Foreclosure vs. Short Sale: 7 Key Differences Every Real Estate Pro MUST Know

Navigating Distressed Inventory with Precision and High-Quality Data from REI Data Solutions

You are driving through a target neighborhood and spot a classic "diamond in the rough." The lawn is overgrown, mail is spilling out of the box, and the shutters are hanging by a thread. To the untrained eye, it is just a neglected house. To a seasoned real estate professional, it is a potential high-margin opportunity.

However, before pulling a title report or knocking on the door, you must identify the legal and financial status of the property. Is it a short sale or a foreclosure? While both terms describe homeowners in financial distress, treating them as the same is a tactical error that can cost thousands in lost time and earnest money.

Understanding the mechanics, timelines, and negotiation levers of these two distinct paths is essential for navigating the distressed property market. Here is a breakdown of the seven key differences every real estate professional should master.

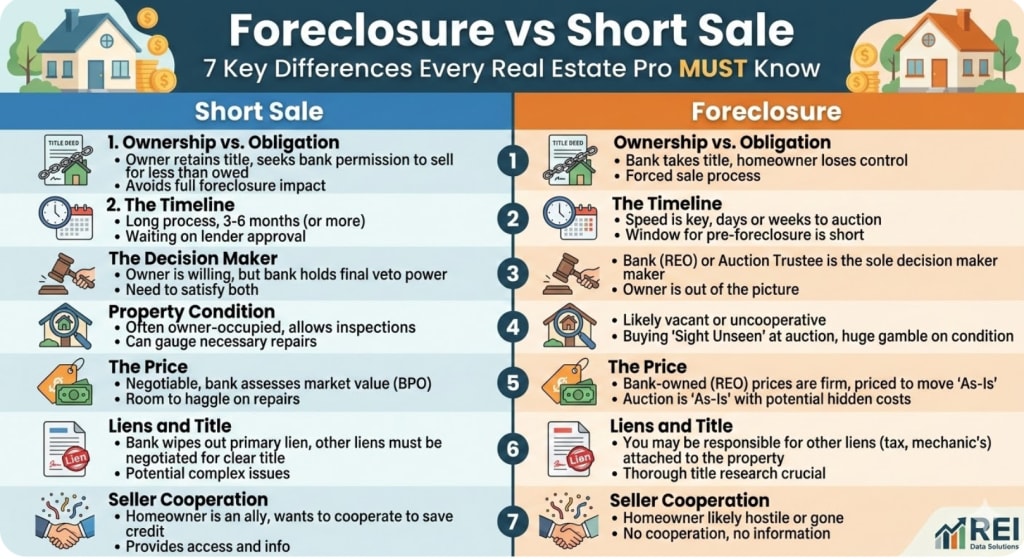

1. Legal Definition: Possession vs. Obligation

The fundamental difference lies in who holds the deed and the owner’s intent.

- Short Sale: The homeowner still owns the property but owes the lender more than the home’s current market value. The "short" refers to the bank accepting a payoff less than the total mortgage balance. The homeowner is typically seeking a graceful exit to mitigate credit damage.

- Foreclosure: This is a legal action where the lender forcibly takes back the property because the borrower defaulted. Once foreclosed, the homeowner loses equity, title, and the right to remain. You are no longer dealing with a person; you are dealing with a corporate REO (Real Estate Owned) department or a court-appointed trustee.

2. The Decision Makers

In a standard transaction, there are two parties: buyer and seller. In distressed real estate, the "decision-maker" table is crowded.

In a short sale, you are in a three-way negotiation. You must convince the homeowner to sell, but more importantly, you must convince the bank to take a loss. The bank will often hire third-party appraisers to verify the value. Even with a signed contract from the owner, the bank can reject the deal if they believe an auction will yield a higher return.

In a foreclosure, the homeowner is legally irrelevant. You deal solely with the lender or a trustee. This simplifies communication but removes the "human element." It is a clinical transaction based strictly on the bank’s internal recovery numbers.

3. The Timeline: Marathon vs. Sprint

If you are looking for a quick turnaround, a short sale is rarely the answer.

- Short Sales: These are notorious "waiting games." Because banks involve multiple layers of bureaucracy, obtaining a final "Short Sale Approval Letter" can take anywhere from 90 days to over six months.

- Foreclosures: During the "Pre-Foreclosure" phase, there is extreme urgency because a sale date is looming. Once the property hits the auction block, the transaction happens in minutes. Post-foreclosure REO properties often move faster than traditional sales as banks are motivated to clear non-performing assets off their books.

4. Property Condition and Inspection Rights

Due diligence is your primary shield, but that shield is often lowered in foreclosure scenarios.

In a short sale, the homeowner is usually still in residence, allowing for traditional inspections. You can assess the HVAC, structure, and plumbing. While the bank sells "as-is," knowing the extent of the repairs allows for an informed offer.

Foreclosures are often a gamble. At a public auction, you are frequently buying sight-unseen. You may be bidding on a house that has been stripped of materials or vandalized. Even with REO listings, the bank has no personal history with the home and will provide zero disclosures regarding defects.

5. Title Complexity and Hidden Liens

A "clear title" cannot be taken for granted in this space.

In a short sale, the primary lender usually coordinates with other lienholders to clear the title. However, if there is a second mortgage or a tax lien, those parties must also agree to a "haircut." If one junior lienholder refuses, the deal collapses.

At a foreclosure auction, you are responsible for your own title research. Depending on state law, you might purchase the property subject to unpaid property taxes, IRS liens, or municipal fines. Buying a foreclosure without a title search is a high-risk move.

6. Occupancy Challenges

When you purchase a short sale, the homeowner typically agrees to a move-out date as part of the closing process. This is generally a cooperative transition.

In a foreclosure, the exit is often uncooperative. You may find the property occupied by a frustrated former owner or a tenant. Your first "renovation" task may not be painting, but rather hiring an attorney to handle a formal eviction, a factor that must be calculated into your initial bid.

7. Strategic Sourcing: Finding the Leads

Knowing the difference between these paths is only useful if you are looking at the right data. Many professionals rely on the MLS, where competition is highest.

To find true off-market opportunities, identify homeowners in the "Pre-Foreclosure" window. This is the sweet spot where you can negotiate a short sale before the property goes to auction. Success here requires moving beyond outdated public records and utilizing high-quality data services that highlight delinquency status and equity positions.

Conclusion

The distressed property market is lucrative for those who understand these nuances. Short sales require the patience of a diplomat and the skills of a negotiator. Foreclosures require the speed of a sprinter and the nerves of an experienced investor. By mastering these seven differences, you position yourself as a professional who doesn't just find houses, you find opportunities.

About the Creator

Keep reading

More stories from REI Data Solutions and writers in Education and other communities.

Mastering Cold Calling Scripts for Pre-Foreclosure Properties

In the 2026 real estate landscape, the most effective investors are distinguished not by the size of their marketing spend, but by their mastery of crisis psychology. While many entry-level practitioners focus on high-volume, low-intent listings, a sophisticated sector of the market is dedicated to the pre-foreclosure niche.

By REI Data Solutions28 days ago in Education

Why the Sun Appears Yellow: The Science Behind the Color of Our Star

The True Color of the Sun Although people often describe the Sun as yellow, scientists classify it as a white star. The Sun emits light across the entire visible spectrum, including red, orange, yellow, green, blue, and violet wavelengths.

By shahkar jalal6 days ago in Education

Atlas Aluminum Corp Parts Catalog: Aerospace Manufacturing, Aviation Hardware, and Industrial Aluminum Components

Introduction: My Research Into Atlas Aluminum Corp Parts Catalog While exploring aerospace hardware suppliers and industrial component manufacturers, I came across the Atlas Aluminum Corp Parts Catalog listed on the NSN platform. What fascinated me most was how manufacturers like Atlas contribute to the broader ecosystem of aerospace engineering, aviation structures, and industrial aluminum components.

By Beckett Dowhan2 days ago in Education

Comments

There are no comments for this story

Be the first to respond and start the conversation.