones support dense neighborhood retail networks.

Market Segmentation

By Type:

Raw Food

Canned Food

Frozen Food

Ready-to-Eat

Ready-to-Cook

Others

By Product:

Meat & Poultry Products

Cereal-Based Products

Vegetable-Based Products

Others

By Distribution Channel:

Supermarkets & Hypermarkets

Convenience Stores

Specialty Stores

Others

By City:

Paris, Lyon, Marseille, Toulouse, Bordeaux, Lille, Nantes, Strasbourg, Nice, Montpellier, and Rest of France

Competitive Landscape

The France convenience store market is supported by a global network of food manufacturers and suppliers, each evaluated through Renub Research’s five-viewpoint framework: overview, key personnel, recent developments, SWOT analysis, and revenue analysis.

Key Companies:

Ajinomoto Co., Inc.

Amy’s Kitchen, Inc.

Cargill, Incorporated

Conagra Brands, Inc.

General Mills, Inc.

McCain Foods Limited

Orkla ASA (MTR Foods Pvt. Ltd.)

Nestlé SA

Tyson Foods Inc.

These companies drive innovation in ready meals, frozen foods, packaged snacks, and protein products—core categories fueling convenience store growth.

Final Thoughts

The France Convenience Store Market is entering a new phase of strategic expansion. With market value expected to rise from US$ 26.52 billion in 2025 to US$ 44.54 billion by 2034, the sector reflects broader shifts in consumer behavior—toward speed, quality, digital payments, and localized retail experiences.

Urbanization, demand for fresh and ready-to-eat foods, and technology adoption are reshaping neighborhood retail across French cities. While challenges such as high operating costs and supply chain complexity persist, innovation in product offerings, logistics, and digital services continues to strengthen the market’s foundation.

As convenience stores evolve into curated micro-markets that blend accessibility with premium food culture, they are becoming indispensable to everyday life in France. Over the next decade, their role will expand further—positioning convenience retail not merely as a quick option, but as a defining pillar of France’s modern consumer economy.

About the Creator

jaiklin Fanandish

Jaiklin Fanandish, a passionate storyteller with 10 years of experience, crafts engaging narratives that blend creativity, emotion, and imagination to inspire and connect with readers worldwide.

Keep reading

More stories from jaiklin Fanandish and writers in Futurism and other communities.

United States Canned Food Market Size and Forecast 2026–2034

Introduction: A Quietly Essential Food Category Canned foods have long been part of the American pantry, but their relevance in modern life has evolved far beyond basic food storage. In a country shaped by fast-paced lifestyles, emergency preparedness, and shifting dietary values, canned products now balance convenience with nutrition, sustainability, and innovation. Once viewed primarily as budget staples, today’s canned foods include organic vegetables, gourmet soups, sustainably sourced seafood, and plant-based protein meals—products that align with the expectations of health-conscious and time-pressed consumers alike.

By jaiklin Fanandish3 days ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight11 days ago in Futurism

United States Video Production Market Size and Forecast 2025–2033

United States Video Production Market Outlook The United States video production industry is entering a decade of extraordinary expansion. According to Renub Research, the market is projected to grow from US$ 25.07 billion in 2024 to US$ 181.24 billion by 2033, representing an impressive Compound Annual Growth Rate (CAGR) of 24.58% from 2025 to 2033. This surge reflects more than rising entertainment demand—it highlights a structural transformation in how businesses, educators, governments, and individuals communicate.

By Aaina Oberoia day ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.