403(b) vs. 401(k): Cousins in the Retirement Family

A dive into the differences between 403(b)/401(k)

403(b) vs. 401(k)

Whether you work in the private sector or public service, choosing the right retirement plan can significantly impact your financial future. The difference between 401k and 403b plans often confuses many professionals seeking to secure their retirement. While both plans offer tax advantages and help you save for the future, they serve different types of employers and come with distinct features. A 401(k) typically caters to private-sector employees, however, a 403(b) is designed specifically for public schools, non-profits, and religious organizations. Understanding these key differences will help you make an informed decision about which retirement plan best aligns with your career path and financial goals.

Understanding 401(k) and 403(b) Basics

Both 401(k) and 403(b) plans serve as tax-advantaged retirement savings vehicles, offering employees structured ways to build their retirement nest eggs. Understanding their fundamental features and eligibility requirements helps in making informed retirement planning decisions.

Key Features of Each Plan

Both plans share core characteristics that make them valuable retirement savings tools. First, these plans offer tax advantages through pre-tax contributions, reducing participants' taxable income for the year [1]. Additionally, earnings grow tax-deferred until withdrawal, maximizing the potential for long-term wealth accumulation.

The contribution limits remain identical for both plans. For 2025, participants can contribute up to USD 23,500 annually [1]. Furthermore, those aged 50 and above can make catch-up contributions of USD 7,500, while participants aged 60-63 can contribute an additional USD 11,250 [1].

Notably, 403(b) plans offer a unique advantage for long-term employees. Participants with 15 years of service at the same organization can make special catch-up contributions of up to USD 3,000 annually, with a lifetime maximum of USD 15,000 [2].

Start or increase your 403(b) contributions today.

Who Can Participate

The primary distinction between these plans lies in employer eligibility:

401(k) Plans: Available through:

- Private sector companies

- For-profit businesses

- Some nonprofit organizations [3]

403(b) Plans: Exclusively offered by:

- Public schools and universities

- Tax-exempt 501(c)(3) organizations

- Religious institutions

- Public school systems organized by Native American tribal governments

- Cooperative hospital service organizations [1]

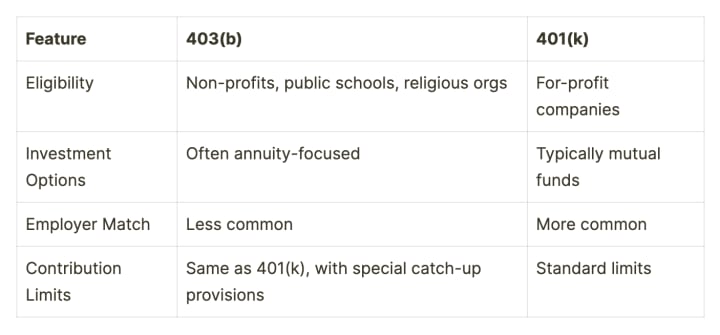

Consequently, 403(b) plans must follow the "universal availability rule," requiring employers to offer plan participation to all employees regardless of their tenure [1]. In contrast, 401(k) plans can implement eligibility requirements, including waiting periods of up to one year and minimum age requirements of 21 [2].

Both plans typically allow for employer matching contributions, though this feature is more common in 401(k) plans [4]. Moreover, vesting schedules for employer contributions generally differ, with 403(b) plans often featuring shorter vesting periods of three years compared to the typical six-year schedule in 401(k) plans [5].

Start or increase your 403(b) contributions today.

Contribution Rules and Limits for 2025

The 2025 tax year brings significant updates to retirement plan contribution limits, offering enhanced savings opportunities for both 401(k) and 403(b) participants.

Standard Contribution Caps

For 2025, the base employee contribution limit increases to USD 23,500 for both 401(k) and 403(b) plans [11]. This represents a USD 500 increase from the 2024 limit [12]. The combined employer-employee contribution ceiling rises to USD 70,000, up from USD 69,000 in the previous year [11]. Accordingly, these adjustments reflect cost-of-living increases determined by the Internal Revenue Service.

Special Catch-up Provisions

First of all, participants aged 50 and older maintain access to the standard catch-up contribution of USD 7,500 [13]. Particularly noteworthy for 2025, individuals aged 60 through 63 qualify for an enhanced catch-up provision of USD 11,250 [11]. This allows eligible participants in this age group to contribute up to USD 34,750 annually [14].

403(b) plans offer an additional unique feature for long-term employees. Those with 15 years of service at qualified organizations can make special catch-up contributions, subject to these limits:

- USD 3,000 per year

- Lifetime maximum of USD 15,000

- Total based on USD 5,000 multiplied by years of service, minus prior elective deferrals [15]

Start or increase your 403(b) contributions today.

Primarily, qualified organizations for this provision include educational institutions, hospitals, health service agencies, and religious organizations [15]. When both age-based and service-based catch-ups apply, contributions exceeding the standard limit must first utilize the 15-year service catch-up before applying the age-based provision [5].

Starting in 2025, part-time employees gain expanded access to retirement benefits. Both 401(k) and 403(b) plans must offer participation to long-term part-time workers who complete at least 500 hours of service in two consecutive years [16]. This modification reduces the previous three-year service requirement, making retirement savings more accessible to part-time workforce members.

Making Your Choice Based on Career Path

Career choices directly determine retirement plan options, with distinct advantages tailored to different employment sectors. First thing to remember, employees rarely get to choose between 401(k) and 403(b) plans, as eligibility stems from their employer's classification [21].

Private Sector Career Considerations

Professionals in the corporate world automatically qualify for 401(k) plans through their for-profit employers [21]. In light of this arrangement, private sector employees benefit from several distinct advantages:

- Investment flexibility through mutual fund companies [3]

- More prevalent employer matching programs [22]

- Broader investment options beyond annuities and mutual funds [23]

- Standardized ERISA protections for all plans [3]

Given these points, private sector employees often find 401(k) plans better suited to their needs, primarily due to the extensive investment choices and consistent regulatory oversight. Above all, these plans typically offer more robust employer matching programs, as private companies face fewer restrictions on contribution matching [22].

Public Service Career Considerations

For this reason, public service professionals, including educators, healthcare workers, and non-profit employees, typically participate in 403(b) plans. These plans offer unique benefits aligned with public service careers:

Qualified employers for 403(b) plans encompass public schools, tax-exempt 501(c)(3) organizations, and religious institutions [1]. Public service employees gain access to distinctive features, such as the ability to receive employer contributions for up to five years after leaving their position, with a maximum of USD 69,000 for 2024 [24].

Public sector 403(b) plans often provide more flexible vesting schedules [3]. Some organizations maintain ERISA exemption status by choosing not to offer matching contributions [3]. Nevertheless, this trade-off allows for reduced administrative costs and potentially lower fees for participants.

Long-term public service employees with 15 or more years at qualified organizations can make additional catch-up contributions of up to USD 3,000 annually, with a lifetime maximum of USD 15,000 [1]. This provision recognizes and rewards extended service in public sector careers.

Public school employees, particularly those in systems organized by Native American tribal governments, receive special consideration under 403(b) regulations [1]. Similarly, ministers employed by religious organizations or functioning as ministers in non-religious settings may qualify for 403(b) participation [1].

The universal availability rule ensures that all eligible public service employees can participate in their organization's 403(b) plan, with limited exceptions for those working less than 20 hours per week or contributing less than USD 200 annually [1]. This inclusive approach aligns with the public service sector's commitment to employee welfare.

Start or increase your 403(b) contributions today.

Conclusion

Both 401(k) and 403(b) retirement plans offer valuable paths toward financial security, though their suitability depends largely on career choices and employer types. Private sector employees benefit from 401(k) plans' broader investment options and prevalent matching programs, while public service workers gain unique advantages through 403(b) plans' special catch-up provisions and flexible vesting schedules.

The 2025 contribution limits remain identical for both plans at USD 23,500, with additional catch-up allowances for older participants. Though 401(k) plans show higher average account balances, 403(b) plans typically feature lower investment costs, offsetting some performance differences.

Career path ultimately determines plan availability, as employees rarely choose between these options. Rather than focusing on which plan type is superior, professionals should maximize the benefits of their available plan through consistent contributions, strategic investment choices, and full utilization of employer matching when offered.

Laura Munoz, Senior Advisor with Financial Advantage Consultants

References

[1] - https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-403b-tax-sheltered-annuity-plans

[2] - https://www.thetaxadviser.com/issues/2021/jan/retirement-plans-comparison-401k-sec-403b.html

[3] - https://www.investopedia.com/ask/answers/100314/what-difference-between-401k-plan-and-403b-plan.asp

[4] - https://www.ncoa.org/article/what-are-the-differences-between-401-k-and-403-b-plans/

[5] - https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-403b-contribution-limits

[6] - https://www.cnb.com/personal-banking/insights/403b-vs-401k.html

[7] - https://www.ebri.org/content/full/401(k)-plan-asset-allocation--account-balances--and-loan-activity-in-2022

[8] - https://www.plansponsor.com/surveys/2024-403b-market-survey/

[9] - https://newsroom.fidelity.com/pressreleases/fidelity--2022-retirement-analysis--in-the-midst-of-inflation-and-uncertainty--retirement-account-ba/s/095bb4a8-cf3a-484e-a911-bc0c61c460ff

[10] - https://www.fool.com/retirement/plans/401k/401k-vs-403b/

[11] - https://tax.thomsonreuters.com/news/irs-announces-2025-retirement-plan-dollar-limits-and-thresholds/

[12] - https://www.cnbc.com/select/401k-contribution-limit-2025/

[13] - https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2025-ira-limit-remains-7000

[14] - https://www.moaa.org/content/publications-and-media/news-articles/2024-news-articles/finance/whats-changing-for-your-retirement-contributions-in-2025-and-beyond/

[15] - https://www.irs.gov/retirement-plans/403b-plans-catch-up-contributions

[16] - https://www.quarles.com/newsroom/publications/key-secure-2-0-act-updates-for-defined-contribution-retirement-plans

[17] - https://www.fidelity.com/learning-center/smart-money/average-401k-match

[18] - https://humaninterest.com/learn/articles/looking-in-depth-at-the-401k-employer-match/

[19] - https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-vesting

[20] - https://extensishr.com/resource/blogs/benefits-of-401k-plans-employers/

[21] - https://www.investmentnews.com/guides/401k-versus-403b-guiding-clients-through-retirement-plan-choices/254206

[22] - https://www.ramseysolutions.com/retirement/403b-vs-401k?srsltid=AfmBOoqRA7CSNz_RCXsQcYkvEruZqW8IPvoUpPiiy5-i7weG3iODuxi1

[23] - https://www.empower.com/the-currency/work/difference-between-401k-and-403b

[24] - https://www.merceradvisors.com/insights/retirement/leaving-your-job-heres-what-to-do-with-your-401k-and-403b-accounts/

About the Creator

Laura E. Munoz

Sr. Advisor at Financial Advantage Consultants, specializing in 403(b)'s, tax advisory, rollovers, IRAs, Roth IRAs, financial planning, Wills, and Trusts. Backed by 50+ years of team expertise, helping clients secure their financial future.

Keep reading

More stories from Laura E. Munoz and writers in Education and other communities.

Are you leaving money on the table?

Are You Leaving Money on the Table? Imagine this: You’re cleaning out a drawer and come across an old 401(k) statement from a job you left years ago. As you look at it, you start to wonder—how much money have you forgotten about?

By Laura E. Munoz12 months ago in Education

How Toys Shape Young Minds and Inspire Lifelong Learning

Toys aid in development by providing children with the opportunity for exploration, stimulus for creativity and development of life skills. While playing with toys from infancy, children develop cognitively and emotionally. Toys have not only been used as objects of play and amusement, but also as a tool for imagination, exploration, and emotional development. The toy industry has had to adapt and grow with new educational models, innovations in design, and interactivity to meet children's modern developmental needs. By today, toys are not only for entertainment, they also carry the potential to shape how children think and interact with the world.

By Rohit Shah3 days ago in Education

🅼🅸🅳🅽🅸🅶🅷🆃 🆂🅽🅰🅲🅺🆂

"It's 10 in Tuscon! We all know what that means... It's Time for Midnight Snacks with your man, Gerald Gee! Ready to spend the night together? Me too! I'm full of snacks and can't wait to regurgitate them all back into your hungry ears. Crack a brew! Pop some corn! Anything to get ready for one hell of a show where the talk maybe cheap but the words cut deep...

By Lamar Wiggins7 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.