China Hotel Market Set for a Tourism-Led Boom Through 2033

Rising Domestic Travel, Expanding Middle Class, and Global Brands Power China’s Hotel Industry Toward a US$ 170.40 Billion Future

China Hotel Market: Size, Growth, and Outlook

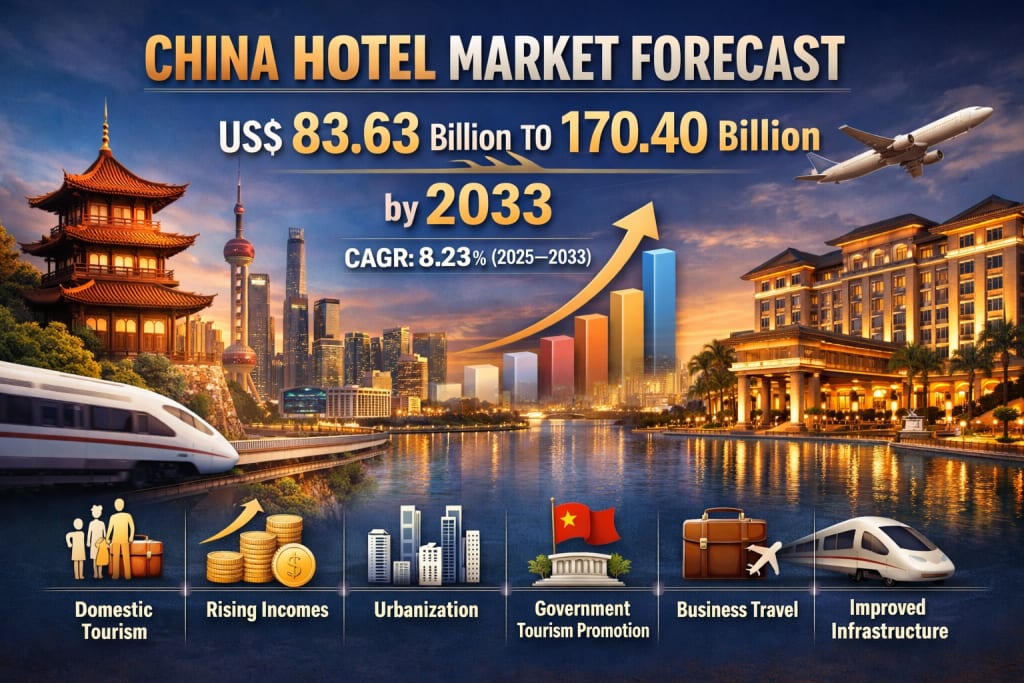

China’s hotel industry is entering a powerful new growth phase, supported by a resurgence in travel, rising incomes, and continuous infrastructure development. According to Renub Research, the China Hotel Market is expected to reach US$ 170.40 billion by 2033, up from US$ 83.63 billion in 2024, registering a compound annual growth rate (CAGR) of 8.23% from 2025 to 2033.

This impressive expansion reflects more than just a post-pandemic recovery. It signals a structural shift in how Chinese consumers travel, spend, and experience hospitality. Increased domestic tourism, rapid urbanization, government-backed tourism promotion programs, better transportation infrastructure, and the steady expansion of foreign business travel are collectively reshaping the country’s hotel landscape.

From luxury five-star properties in tier-one cities to budget hotels in emerging urban clusters and tourist hubs, China’s hospitality sector is becoming more diverse, competitive, and experience-driven. The result is a market that is not only growing in size but also evolving in quality, service models, and customer expectations.

Overview of the China Hotel Industry

Over the past decade, China’s hospitality industry has grown at an extraordinary pace. The country’s massive population, rising middle class, rapid economic development, and increasing integration with global trade and tourism have made it one of the most attractive hotel markets in the world.

Both international and domestic hotel groups have aggressively expanded their footprints across China. Global brands see the country as a long-term growth engine, while Chinese hotel chains continue to professionalize, scale up, and adopt more sophisticated management and digital strategies.

One of the most important trends shaping the market is the rise of domestic travel. More Chinese consumers are traveling within the country for leisure, family visits, business, and short breaks. This has created sustained demand across all hotel categories—high-end, mid-range, and budget.

At the same time, urbanization and infrastructure development have improved access to both major cities and previously hard-to-reach tourist destinations. High-speed rail networks, modern airports, and upgraded highways are making travel faster, cheaper, and more convenient, directly boosting hotel occupancy and encouraging new hotel investments.

Additionally, the growth of business travel and MICE (Meetings, Incentives, Conferences, and Exhibitions) tourism is strengthening demand in major commercial and industrial centers. As China continues to play a central role in global manufacturing, trade, and technology, the need for quality business accommodations is rising steadily.

Key Growth Drivers of the China Hotel Market

1. Rising Domestic Tourism

The most powerful engine behind the China hotel market’s growth is the surge in domestic tourism. As incomes rise and lifestyles change, more Chinese consumers are prioritizing travel for leisure, wellness, family bonding, and cultural exploration.

China is now one of the world’s largest travel markets, and tourism has become a major contributor to the national economy. In 2023, travel and tourism contributed a substantial share to the country’s GDP, underlining just how strategically important this sector has become.

Following the lifting of pandemic-era travel restrictions, domestic tourism rebounded sharply. Industry reports showed a strong recovery, with travel activity rising dramatically as people returned to exploring cities, cultural sites, natural attractions, and entertainment destinations across the country.

This rebound has had a direct and positive impact on hotels. From city hotels and resort properties to budget accommodations near transport hubs, demand has increased across the board. Travelers are also becoming more segmented in their preferences—some seek affordable and functional stays, while others are willing to pay a premium for luxury, experiences, and branded comfort. This diversification is helping the hotel market grow not just in volume, but also in depth and value.

2. Improved Infrastructure and Connectivity

China’s massive investment in infrastructure continues to be a game-changer for the hospitality sector. The expansion of high-speed rail networks, airports, metro systems, and expressways has transformed how people move across the country.

Destinations that were once considered remote are now accessible within hours. This improved connectivity has unlocked new tourism corridors and encouraged hotel development in secondary and tertiary cities, scenic regions, and emerging business hubs.

Better infrastructure does more than just move people—it reduces travel friction, increases trip frequency, and supports shorter, more spontaneous trips. All of these trends directly translate into higher demand for hotel rooms.

For hotel operators, improved infrastructure also reduces operational challenges and makes it easier to scale networks across regions. As a result, both domestic and international hotel groups are more confident in expanding their presence across different parts of China.

3. Expanding Presence of Global Hotel Brands

Another major growth driver is the continued expansion of international hotel chains in China. Global brands are increasingly targeting the country to serve both international travelers and a growing base of Chinese consumers who value branded experiences, consistent service standards, and loyalty programs.

International hotel groups bring with them strong brand recognition, advanced management systems, and global best practices. This raises overall service quality in the market and intensifies competition, pushing both foreign and domestic players to innovate.

The opening of new branded properties in major cities and tourist destinations reflects the long-term confidence global players have in China’s hospitality sector. This trend is also helping to elevate China’s position as a premium travel destination, especially for high-end leisure and business travelers.

Challenges Facing the China Hotel Market

1. Intense Competition

With the rapid expansion of both domestic and international hotel brands, competition in China’s hotel market is fierce. In many cities, travelers can choose from a wide range of properties across all price segments.

This intense competition puts pressure on pricing, margins, and occupancy rates. Hotels are forced to differentiate themselves through better locations, superior service, unique design, digital convenience, and personalized guest experiences. While this ultimately benefits consumers, it increases operational complexity and requires continuous investment from hotel operators.

2. Overcapacity in Certain Regions

In some markets, especially fast-developing urban and tourist areas, overcapacity has become a real concern. The rapid pace of hotel construction has, in certain locations, outstripped demand growth.

Overcapacity can lead to lower occupancy rates, aggressive discounting, and reduced profitability. It also makes market entry more challenging for new players and increases the risk profile for investors. Managing supply growth in line with realistic demand projections will be crucial for the long-term health of the industry.

China Hotel Market Segmentation

The China hotel market is highly diversified and segmented to reflect different traveler needs, budgets, and travel purposes.

By Type:

High-End

Mid-End

Budget

By Business Model:

Chain

Independent

By Sales Channel:

Offline

Online

By End User:

Leisure FIT & Group

Corporate

MICE

Others

By Age Group:

18–24 years

25–34 years

35–44 years

45–54 years

55–64 years

By Gender:

Male

Female

By Star Rating:

1 Star

2 Star

3 Star

4 Star

5 Star

This segmentation highlights how broad and dynamic the Chinese hotel market has become. Growth opportunities exist across virtually all categories, from economy hotels catering to young travelers to luxury resorts targeting affluent domestic and international guests.

Competitive Landscape and Key Players

The China hotel market features a mix of powerful domestic groups and leading global hospitality brands. Competition is centered on scale, brand strength, location strategy, digital capabilities, and customer loyalty.

Some of the key players operating in the market include:

Marriott International Inc.

Huazhu Hotels Group Ltd

Zhejiang New Century Hotel Management Co. Limited

Expedia Group Inc.

Guangdong International Hotel Management Holdings Ltd.

Huangshan Tourism Development Co. Ltd.

InterContinental Hotels Group PLC

Shanghai Jin Jiang International Hotels (Group) Company Limited

Tongcheng Travel Holdings Ltd.

Emei Shan Tourism Co., Ltd.

These companies compete across multiple dimensions, including property expansion, brand portfolio diversification, technology adoption, and partnerships with travel platforms. Many are also investing heavily in digital booking systems, loyalty programs, and data-driven pricing strategies to strengthen their market positions.

Digitalization and Changing Consumer Behavior

One of the most important structural shifts in China’s hotel market is the rapid digitalization of travel planning and booking. Online travel agencies, mobile apps, and super-platform ecosystems have become central to how consumers search, compare, and book accommodations.

Younger travelers, in particular, are highly price-sensitive, review-driven, and experience-focused. They expect seamless digital experiences, fast check-ins, flexible cancellations, and personalized offers. Hotels that fail to adapt to these expectations risk losing visibility and relevance.

At the same time, social media and content platforms are increasingly influencing travel decisions, turning hotels into not just places to stay, but also lifestyle and experience brands.

Future Outlook: What Lies Ahead for China’s Hotel Industry?

Looking ahead to 2033, the outlook for the China hotel market remains strongly positive. The projected growth to US$ 170.40 billion reflects confidence in the long-term fundamentals of the sector: a huge domestic market, rising incomes, ongoing urbanization, and China’s central role in regional and global travel.

However, growth will not be uniform. Winners will likely be those operators who can:

Manage capacity and pricing discipline

Differentiate through service, branding, and experience

Leverage digital platforms and data analytics

Adapt to evolving traveler preferences

Balance expansion with profitability

Sustainability, smart hotel technologies, and experience-driven hospitality are also expected to play a bigger role in shaping future investment and development strategies.

Final Thoughts

China’s hotel industry is no longer just about adding more rooms—it is about building smarter, more differentiated, and more customer-centric hospitality ecosystems. With the market set to nearly double in value from US$ 83.63 billion in 2024 to US$ 170.40 billion by 2033, the opportunities are enormous, but so are the competitive pressures.

Driven by domestic tourism, infrastructure growth, and the expanding presence of global brands, China’s hotel market is entering a new era of maturity and sophistication. For investors, operators, and industry stakeholders, the coming decade will be defined not just by growth, but by how well they adapt to a faster, more digital, and more experience-focused travel economy.

About the Creator

AI in Fintech Market: Fraud Detection Innovation, Risk Analytics & Market Forecast

According to IMARC Group's latest research publication, the global AI in fintech market size reached USD 17.64 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 97.70 Billion by 2034, exhibiting a growth rate of 19.90% during 2026-2034.

By sujeet. imarcgroupabout 13 hours ago in Futurism

Autocatalyst Industry in Saudi Arabia: Stricter Emission Norms, Automotive Production & Market Expansion

According to IMARC Group's latest research publication, Saudi Arabia autocatalyst market size reached USD 131.3 Million in 2025. The market is projected to reach USD 173.4 Million by 2034, exhibiting a growth rate of 3.14% during 2026-2034.

By Kishan Kumarabout 10 hours ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.