Autocatalyst Industry in Saudi Arabia: Stricter Emission Norms, Automotive Production & Market Expansion

How stricter emission regulations, rising vehicle production, and demand for cleaner mobility solutions are driving innovation and growth across Saudi Arabia’s autocatalyst market.

According to IMARC Group's latest research publication, Saudi Arabia autocatalyst market size reached USD 131.3 Million in 2025. The market is projected to reach USD 173.4 Million by 2034, exhibiting a growth rate of 3.14% during 2026-2034.

How AI is Reshaping the Future of Saudi Arabia Autocatalyst Market

- Predictive Quality Control: AI-powered imaging systems monitor autocatalyst coating uniformity and precious metal loading in real-time during manufacturing, reducing defects and optimizing platinum, palladium, and rhodium usage to cut material costs.

- Smart Precious Metal Recovery: Machine learning algorithms optimize catalyst recycling processes, achieving recovery rates above ninety percent for platinum group metals from spent converters while predicting optimal processing times based on catalyst age and composition.

- AI-Driven Materials Optimization: Advanced algorithms simulate thousands of catalyst formulations virtually, identifying optimal platinum-palladium substitution ratios that maintain emission control performance while responding to fluctuating precious metal prices and supply constraints.

- Intelligent Supply Chain Management: AI platforms forecast PGM price movements and demand patterns, helping manufacturers hedge against volatility in rhodium and palladium markets while optimizing inventory levels and procurement timing across global supply networks.

Request a Sample Report with the Latest Market Data & Outlook

How Vision 2030 is Revolutionizing Saudi Arabia Autocatalyst Industry

Vision 2030's environmental sustainability objectives and industrial diversification goals are fundamentally reshaping the autocatalyst landscape. The Kingdom targets limiting passenger vehicle emissions to one hundred twenty-two grams of carbon dioxide per kilometer, driving demand for advanced catalytic converters. National fuel economy standards aim for nineteen kilometers per liter fleet average, requiring sophisticated emission control technologies as vehicles achieve greater efficiency. Saudi Green Initiative commitments to reduce two hundred seventy-eight million tons of carbon dioxide equivalent emissions annually position autocatalysts as critical environmental compliance tools. Government investments in renewable energy infrastructure reaching three point seven gigawatts installed capacity signal broader decarbonization priorities that extend into transportation. Localization initiatives under economic diversification programs encourage domestic autocatalyst manufacturing capabilities, reducing import dependence while creating specialized employment opportunities aligned with national transformation goals.

Saudi Arabia Autocatalyst Market Trends & Drivers:

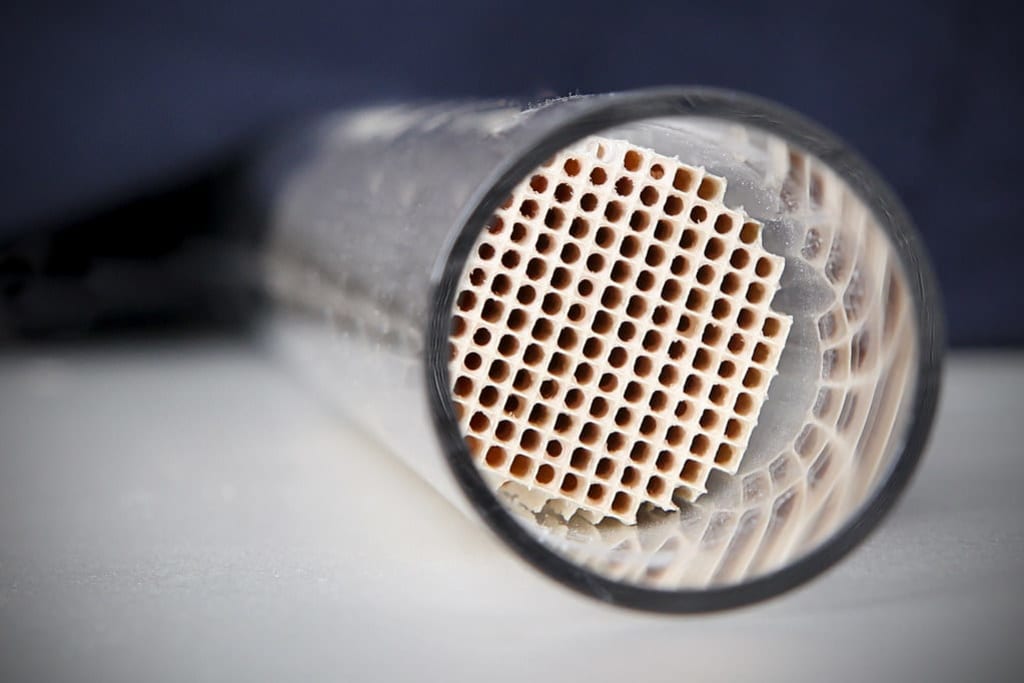

Vehicle production momentum is accelerating market expansion as domestic assembly operations scale up. The Saudi car market surged seven point eight percent in volume representing the strongest performance in eight straight years. Hyundai and Kia manufacturing facilities in Jeddah are ramping production alongside expanding Toyota operations meeting both local demand and export requirements to neighboring GCC markets. Rising assembly volumes create direct OEM autocatalyst demand while supporting aftermarket segment growth as the national vehicle fleet expands. Government localization mandates incentivize automakers to source emission control components domestically, encouraging international catalyst manufacturers to establish partnerships with Saudi suppliers. The shift toward SUVs and pickup trucks, which require larger catalyst systems to meet emission standards, boosts market value despite potentially slower unit growth. New manufacturing plants implementing stricter quality standards demand advanced three-way and four-way catalytic converters incorporating optimized precious metal loadings to balance performance against cost pressures from volatile palladium and rhodium prices.

Stringent emission regulations are driving technology upgrades across the vehicle population. The Kingdom established Corporate Average Fuel Economy standards targeting four percent annual efficiency improvements lifting fleet economy from twelve to nineteen kilometers per liter. GCC Standardization Organization technical regulations mandate Euro 6-equivalent emission limits for new vehicles sold throughout the region, requiring sophisticated autocatalysts with precise platinum group metal formulations. As Saudi Arabia targets thirty percent clean fuel vehicle sales in Riyadh, hybrid models entering the market demand specialized catalytic systems capable of cold-start emission control during frequent engine cycling. Government vehicle scrappage incentives removing older vehicles meeting China 4 standards accelerate fleet turnover, replacing basic two-way catalysts with advanced three-way systems. Inspection programs enforcing emission compliance create aftermarket demand for catalyst replacement when systems deteriorate beyond performance thresholds. The regulatory framework aligns with Saudi Green Initiative carbon reduction targets, ensuring sustained pressure for emission control technology adoption across gasoline, diesel, and emerging hybrid powertrains.

Precious metal market dynamics are reshaping catalyst formulation strategies and supply chain approaches. Platinum prices trading at premiums to palladium reversed historical relationships, encouraging reverse substitution where platinum replaces palladium in gasoline applications without compromising catalytic efficiency. Rhodium stabilized in the four thousand four hundred to four thousand eight hundred dollar range after Chinese glass industry liquidations, supporting steady industrial demand despite automotive sector pressures. Secondary supply from autocatalyst recycling improved as higher PGM prices incentivized spent converter collection, with recovery operations achieving processing efficiencies above ninety percent for platinum group metal extraction. Manufacturers increasingly optimize washcoat formulations to minimize rhodium loadings, the scarcest and costliest PGM, while maintaining nitrogen oxide conversion capabilities. Strategic relationships with South African and Russian PGM producers ensure supply continuity amid geopolitical uncertainties affecting thirty percent of global palladium output. Technology partnerships with catalyst innovators like BASF and Johnson Matthey enable access to advanced formulations achieving emission compliance with reduced precious metal content.

Saudi Arabia Autocatalyst Market Industry Segmentation:

The report has segmented the market into the following categories:

Material Insights:

- Platinum

- Palladium

- Rhodium

- Others

Catalyst Type Insights:

- Two-way

- Three-way

- Four-way

Distribution Channel Insights:

- OEM

- Aftermarket

Vehicle Type Insights:

- Passenger Car

- Light Commercial Vehicle

- Heavy Commercial Vehicle

- Others

Fuel Type Insights:

- Gasoline

- Diesel

- Hybrid Fuels

- Hydrogen Fuel Cell

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

Competitive Landscape:

The competitive landscape of the industry has also been examined along with the profiles of the key players.

Recent News and Developments in Saudi Arabia Autocatalyst Market

- November 2025: Saudi Green Initiative reaffirmed commitments to reduce two hundred seventy-eight million tons of carbon dioxide equivalent emissions annually, strengthening regulatory framework supporting autocatalyst adoption across transportation sector decarbonization efforts.

- October 2025: GCC Standardization Organization maintained Euro 6-equivalent emission standards for new vehicles sold throughout the region, sustaining demand for advanced three-way and four-way catalytic converters with optimized precious metal formulations.

- September 2025: The Saudi car market achieved seven point eight percent year-over-year volume growth representing the strongest annual performance in eight consecutive years, driving increased OEM autocatalyst demand across expanding domestic vehicle assembly operations.

- August 2025: Platinum and palladium markets experienced pricing dynamics shifts as platinum traded at average premiums of fifty-nine dollars per ounce over palladium, encouraging reverse substitution strategies in gasoline catalyst formulations across automotive manufacturers.

- June 2025: Major autocatalyst manufacturers including BASF, Johnson Matthey, and Umicore maintained focus on Middle Eastern markets with advanced catalyst technologies optimized for regional fuel quality specifications and extreme temperature operating conditions.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Kishan Kumar

My name is Kishan Roy and I am a market analyst having 5 years of experience and a skilled researcher with a keen eye for consumer trends and data-driven insights.

Keep reading

More stories from Kishan Kumar and writers in Futurism and other communities.

Saudi Arabia Healthcare IT Market: Digital Transformation, AI Integration & Growth Outlook

According to IMARC Group's latest research publication, Saudi Arabia healthcare IT market size reached USD 3.3 Billion in 2024. The market is projected to reach USD 7.7 Billion by 2033, exhibiting a growth rate of 8.9% during 2025-2033.

By Kishan Kumarabout 12 hours ago in Futurism

Organic Demand and Packed Innovations Drive Coconut Water Market Growth

The global coconut water market size was valued at USD 5.69 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 13.98 Billion by 2034, exhibiting a CAGR of 10.50% during 2026-2034. North America currently dominates the market, holding a significant coconut water market share of over 28.9% in 2025.

By Frank Morganabout 15 hours ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.