Europe AI in Healthcare Market Set to Surge Toward USD 31.72 Billion by 2030 as Regulation, Cloud Adoption, and Clinical AI Accelerate

Strong regulatory momentum, enterprise-wide AI deployments, and data-sharing initiatives position Europe as a global leader in trustworthy medical AI

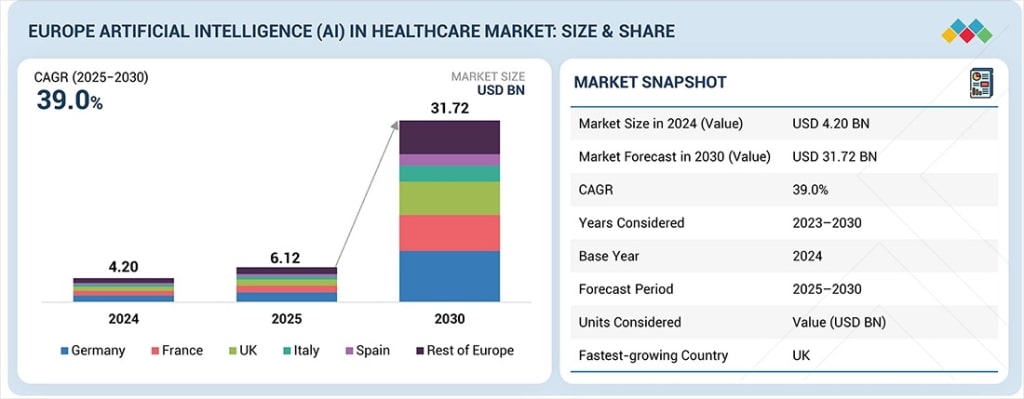

Europe’s Artificial Intelligence (AI) in Healthcare market is entering a decisive growth phase, as regulatory clarity, cloud-scale infrastructure, and AI-enabled clinical transformation converge to reshape healthcare delivery across the region. Valued at USD 4.20 billion in 2024, the market expanded to USD 6.12 billion in 2025 and is projected to grow at a robust CAGR of 39.0% from 2025 to 2030, reaching an estimated USD 31.72 billion by 2030.

Download PDF Brochure of Europe Artificial Intelligence (AI) in Healthcare Market

This acceleration reflects what is changing now in European healthcare: AI is moving from pilot programs to enterprise-grade, compliant deployments that directly address workforce shortages, operational inefficiencies, and rising demand for high-quality, value-based care.

Why This Growth Matters Now

European healthcare systems are under mounting pressure to deliver faster diagnoses, improve clinical outcomes, and maintain sustainability amid staffing constraints. AI-enabled diagnostics, clinical decision support systems, and hospital automation are increasingly viewed as strategic imperatives rather than optional technologies. Regulatory frameworks such as the European AI Act and initiatives like the European Health Data Space (EHDS) are providing the guardrails needed to scale AI adoption responsibly—answering long-standing concerns around safety, transparency, and accountability.

Market Expansion: Who Is Leading and Where Growth Is Concentrated

Germany led the European AI in healthcare market in 2024, accounting for 28.1% of total market share, underscoring its strong digital health infrastructure and early adoption of regulated medical AI solutions. Looking ahead, the UK is expected to register the fastest CAGR, supported by government-backed programs such as the NHS AI Lab and sustained investments in digital health infrastructure.

From a segment perspective:

Integrated AI solutions are forecast to grow at the highest CAGR of 40.6%, as healthcare providers prioritize interoperable, enterprise-wide platforms over standalone tools.

Clinical applications dominated the market in 2024, representing 77.7% of total revenue, reflecting strong uptake of AI in diagnostics, imaging analytics, and clinical workflows.

Diagnosis and early detection is projected to be the fastest-growing functional segment, driven by advances in medical imaging AI and preventive care initiatives.

Cloud-based deployment models are expected to grow at the highest rate, supported by cross-border data-sharing requirements and faster scalability.

Machine learning, particularly deep learning, continues to dominate as the core enabling technology due to its ability to process large volumes of unstructured clinical and imaging data.

Healthcare providers, especially hospitals and clinics, remain the largest end users as they modernize diagnostics, surgical planning, and patient management systems.

How Regulation Is Shaping Competitive Advantage

The European AI Act is emerging as a powerful market catalyst. By classifying many medical AI systems—particularly in radiology and diagnostics—as high-risk, the regulation is increasing demand for compliant, auditable, and transparent AI solutions aligned with both the AI Act and the EU Medical Device Regulation (MDR). Vendors that can demonstrate strong clinical evidence, model interpretability, and continuous performance monitoring are gaining faster adoption and deeper trust among healthcare buyers.

At the same time, regulatory complexity remains a restraint. Dual compliance with MDR and the AI Act has raised certification burdens, particularly for startups, as notified bodies face capacity constraints. This dynamic is reshaping vendor strategies, favoring partnerships, consolidation, and platforms that can scale compliance across markets.

EHDS: Unlocking Pan-European Validation and Trust

The European Health Data Space represents a critical opportunity for the industry. By enabling secure, cross-border access to structured health and imaging data, EHDS allows AI vendors to conduct pan-European validation studies, strengthen regulatory evidence, and improve model generalizability across diverse populations and clinical environments. This development directly addresses one of the sector’s core challenges—performance variability across scanners, sites, and protocols—and positions Europe as a global benchmark for ethics-driven, evidence-based medical AI.

Competitive Landscape: Established Leaders and Emerging Innovators

The competitive environment is defined by a mix of global technology leaders and agile innovators. Koninklijke Philips N.V., Siemens Healthineers AG, and GE Healthcare are recognized as star players, leveraging extensive clinical ecosystems, broad AI portfolios, and deep hospital partnerships across Europe. At the same time, startups and SMEs such as Qure.ai and Healx are gaining traction in specialized niches, highlighting the market’s openness to innovation where clinical value and compliance align.

Strategic collaborations, federated learning advancements, and cross-border data initiatives are rapidly reshaping competitive dynamics—raising the bar for scalability, interoperability, and regulatory readiness.

Strategic Implications for Decision-Makers

For CEOs, CFOs, and digital health leaders, the message is clear: AI in healthcare is becoming a core infrastructure investment in Europe. Success will depend on aligning technology roadmaps with regulatory compliance, prioritizing cloud-ready and interoperable platforms, and building partnerships that accelerate validation and deployment at scale. Organizations that move early to integrate compliant AI into clinical workflows stand to gain measurable advantages in efficiency, quality of care, and long-term cost control.

About the Creator

Keep reading

More stories from Juan Martinez and writers in Futurism and other communities.

U.S. Pen Needles Market on Track to Reach USD 1.53 Billion by 2031 as Home-Based Diabetes Care and Device Innovation Accelerate

The U.S. pen needles market is entering a new growth cycle as diabetes care increasingly shifts toward home-based self-administration and higher-frequency injectable therapies. Valued at USD 0.85 billion in 2025 and USD 0.93 billion in 2026, the market is projected to expand at a CAGR of 10.4% from 2026 to 2031, reaching USD 1.53 billion by the end of the forecast period. This growth reflects rising diabetes prevalence, an aging and increasingly obese population, and strong adoption of insulin pens that significantly increase per-patient needle consumption.

By Juan Martinezabout 11 hours ago in Futurism

About Binding Prometheus

I want to start actively advocating on behalf of my own work, and the most valuable part of my canon is, without a doubt, Binding Prometheus, the play I have been working on since 2019 and only finished in 2023 as part of my MA. The play itself is an amalgamation of a million different inspirations. On one end, it evokes the Ancient Greek myth-play, deriving its own title from the earliest extant work of Western drama we have, Aeschylus’s Prometheus Bound. On the other end, it borrows significantly from the sci-fi bulwarks from over the years, namely Mary Shelley’s Frankenstein and Karel Capek’s Rossum’s Universal Robots. The play could be an episode of Black Mirror, I fear. I don’t know. I’ve only ever seen one episode of Black Mirror.

By Steven Christopher McKnight26 days ago in Futurism

Saudi Arabia Specialty Chemicals Market: Industrial Diversification & Demand Growth

According to IMARC Group's latest research publication, Saudi Arabia specialty chemicals market size reached USD 7,543.9 Million in 2025. The market is projected to reach USD 10,701.6 Million by 2034, exhibiting a growth rate (CAGR) of 3.96% during 2026-2034.

By Faisal Al-Harbiabout 14 hours ago in Futurism

The Duelist

The rays of a dying red sun flashed against the onrushing blade. The grey beards say the key to dueling lies in size, speed, reach, righteous fury, whatever the person in front of them pays them to say. Matteo knew better than any it was none of these and had an undefeated record on these sands to prove it.

By Matthew J. Fromm2 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.