Europe Pen Needles Market Poised for Steady Expansion, Reaching US$1.10 Billion by 2031 Amid Diabetes Growth and Home-Care Shift

Rising diabetes prevalence, aging populations, and premium safety innovations redefine value creation in Europe’s pen needles landscape

Europe’s pen needles market is entering a period of sustained, value-driven growth as chronic disease burden, demographic shifts, and home-based care adoption reshape injectable therapy delivery across the region. Valued at US$0.66 billion in 2025, the market increased to US$0.72 billion in 2026 and is projected to expand at a resilient CAGR of 8.9% from 2026 to 2031, reaching a forecasted US$1.10 billion by 2031.

Download PDF Brochure of Europe Pen Needles Market Report

This growth trajectory underscores what is driving demand now: a rising prevalence of diabetes, expanding elderly populations, high obesity rates, and accelerating uptake of insulin and GLP-1 pens—each contributing to higher per-patient needle utilization across Europe’s outpatient and home-care settings.

Why the Market Is Advancing—and Why It Matters Now

Healthcare systems across Europe are facing increasing pressure to manage chronic conditions efficiently while improving patient adherence and comfort. Pen needles, as essential consumables in insulin and GLP-1 therapies, play a critical role in enabling accurate dosing, safe self-administration, and scalable home care. As treatment increasingly shifts away from hospitals toward patient-managed environments, how manufacturers differentiate beyond price has become central to sustaining margins and long-term growth.

Market Snapshot: Where Growth Is Concentrated

France is expected to be the fastest-growing country, registering a CAGR of 9.7%, supported by strong reimbursement frameworks, rising diabetes incidence, and rapid adoption of home-care and e-pharmacy channels.

Key segment insights highlight where volume and value are concentrated:

Standard pen needles dominated the market with an 84.2% share in 2025, reflecting broad compatibility, affordability, and strong reimbursement support.

By length, 8 mm pen needles accounted for 31.1% share in 2024, benefiting from long-standing clinical familiarity and widespread availability.

Insulin therapy is expected to be the fastest-growing application, driven by lifelong injection requirements and the steady expansion of insulin-dependent Type 2 diabetes.

Over-the-counter (OTC) purchases led distribution with a 30.8% share in 2025, enabling immediate access and supporting adherence.

Home-care settings are projected to grow at the highest CAGR of 9.2%, reinforcing the shift toward self-administration and decentralized care.

Competitive Landscape: Leaders, Challengers, and Strategic Focus

The European pen needles market remains highly competitive and increasingly commoditized. Embecta Corp., Novo Nordisk A/S, and B. Braun SE have emerged as star players, supported by broad portfolios, strong operational capabilities, and sustained investment in innovation. At the same time, startups and SMEs such as AdvaCare Pharma, MHC Medical Products, and Wellion are gaining traction through focused product strategies and agile market approaches.

As tender-driven procurement and private-label penetration intensify pricing pressure, who wins going forward will depend on the ability to balance scale with differentiation—particularly in safety, comfort, and sustainability.

Market Dynamics: Drivers, Constraints, and Strategic Openings

The primary growth driver remains the rising prevalence of diabetes, especially insulin-dependent Type 2 diabetes, which continues to expand the base of frequent injection users. Clinicians increasingly favor pen-based delivery for its convenience, dosing accuracy, and reduced administration errors, directly supporting recurring needle demand.

However, the market faces notable restraints. High penetration of low-cost competitors, tender-based commoditization, and reimbursement disparities across countries are compressing pricing power. Additionally, longer-acting injectable therapies are reducing injection frequency for some patients, moderating volume growth.

Against this backdrop, clear opportunities are emerging. Demand is rising for ultra-thin, pain-minimizing, ergonomic, and safety-engineered pen needles that enhance patient comfort and adherence. Sustainability-focused designs, connected or digital-enabled disposables, and OEM partnerships with pen manufacturers are opening new avenues for premiumization, differentiation, and margin protection in a value-driven healthcare environment.

Trends Reshaping Customer and Patient Experience

Innovation in needle geometry, coatings, and ergonomics—combined with strict EU safety standards—is steadily increasing adoption of advanced pen needles. Healthcare professionals are increasingly recommending safety-engineered devices to reduce needlestick injuries, while patients prioritize comfort and ease of use as self-management becomes the norm. The rise of e-pharmacies and home-care delivery models is further transforming how and where pen needles are purchased, distributed, and used.

Strategic Implications for Decision-Makers

For executives across medical devices, pharmaceuticals, and healthcare distribution, why this market matters now is clear. Pen needles may be a mature category, but evolving care models, patient expectations, and regulatory requirements are redefining competitive advantage. Companies that invest in differentiated design, aligned OEM collaborations, and omnichannel distribution strategies stand to secure long-term relevance and resilient growth despite commoditization pressures.

About the Creator

Keep reading

More stories from Juan Martinez and writers in Futurism and other communities.

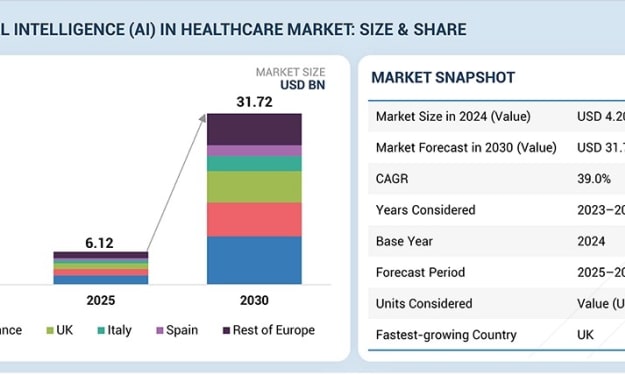

Europe AI in Healthcare Market Set to Surge Toward USD 31.72 Billion by 2030 as Regulation, Cloud Adoption, and Clinical AI Accelerate

Europe’s Artificial Intelligence (AI) in Healthcare market is entering a decisive growth phase, as regulatory clarity, cloud-scale infrastructure, and AI-enabled clinical transformation converge to reshape healthcare delivery across the region. Valued at USD 4.20 billion in 2024, the market expanded to USD 6.12 billion in 2025 and is projected to grow at a robust CAGR of 39.0% from 2025 to 2030, reaching an estimated USD 31.72 billion by 2030.

By Juan Martinezabout 8 hours ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight26 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.