Simple vs. Compound Interest: How to Make Them Work for You

See how simple and compound interest impact loans, investments, and savings. Discover their differences, real world examples, and practical tips to make good financial decisions and to achieve your goals.

When it comes to managing money, one of the most essential concepts to understand is the difference between simple interest and compound interest. Whether you’re borrowing money to pay for a home, financing a car, or investing for the future, these two types of interest play a pivotal role in determining how much you’ll pay—or how much your money will grow over time.

In this guide, we’ll break down these two types of interest, highlight their differences, and provide fresh, real-world examples to help you apply this knowledge to your financial decisions.

Simple Interest: The Straightforward Option

What is Simple Interest?

Simple interest is calculated solely on the original principal amount, meaning the interest doesn’t grow over time. It’s predictable and easy to calculate, making it a common choice for short-term loans or situations where steady, manageable payments are preferred.

The Formula for Simple Interest

The formula for simple interest is:

Simple Interest (SI) = Principal (P) × Rate (R) × Time (T) ÷ 100

Example: A Short-Term Personal Loan

Imagine you borrow $8,000 at an annual interest rate of 6% for 3 years.

Annual interest = $8,000 × 6 ÷ 100 = $480

Total interest after 3 years = $480 × 3 = $1,440

Total repayment = $8,000 (principal) + $1,440 (interest) = $9,440

In this case, the interest remains constant at $480 each year, making it easy to budget for your repayments. Simple interest is a great option if you want predictable, steady payments.

Compound Interest: The Power of Growth Over Time

What is Compound Interest?

Compound interest takes things a step further by calculating interest not only on the principal but also on any previously earned or accrued interest. This “interest on interest” effect means that the total amount grows exponentially over time.

The Formula for Compound Interest

Compound Interest (CI) = P × (1 + R/n)^(n × t) – P

Where:

P = Principal

R = Annual interest rate (as a decimal)

n = Number of times interest is compounded per year

t = Number of years

Example: A Long-Term Investment

Let’s say you invest $5,000 in a retirement account with an annual interest rate of 7%, compounded quarterly, for 10 years.

CI = $5,000 × (1 + 0.07/4)^(4 × 10) – $5,000

CI = $5,000 × (1.0175)^40 – $5,000

CI = $5,000 × 1.34935 – $5,000

CI = $6,746.75

In this example, your investment would earn $6,746.75 in interest, more than doubling the initial $5,000. Compound interest works best when you’re investing over a long period, as it allows time for the exponential growth effect to take hold.

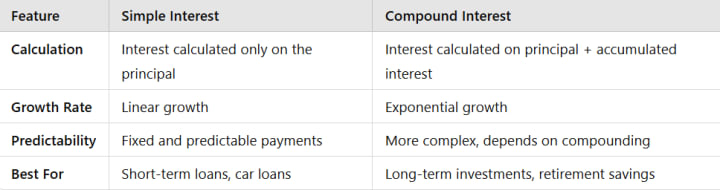

Key Differences Between Simple and Compound Interest

To better understand the difference between these two types of interest, here’s a quick comparison:

When to Choose Simple or Compound Interest

When Simple Interest is Better

Short-Term Loans: Simple interest is ideal for short-term loans like personal loans or car loans, where you repay the loan within a few years.

Predictable Payments: If you prefer a straightforward repayment plan where you know exactly how much interest you’ll pay, simple interest is the way to go.

When Compound Interest is Better

Investments: If you’re saving for long-term goals like retirement, compound interest helps your money grow significantly over time.

Time is on Your Side: Compound interest works best when you have years—or even decades—for your investment to grow.

Comparing Car Loans

Let’s compare two different $20,000 car loans, one with simple interest and the other with compound interest:

Simple Interest Loan

Loan Amount: $20,000

Annual Interest Rate: 5%

Term: 5 years

Calculation:

Annual interest = $20,000 × 5 ÷ 100 = $1,000

Total interest = $1,000 × 5 = $5,000

Total repayment = $20,000 + $5,000 = $25,000

Compound Interest Loan (Compounded Annually)

Loan Amount: $20,000

Annual Interest Rate: 5%

Term: 5 years

Calculation:

CI = $20,000 × (1 + 0.05)^5 – $20,000

CI = $20,000 × 1.27628 – $20,000

CI = $5,525.60

Total repayment = $20,000 + $5,525.60 = $25,525.60

Which is Better?

In this example, the simple interest loan saves you $525.60 compared to the compound interest loan. This highlights why simple interest is often used for car loans—it keeps costs lower and predictable for the borrower.

Tips for Managing Interest Like a Pro

Know the Type of Interest: Always check whether your loan or investment uses simple or compound interest, and ask about the compounding frequency for compound interest.

Pay Off High-Interest Debt First: If you have debt with compound interest (like credit card debt), prioritize paying it off as soon as possible to avoid skyrocketing interest.

Start Investing Early: If you’re taking advantage of compound interest for investments, start early to maximize growth over time.

Use Calculators: Online tools like loan calculators and compound interest calculators can help you understand exactly how much you’ll pay or earn over time.

Conclusion

Both simple interest and compound interest have their place in financial planning. Simple interest is straightforward and predictable, making it great for short-term loans or those who want stability. Compound interest, on the other hand, offers exponential growth that’s ideal for long-term investments but can also make loans more expensive if you’re not careful.

Understanding how these two types of interest work will empower you to make better financial decisions, whether you’re borrowing money, paying off debt, or investing for the future. By using interest to your advantage, you can take control of your financial journey.

About the Creator

FinanceLove

Just a guy who like to write about Finance.

Keep reading

More stories from FinanceLove and writers in Education and other communities.

DeepSeek-V2: The AI Model That’s Beating ChatGPT-4 Turbo—But Not Without Controversy

The AI race is heating up, and a new contender has emerged: DeepSeek-V2. Developed by the Chinese AI research team DeepSeek, this model has recently made headlines for outperforming OpenAI’s ChatGPT-4 Turbo in multiple benchmarks.

By FinanceLove12 months ago in Education

How exactly do inhaler work?

Early 20th century writer, Marcel Proust, finished his magnum opus “In Search of Lost Time” from bed— in a cork-lined room to keep allergens out. Proust suffered from severe asthma. At the time, there weren’t great treatments. When breathlessness set in, he’d burn powders that filled the space with smoke and fumes. Or, for a quick fix, he’d smoke a doctor-recommended anti-asthma cigarette. These powders and cigarettes commonly contained thorn apple, which can open your airways. However, both were clearly terrible ideas.

By Munesh Yadavabout 9 hours ago in Education

Everyday Cooking Skills That Turn Home Kitchens Into Creative Spaces

Cooking at home is more than a routine task. It is a practical life skill that supports better health, saves money, and encourages creativity. While recipes are helpful, true kitchen confidence comes from understanding essential cooking skills that work across countless dishes. When home cooks grasp these fundamentals, they can adapt recipes, solve problems, and cook with freedom rather than fear.

By Erika Mackinnonabout 8 hours ago in Education

Comments

There are no comments for this story

Be the first to respond and start the conversation.