We Did 4 Tesla Valuations. They All Show It's Highly Overvalued.

Enough of just trolling Musk, he trolls himself at some point. Here are 4 methods that calculate Tesla’s true stock price. (Originally Posted on March 15, 2025)

Introduction

Setting aside Elon Musk’s character, for quite some time now critics have come out and stated that Tesla’s stock price is extremely overvalued. Others in defense argue that it is a fair price and even stand firm with bullish positions on Tesla, claiming it still to be the most innovative EV car company across the globe.

Who’s right? Who’s wrong?

Numbers can answer this question, as the phrase "Numbers don’t lie" is often true.

Before getting to the numbers, there is something quite unique about Tesla we must consider:

Originally it started as a car company, or at least that is the only sector that is comparable to at the time, the automotive industry. This is our reasoning behind using the traditional PE Valuation Method, comparing Tesla to its automotive competitors.

Over time Tesla has created a shift broadening its horizons into more of a tech-forward company, though it should be noted that its EV roots are vital to the company’s growth. Take the boycotts and sales plummeting as an impact on price

Yes, Tesla does have some tech if that is what people want to call it.

There is no denying that there are critics of Tesla’s products, while it’s also important to reflect on its unreliable track record. We know you’re asking where the numbers are by now.

Let’s dive in on taking these 4 different approaches to explore and see if critics are right or wrong, and if they are right, our goal is to figure out how much is Tesla overvalued.

1. The Traditional P/E Method: Comparing Tesla to Automakers

The least complex, simplest approach.

This method is straight-forward meaning we are comparing Tesla’s Price-to-Earnings, P/E ratio, to other competitors’ in the automotive industry.

The Formula for calculating P/E:

P/E = Stock Price / Earnings Per Share (EPS)

After Trump pumped it up after having his sales pitch on the White House Tesla Lot, its stock price is at $247.

Telsa’s EPS is $2.04 (last reported)

Tesla’s P/E vs. Traditional Automakers

Tesla: ~121

Hyundai: ~4

Ford: ~6

General Motors: ~5

To determine the true price using this traditional approach, we’ll provide two examples:

Tesla compared to Ford, P/E of 8: 2.04 x 8 = ~$16 per share

Tesla compared to Hyundai, P/E of 4: 2.04 x 4 = ~$8 per share

Yes, that is accurate.

You are probably wondering why Tesla’s is way higher compared to other car companies. The reason is due to the prior mentioned discussion; Tesla is evolving beyond a traditional car company thus the growth will not look identical when viewing it side-by-side with its competitors.

This approach being the least complex, is argued to be “weakest”. It’s essentially treating Tesla as if it were only a car company, which we know isn’t entirely true. On the other hand, the point again of Tesla’s origins and ties to the car industry should be duly noted. Ignoring that truth is ignoring a massive piece of Tesla’s derived valuation.

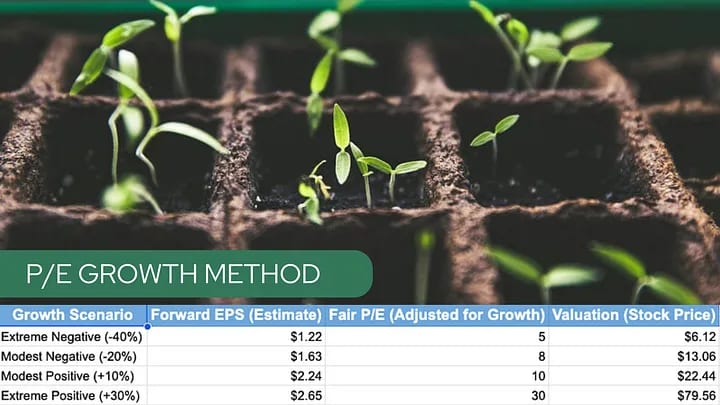

2. The PEG Method: Including Tesla’s Growth

Incorporating Tesla’s growth. The chart says more than enough for itself.

Let’s do a quick run-down of this method and then do an overview of each scenario. This method takes the extra step in that it factors in the point that:

‘Tesla is not a car company’. Yes, we know.

So the PEG method simply says:

‘Let’s factor in Tesla’s growth to the PE method, bro.

Four Scenarios:

Scenario 1: Extreme Negative Growth (-40%) As crazy as it sounds, there is a possibility it could happen. Due to the boycotts, sales declining at levels never before, BYD and other competitors taking their share in the EV market; the trend has been extremely slow growth.

Scenario 2: Modest Negative Growth (-20%) This is simply a less extreme version of scenario 1. Possibly Trump’s administration and foreign money will continue to prop up Tesla’s stock throughout 2025.

Modest Positive Growth (+10%) In the case that Musk dampens the noise and reigns back in some of his controversies, as well as Tesla sees steady growth in sales over each quarter, signifying the idea of a turnaround.

Extreme Positive Growth (+30%) The case we see as most unlikely, but we cannot eliminate it from being the reality. This is the case that the administration goes heavy on supporting Tesla and imposes more restrictions on Americans looking for competitors

Key takeaway:

What this method suggests is that even if Tesla has a year of extreme positive growth (30%), what Reuters estimated at the beginning of the year, its true fair price is still valued at roughly $80.

This points to Tesla still being very overvalued, as it is currently sitting around $240. We can see the other three scenarios and none of them look any better.

Musks’ Image Impacting Growth

Putting aside all of the criticism, Musk has been known to market himself and his companies well. From governments to millions of people across the globe, he has convinced plenty to believe in all of his visions for years.

However, we have mentioned this before; Musk’s investors are selling his debt at a loss. Our take on it is that Musk’s behaviors are catching up to him quicker than he expected.

People are finally starting to wake up — they are seeing Elon for what he truly is — a scam artist, alike Donald Trump.

The main question:

How much of an impact will Musk’s character have on Tesla’s growth?

Check out how one arrogant tweet from Musk obliterated $29 Billion in contracts for SpaceX.

3. Discounted Cash Flow or DCF

Also known as the “Intrinsic” Valuation

Simply put this method estimates the present value of Tesla’s future cash flows. Key things to consider when using this approach:

- Projected revenue & earnings growth

- Capital expenditures (Research & Dev, factory expansions)

- Discounting future cash flows back to today’s value

Using Tesla DCF Assumptions:

Revenue growth: 15–20%

Free Cash Flow (FCF) Margin: 10–12%

Discount Rate (WACC): 10%

Terminal Growth Rate: 3%

Applying these data points, the outcome of Tesla’s stock is estimated:

Bear Case: $70 per share

Base Case: $90 per share

Bull Case: $120 per share

Conclusion:

Unlike the other approaches, DCF takes into factor Tesla’s potential cash flow. Ultimately, we can assume that a fair range for Tesla’s stock price is between $70–$120, still quite significantly lower than where it is today.

4. A Comprehensive Approach to Valuation

Blending all of the best aspects within the 3 Valuation methods.

- DCF (Growth Adjusted for Risk)

- PEG (Adjusting P/E for Reasonable Growth Assumptions)

- Market Competitors (Tech and Automakers)

- Scenario Analysis (Musk’s Reputation and Boycotts

Final Valuation Estimate Side-by-Side

The Hybrid approach gives the stock a fair value range between $60–$100.

The Bottomline:

What is Tesla worth?

Right now, the price of Tesla is based on hypergrowth, previous strong EV demand, and Musk’s prior leadership in driving ‘innovation’. However, the narrative seems like is starting to shift.

Summary in Bullet points:

- If Tesla continues to grow at 30% YoY, it’s fair value range: $80–$100

- If Tesla’s growth slows to 10% range, it’s fair value range: $20–$40

- If Tesla has a contraction, -15%+ it’s fair value: $15

By now, you know, we’ve written quite a bit on Tesla and Musk. This post was not to focus on his figure, however controversial it may be. On the contrary, the focus was to provide an overview of 4 different approaches in determining a fair value price for Tesla’s stock.

What do you think Tesla’s stock is valued at?

I don’t just write — I help brands grow, pivot, and lead. Whether you need words, strategy, or insight, we’ve got packages for that. Check out my services → Trade in Motions

Enjoyed this read? Subscribe to ournewsletter so you never miss our next article.

About the Creator

Keep reading

More stories from Trade in Motions and writers in Earth and other communities.

The Great Bubble of 2025: Why the US Stock Market Is Poised for a Reckoning

Introduction The US stock market is facing what could be the largest bubble in history, a phenomenon that makes the 2008 financial crisis appear modest by comparison. From soaring valuations in the tech sector to record-breaking bubble indicators, the signs of an unsustainable financial system are clear. Combine this with a government struggling to manage debt, inflation, and the federal budget, and the picture becomes even more concerning.

By Trade in Motions9 months ago in Trader

Why Peet’s Coffee Is Closing Multiple Bay Area Shops After the Keurig Dr Pepper Takeover

Coffee shops are more than places where we grab a morning latte. Especially in the Bay Area, Peet’s Coffee has been part of many people’s daily routines, college memories, and work‑meeting rituals. So when customers learned that several Bay Area locations were closing just months after Peet’s was acquired by Keurig Dr Pepper, the reaction wasn’t just curiosity — it was emotional.

By Muhammad Hassan7 days ago in Earth

What Went Right This Week: The Good News That Matters

In a world often dominated by breaking news alerts, crises, and uncertainty, it can be easy to overlook the positive developments quietly shaping our lives. Yet every week brings stories of progress, resilience, and human ingenuity that deserve attention. From breakthroughs in health and science to acts of kindness and environmental wins, good news still happens—and it matters.

By Aarif Lashari5 days ago in Earth

Comments

There are no comments for this story

Be the first to respond and start the conversation.