Bunker Fuel Market Trends: LNG Adoption, Decarbonization Efforts & Forecast to 2034

How LNG adoption, IMO emission regulations, and decarbonization targets are reshaping fuel choices and investment strategies in the global bunker fuel market

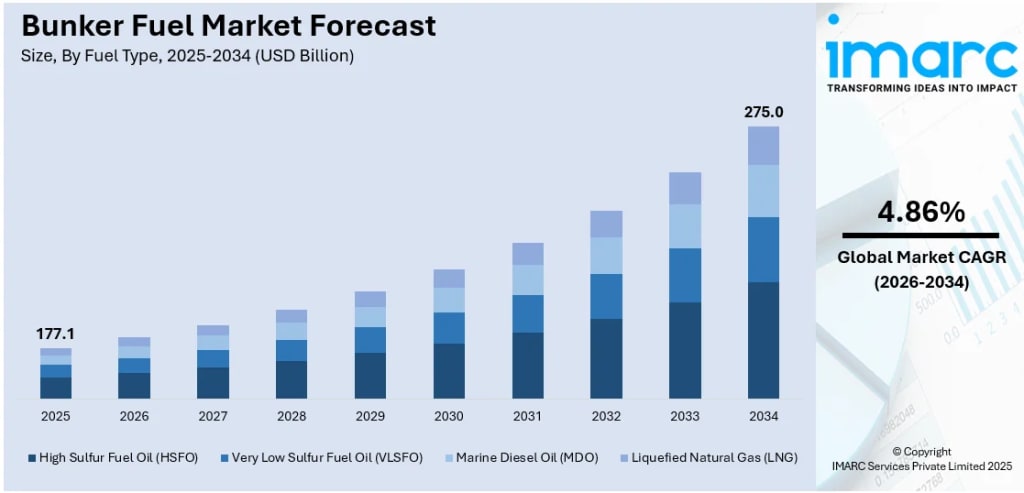

Expanding global maritime trade, stringent environmental regulations, and rising adoption of cleaner fuel alternatives are driving steady growth in the bunker fuel market, supported by port infrastructure expansion, IMO sulfur cap compliance, and increasing investment in LNG bunkering facilities worldwide. According to IMARC Group's latest data, the global bunker fuel market size was valued at USD 168.59 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 268.92 Billion by 2033, exhibiting a CAGR of 5.06% during 2025-2033. Asia-Pacific currently dominates the market, holding a market share of 45.6% in 2024.

Bunker fuel remains the backbone of global shipping, powering the vessels that move over 80% of global trade by volume. The industry is in the middle of a major transition, driven by environmental regulations that have fundamentally changed what can be burned at sea. Very low sulfur fuel oil (VLSFO) now accounts for 43.2% of the market by fuel type, a direct result of the IMO 2020 sulfur cap that limited sulfur content to 0.5%. Container vessels lead by vessel type with 40.0% share, reflecting the massive volume of consumer goods, electronics, and manufactured products moving through global supply chains.

Bunker Fuel Market Growth Drivers:

- IMO Regulations Reshaping Fuel Demand and Compliance Costs

The International Maritime Organization's 2020 sulfur cap changed the entire market overnight. Ships were forced to either switch to VLSFO, install scrubbers to keep using high sulfur fuel oil, or move to alternative fuels like LNG. VLSFO became the default choice for most operators, now representing the largest fuel type segment. According to VPS laboratories, VLSFO accounted for 54.3% of marine fuels tested, followed by high sulfur fuel oil at 29.5% and marine gas oil at 14.2%. In January 2025, the U.S. Treasury and IRS released guidance on Section 45Z, offering tax credits for producing transportation fuels with reduced lifecycle greenhouse gas emissions, including marine fuels. These regulations are not just environmental measures they directly shape purchasing decisions, infrastructure investment, and long-term fleet planning.

- Global Maritime Trade Expansion Driving Consistent Fuel Demand

Seaborne trade continues growing steadily. According to UNCTAD, maritime trade volumes expanded 2% in 2024, with containerized trade up 3.5%. Between 2025 and 2029, total seaborne trade is projected to grow at an average rate of 2.4% annually. Over 11.5 billion metric tons of goods were loaded globally, including 7.2 billion metric tons of dry cargo and 2 billion metric tons of crude oil. This volume translates directly into fuel consumption. As e-commerce expands, container shipping already the largest vessel type segment at 40.0% keeps growing. Every container ship running between Asia and Europe or Asia and North America needs reliable fuel supply at multiple ports, and that demand is not slowing down.

- Infrastructure Investment in LNG Bunkering and Alternative Fuels

LNG as a bunker fuel is growing fast, though still a small share of the overall market. In May 2024, EXP and Galveston LNG Bunker Port announced plans to build an LNG bunkering facility in Galveston, Texas, capable of producing 600,000 gallons per day to serve vessels across the Gulf of Mexico. In July 2025, Hyundai Glovis completed its first LNG bunker lift from Shell in Singapore, marking another step in the industry's shift toward lower-emission fuels. In January 2024, Shell and TotalEnergies announced a joint venture to develop and operate a new LNG bunkering vessel, aimed directly at reducing emissions. These are not pilot projects they represent billions in infrastructure investment aimed at building out a parallel fuel supply chain alongside traditional bunker fuel.

Bunker Fuel Market Trends:

- Digital Platforms Bringing Transparency to Fuel Procurement

Bunker fuel procurement has historically been opaque, with pricing, quality, and availability often unclear until the transaction is complete. That is changing. In March 2025, Hafnia partnered with Studio 30 50 to launch FuelSure, a digital platform that integrates real-time data to improve transparency, accountability, and cost efficiency in bunker fuel transactions. These platforms allow ship operators to compare suppliers, lock in pricing, verify fuel quality, and manage compliance documentation all in one place. As margins tighten and regulatory scrutiny increases, having accurate data at the point of purchase is becoming a competitive advantage rather than a luxury.

- Carbon Capture and Biofuels Entering Commercial Deployment

Alternative fuels are moving from concept to commercial operation. In March 2024, ExxonMobil received approval from the U.S. Maritime Administration to build the first large-scale commercial carbon capture utilization and storage (CCUS) facility for bunker fuel at its Baytown, Texas refinery, expected to reduce maritime carbon emissions by approximately 1 million metric tons annually. In 2023, BP supplied B30 biofuel a blend of 30% fatty acid methyl ester and VLSFO to Anglo American's marine fleet in Australia, helping reduce the mining company's carbon footprint from shipping operations. Biofuels accounted for just 0.8% of tested marine fuels, but that number is climbing as companies face increasing pressure to cut emissions.

- Strategic Partnerships and Fleet Modernization Driving LNG Adoption

Major shipping lines and fuel suppliers are forming long-term partnerships to secure LNG supply and accelerate fleet transitions. In May 2024, BP and Mitsui O.S.K. Lines signed an MOU to collaborate on developing a new LNG bunkering vessel. In July 2024, MOL invested in Carnot, a startup building heat-resistant engine technology that improves fuel efficiency and lowers greenhouse gas emissions. In November 2024, Maersk converted a large container vessel to a dual-fuel methanol engine, directly addressing climate goals while maintaining operational flexibility. In October 2024, Bunker One announced it would launch LNG bunker supply in Northwestern Europe by early 2025, expanding its portfolio to include physical LNG and liquefied bio methane. These moves reflect a broader industry shift toward diversified fuel strategies rather than reliance on a single fuel type.

Recent News and Developments in Bunker Fuel Market

- March 2025: Hafnia partnered with Studio 30 50 to launch FuelSure, a digital platform designed to integrate real-time data for enhanced transparency, accountability, and cost efficiency in the maritime bunker fuel market. The platform addresses long-standing issues around pricing visibility and quality assurance, giving ship operators better tools to manage procurement and regulatory compliance in an increasingly complex fuel landscape.

- January 2025: The U.S. Treasury and IRS released guidance on Section 45Z, establishing tax credits for producing transportation fuels including sustainable aviation fuel and marine fuels with reduced lifecycle greenhouse gas emissions. The policy is aimed at incentivizing cleaner fuel production and accelerating the maritime industry's transition away from high-emission bunker fuels, particularly in U.S. ports and shipping lanes.

- July 2025: Hyundai Glovis completed its first LNG bunker lift from Shell at Singapore, marking a significant operational milestone in the company's shift toward lower-emission marine fuels. The transaction reflects broader momentum in Asia-Pacific toward LNG bunkering infrastructure, with Singapore positioning itself as a central hub for alternative marine fuel supply in the region.

- October 2024: ABS granted Approval in Principle (AiP) to VARD for an ammonia bunkering barge developed by the RADIUS consortium. The barge is designed to be compatible with vessels like Höegh's Aurora Class and MMMCZCS's 15,000 TEU container ship, with operations targeted for 2030 along the U.S. East Coast. The approval reflects growing industry interest in zero-carbon fuel alternatives beyond LNG, positioning ammonia as a potential long-term solution for deep-sea shipping decarbonization.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Suhaira Yusuf

I specialize in Consumer Insights, focusing on transforming detailed market data into strategic business solutions that accelerate growth and improve customer engagement.

Keep reading

More stories from Suhaira Yusuf and writers in Futurism and other communities.

Aquaculture Market Trends: Rising Fish Consumption, Export Demand & Forecast to 2034

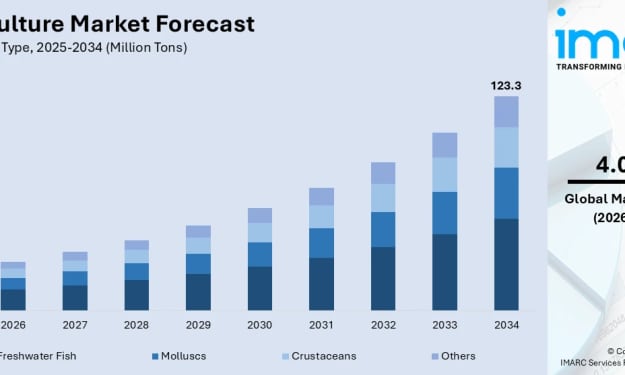

Rising global demand for seafood, declining wild fish stocks, and growing awareness of aquaculture's nutritional benefits are driving steady expansion in the market, supported by technological advances in farming practices, sustainable production methods, and increasing protein consumption in emerging economies. According to IMARC Group's latest data, the global aquaculture market size was valued at 82.8 Million Tons in 2024. Looking forward, IMARC Group estimates the market to reach 122.9 Million Tons by 2033, exhibiting a CAGR of 4.03% during 2025-2033. Asia-Pacific currently dominates the market, holding a market share of over 90.7% in 2024.

By Suhaira Yusufabout 11 hours ago in Futurism

Green Hydrogen Market Report: Decarbonization Trends & Growth Outlook

According to IMARC Group's latest research publication, global green hydrogen market size was valued at USD 2,477.8 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 68,257.4 Million by 2034, exhibiting a growth rate (CAGR) of 44.55% during 2026-2034.

By sujeet. imarcgroupabout 14 hours ago in Futurism

In-vitro Colorectal Cancer Screening Tests Market Outlook: Early Detection Demand and Growth Opportunities

According to IMARC Group's latest research publication, The global in-vitro colorectal cancer screening tests market size was valued at USD 1,049.22 Million in 2024. The market is projected to reach USD 1,658.67 Million by 2033, exhibiting a CAGR of 4.96% from 2025-2033.

By Michael Richard7 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.