Term Insurance क्या होता है? – How to Buy Best Term Insurance Plan in India in 2023?

Understanding Term Insurance: A Guide to Buying the Best Term Insurance Plan in India in 2023

Friends, when we think of taking life insurance, it creates a lot of confusion

So many different questions start popping. A very important question is whether we should take life insurance or not? Is life insurance suitable for my profile or not? Many people don't even think about this. The second question is, which insurance is best if we decide to take it? Term Insurance, Endowment policy, or ULIP? When should we take life insurance? How can we choose the best life insurance and what are all the parameters to check? Should we pay a single, regular premium or for a limited time? And when all the points are clear, we think that whether we should discontinue our existing policy or not?

I'm going to answer all these important questions in this article so that whenever you go to buy life insurance, your life becomes easy. This article is going to be interesting, so stay tuned!

Who Should Buy Life Insurance?

Let's address the most important question first - who should buy life insurance and who doesn't even need it? To understand this, let's consider a hypothetical example. Let's assume Rahul is a healthy person doing his job. He thinks that if by chance he dies in the future, his family doesn't have to compromise on their lifestyle and their financial situation doesn't get bad. For this, he wants to buy insurance, which is the main purpose of insurance. So now a question arises - should Rahul buy life insurance or not? It depends mainly on two factors related to his financial situation.

The first factor is Rahul's income and his family income. Rahul might have his parents, wife, and two kids. His wife and parents might be working, and their family income might be good. The second factor is their expenses. If the family income (excluding Rahul's income) is more than their expenses, then they aren't dependent on Rahul, and they are financially independent.

Another aspect to consider is the assets and liabilities of the family. If the family assets are more than the liabilities, including home loan, car loan, or other loans, as well as future liabilities such as children's education and marriage expenses, then their net worth is positive. In such cases, where the family income is more than their monthly expenses (excluding Rahul's income) and the net worth is positive (including current and future liabilities), life insurance may not be necessary as the family is financially independent.

However, if the family members are dependent on Rahul's main income and if the net worth is negative, i.e., the current and future liabilities are more than the asset values, then life insurance becomes essential.

Introduction:

When it comes to life insurance, many individuals find themselves confused and overwhelmed by the various options available in the market. Questions such as whether to purchase life insurance or not, which type of insurance is suitable, when to buy it, and how to select the best policy often arise. In this article, we will address these important questions and provide you with a clear understanding of life insurance, empowering you to make informed decisions.

Outline:

I. Introduction II. Who Should Buy Life Insurance? A. Assessing Financial Situation B. Dependency and Net Worth Analysis III. Which Life Insurance Policy to Choose? A. Term Insurance B. Endowment Policy C. ULIP (Unit Linked Insurance Plan) IV. Understanding the Benefits of Term Insurance A. Pure Insurance Coverage B. Premium Comparison C. Returns on Investment V. Exploring Endowment Policies and ULIPs A. Money Back Guarantee and Returns B. Life Insurance Coverage Analysis VI. The Superiority of Term Insurance with Mutual Funds A. Enhanced Sum Assured B. Higher Returns on Investment VII. Factors to Consider When Choosing a Life Insurance Policy A. Coverage Amount B. Premium Affordability C. Policy Duration D. Claim Settlement Ratio VIII. When to Purchase Life Insurance? A. Early Career Stage B. Life Milestones (Marriage, Parenthood, etc.) C. Before Other Investments IX. Key Parameters for Selecting the Best Life Insurance A. Reputation and Financial Stability of the Insurer B. Policy Features and Riders C. Flexibility and Customization Options D. Premium Payment Options E. Policy Exclusions and Limitations X. Conclusion XI. Frequently Asked Questions (FAQs)

1. What happens if I stop paying premiums for my life insurance policy?

2. Can I change my life insurance policy after purchasing it?

3. Are there any tax benefits associated with life insurance?

4. Can I have multiple life insurance policies?

5. How often should I review my life insurance coverage? XII. Get Access

Choosing the Best Life Insurance: A Comprehensive Guide

Introduction:

Friends, when we think of taking life insurance, it creates a lot of confusion. So many different questions start popping. A very important question is whether we should take life insurance or not. Is life insurance suitable for my profile or not? Many people don't even think about this. The second question is, which insurance is best if we decide to take it? Term Insurance, Endowment policy, or ULIP? When should we take life insurance? How can we choose the best life insurance and what are all the parameters to check? Should we pay a single, regular premium or for a limited time? And when all the points are clear, we think that whether we should discontinue our existing policy or not?

I'm going to answer all these important questions in this article so that whenever you go to buy life insurance, your life becomes easy. The process of selecting the right policy can be overwhelming, but with the right knowledge and understanding, you can make an informed decision. Let's dive in and address the most important question first.

Who Should Buy Life Insurance?

To determine if life insurance is necessary for you, it's essential to assess your financial situation. Two key factors play a significant role in this evaluation: your income and your family's financial dependency.

Firstly, consider your income and your family's income. If your income is the primary source of financial support for your family, life insurance becomes crucial. It ensures that in the unfortunate event of your demise, your loved ones are financially protected and can maintain their standard of living.

Secondly, analyze the financial dependency of your family members. If you have dependents such as a spouse, children, or aging parents who rely on your income for their daily needs, education, or healthcare expenses, life insurance provides a safety net to support them in your absence.

Additionally, it's essential to evaluate your net worth. If you have significant debts, such as a mortgage or loans, life insurance can help cover those liabilities and prevent them from burdening your family.

Considering these factors, if you find that your loved ones would face financial hardship in the event of your untimely demise, it's advisable to purchase a life insurance policy.

Which Life Insurance Policy to Choose?

Once you've determined the need for life insurance, the next step is to choose the right policy. There are various types of life insurance policies available in the market, but the most common ones are term insurance, endowment policies, and ULIPs (Unit Linked Insurance Plans).

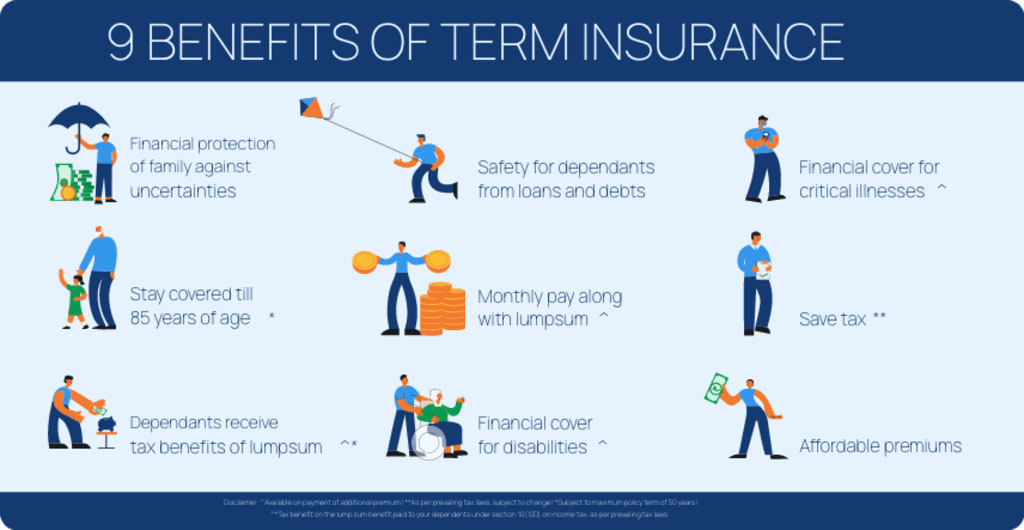

1. Term Insurance: Term insurance provides coverage for a specified term, typically ranging from 10 to 30 years. It offers pure insurance coverage, meaning it pays out the sum assured only in the event of the policyholder's death during the policy term. Term insurance policies generally have lower premiums compared to other types of life insurance.

2. Endowment Policy: An endowment policy combines insurance coverage with savings. It provides a death benefit to the nominee in case of the policyholder's demise during the policy term, and if the policyholder survives the term, a maturity benefit is paid out. Endowment policies have higher premiums compared to term insurance but offer a guaranteed payout.

3. ULIP (Unit Linked Insurance Plan): ULIPs are investment-cum-insurance products. They offer life insurance coverage along with an investment component, allowing policyholders to invest in various market-linked funds. ULIPs provide flexibility in investment options but may involve higher charges and risks.

Understanding the Benefits of Term Insurance:

Term insurance is often considered the most suitable option for individuals seeking pure insurance coverage. Let's explore some key advantages of term insurance:

1. Pure Insurance Coverage: Term insurance focuses solely on providing a death benefit to the nominee in the event of the policyholder's demise. It ensures that the financial needs of your dependents are met if you're no longer there to provide for them.

2. Premium Comparison: Term insurance policies generally have lower premiums compared to other types of life insurance. This affordability allows individuals to purchase higher coverage amounts within their budget.

3. Returns on Investment: Term insurance policies do not provide any maturity or investment returns. However, it allows policyholders to invest the savings from lower premiums into other investment avenues, such as mutual funds, which can potentially yield higher returns over the long term.

Exploring Endowment Policies and ULIPs:

While term insurance focuses on pure coverage, endowment policies and ULIPs offer additional benefits. Let's explore some features of these policies:

1. Money Back Guarantee and Returns: Endowment policies offer a money-back guarantee, meaning the policyholder receives periodic payouts during the policy term. If the policyholder survives the term, a maturity benefit is paid out. ULIPs also provide investment returns based on the performance of the chosen funds.

2. Life Insurance Coverage Analysis: Compared to term insurance, endowment policies and ULIPs may provide lower coverage for the same premium amount. It's important to evaluate the life insurance component of these policies and determine if it adequately meets the needs of your dependents.

The Superiority of Term Insurance with Mutual Funds:

To maximize both insurance coverage and investment returns, a popular approach is to combine term insurance with mutual funds. This strategy allows you to benefit from the advantages of both products. Here's how it works:

1. Purchase a Term Insurance Policy: Start by selecting a suitable term insurance policy based on your financial needs and affordability. Consider factors such as the coverage amount, policy term, and premium payment term.

2. Invest the Savings: Since term insurance policies generally have lower premiums compared to other types of life insurance, you can allocate the saved amount towards investments. Mutual funds are a popular choice due to their potential for higher returns over the long term.

3. Choose Mutual Funds Wisely: Research and select mutual funds that align with your investment goals, risk tolerance, and investment horizon. Consider factors such as the fund's historical performance, fund manager's expertise, expense ratio, and investment strategy.

4. Diversify Your Portfolio: It's advisable to diversify your investments across multiple mutual funds to spread out the risk. Allocate your investments based on your risk appetite, financial goals, and investment horizon.

5. Monitor and Review: Regularly monitor the performance of your mutual funds and review your investment portfolio. Make adjustments as needed based on market conditions, changes in your financial situation, and investment objectives.

By combining term insurance with mutual funds, you can secure your family's financial future with the insurance coverage while potentially earning higher returns through your investment portfolio. This approach offers flexibility, affordability, and the potential for wealth creation.

Consulting a Financial Advisor:

It's crucial to consult a qualified financial advisor before making any decisions regarding life insurance and investments. A financial advisor can help assess your financial situation, understand your goals, and provide personalized recommendations based on your needs and risk profile.

They can help you determine the appropriate coverage amount for your term insurance policy and assist in selecting suitable mutual funds for investment. A financial advisor can also guide you through the application process, policy documentation, and provide ongoing support for your investment portfolio.

Remember to review your insurance coverage and investment strategy periodically to ensure they align with your changing financial goals and circumstances.

Conclusion:

Life insurance is an essential tool for financial planning and ensuring the well-being of your loved ones. By carefully assessing your family's financial dependency, net worth, and considering the need for financial protection, you can make an informed decision about purchasing life insurance.

Term insurance is often recommended for individuals seeking pure insurance coverage at an affordable cost. By combining it with mutual funds, you can potentially enhance your investment returns while maintaining adequate insurance coverage.

Remember to seek professional guidance from a financial advisor to navigate through the various options, understand the terms and conditions, and make well-informed decisions that align with your financial goals.

About the Creator

Ranjan Kumar Pradhan

Unleash your curiosity and dive into a realm of captivating wonders. Join me on a journey of knowledge, inspiration, and thought-provoking insights. Let's embark on an extraordinary adventure together.

Keep reading

More stories from Ranjan Kumar Pradhan and writers in Families and other communities.

Thrilling Showdown in Qualifier 1: CSK vs GT Clash Sets the Stage for IPL 2023 Drama

Introduction The IPL 2023 playoffs are underway, and the CSK vs GT qualifier 1 match took place at the M.A. Chidambaram Stadium in Chennai. The match drew attention as an emoji of a tree was shown instead of a dot ball during the game, sparking controversy. This article delves into the events of the match, the significance of dot balls, and the impact of players like Shami. Furthermore, it explores the relationship between dot ball cricket and environmental conservation.

By Ranjan Kumar Pradhan3 years ago in Gamers

Wise~Guys

— Look Behind what's in Front of You ~ Make Good Choices — Hey, So how you Doin'..! Made~Men — Mobster Movies romanticise a distinctive, elegant appearance, impeccable attire style, along with the 'Families' expressive lingo. Making their 'Bones' gave them Panache — with vintage fedoras, tailored pin-striped suits, mirror-polished wing-tip shoes adorned with tassels; with their 'Gun Moll' gorgeous dates on their arms.

By Jay Kantor18 days ago in Families

Comments

There are no comments for this story

Be the first to respond and start the conversation.