Mortgage-Backed Securities Refund: Process and Elegibility Criteria

What are MBS Refunds? learn more here

Key Takeaways

• Mortgage-backed securities (MBS) are investment products that group together many mortgages, yielding reliable cash flows to investors with each monthly mortgage payment. The facts about mortgage-backed securities Understanding the way these securities work is important to all potential investors.

• In addition, with each economic downturn the tide of mortgage defaults rises and there are more mortgage-backed securities refund requests. Understanding where the market is headed will allow investors to predict how shifts in the market may impact their investments.

• Investors need to know what the eligibility requirements are and what documentation they need to provide to start the refund claim. Clear documentation and adherence to deadlines will ensure the smoothest possible claims process.

• Key stakeholders, such as mortgage originators and daily mortgage market participants like servicers, and investors have crucial roles within the refund process. Clear communication between all these stakeholders can help speed up claims and get people back on their feet sooner.

• Knowing what’s happening in your region is key. Legal precedents may be relevant to the refund process and eligibility. In particular, investors should take the time to read up on their applicable regulations to understand their requirements.

• Emerging technologies like blockchain and artificial intelligence are already changing the way refunds are processed, making them more transparent and efficient. Adopting these game changing advances will help investors have a much easier time tracking and reconciling their unrepaired refund claims.

A mortgage-backed security refund happens when mortgage investors get paid back. This occurs whenever a mortgage-backed security (MBS) is refinanced or paid off in full before maturity.

These refunds are triggered in different situations, like when a homeowner refinances their mortgage or sells their home. For investors, especially those in sectors with long duration liabilities, understanding the implications of these refunds is key.

It can make or break cash flow and long-term returns. Understanding what drives these factors gives investors real power. As a result, they can take less risk, make better decisions with their portfolios and better manage the complexity of the mortgage market.

What Are Mortgage-Backed Securities?

Mortgage-backed securities (MBS) are investment products made up of the cash flows from thousands of individual mortgage loans pooled together. This arrangement allows investors to purchase shares of a highly diversified pool of mortgages. In this way, they mitigate risk and generate profits for themselves by collecting interest payments.

The cash flows from MBS are very predictable because they come from the monthly mortgage payments that all homeowners make. Therefore, the performance of these underlying mortgages has a direct effect on the returns realized by MBS investors.

Definition and Functionality

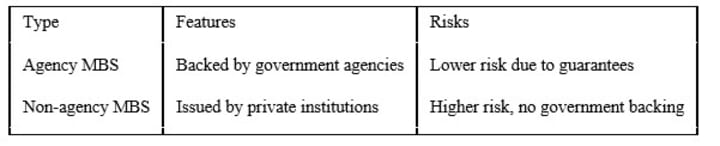

MBS can be issued by government-sponsored enterprises or government agencies, and sometimes by private institutions, the latter often called “private-label” mortgage securities. Creditworthiness plays a major role in determining the level of risk involved.

The quality of a security is based solely on the mortgages that back it. For example, during the 2007-2008 subprime mortgage crisis, a vast majority of MBS lost value as they were tied to bad loans.

Role in the Financial System

These securities have a powerful impact on liquidity in the mortgage market by allowing lenders to recycle capital. This function is more important than ever, including in times of financial crises, as it helps to ensure that housing finance can continue.

In addition, government guarantees from MBS-issuing entities, such as Fannie Mae and Freddie Mac, further insulate the MBS market.

Types of Mortgage-Backed Securities

MBS can be divided into agency MBS, which includes government-backed securities like those from Ginnie Mae, and non-agency MBS, consisting of conventional mortgage loans, thus impacting the agency mortgage market.

Scenarios Leading to Refunds

Mortgage-backed security (MBS) investors, particularly those dealing with agency mortgage securities, might find themselves in several situations that lead to a request for a refund. Recognizing these scenarios is crucial to navigating the complexities of MBS investments.

Common Reasons for Refund Requests

The most common scenario leading to a refund occurs when a loan quality is misrepresented. When the underlying mortgages fail to adhere to defined underwriting criteria, it creates the potential for severe financial harm to bondholders.

Interest rate fluctuations lead to changes in the valuation of MBS. For instance, if rates drop below 5%, homeowners may refinance, creating a ripple effect that can lead to refunds for MBS holders.

Mortgage servicers are the ones who manage these requests, and they have a key role to play in making sure they’re done correctly and fairly.

Impact of Economic Downturns

Economic downturns historically result in increased mortgage defaults, which are directly tied to increased claims for refunds. During recessions, investor confidence in MBS can dry up, as evidenced by crises in the dot-com bubble and 2008 housing crash.

Recent history provides proof that economic downturns take a major toll on MBS performance, resulting in robust refund activity as defaults increase.

Market Fluctuations and Their Effects

Changes in the real estate market may have a significant impact on MBS value and the likelihood of a refund request. High interest rates produce a situation in which investors may start looking for refunds to cover losses.

Moreover, current market conditions, with mortgage rates above 6.5%, indicate low prepayment risk, as many homeowners have locked in lower rates. This scenario significantly lowers the chance of refunds, illustrating the complicated interaction of market conditions and MBS performance.

Eligibility and Process for Refund Claims

We want to make sure that every eligible investor understands the process for MBS refund claims. To receive a refund, Claimants are required to provide proof that they own MBS. These assets need to meet very particular criteria as set out in the bond indenture.

First, you need to be eligible under the 10-year rule. This rule requires the use of principal repayments to retire bonds within narrow timeframes.

Detailed documentation is key in supporting any claim. Detailed documentation, such as transaction logs and reports of compliance, are essential to lend credence to claims for refunds. Investors need to be aware that things like incomplete documentation can lead to massive delays in the refund process.

Key Stakeholders Involved

The refund process is much more complex than simply sending money back to the government. Each party plays a unique role. Originators facilitate the initial mortgage process, servicers manage the loan accounts, and investors seek to recover funds.

Clear and transparent communication between all stakeholders is key. This can help them avoid delays in the claims process and make sure everyone is on the same page.

Steps to Initiate a Refund Claim

To initiate a refund claim, investors should follow these steps:

1. Verify eligibility based on the bond's characteristics.

2. Gather necessary documentation.

3. Submit the claim to the appropriate servicer promptly.

Common documents requested are loan agreements, payment history, and the 10-year rule report.

Common Errors to Avoid

Don’t fall into the trap of submitting incomplete claims and not understanding your eligibility. Double-checking all documentation before submission ensures all information is up to date and accurate.

Second, it helps ensure that the program complies with all applicable rules, including the 10-year and 32-year rules.

Regulatory Frameworks and Guidelines

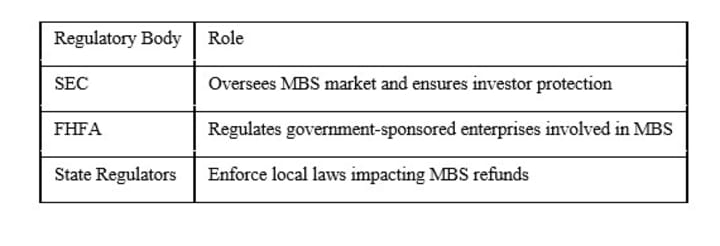

We know that the regulatory environment around MBS and their refund processes is complicated and influenced by federal and state laws. Federal regulations, such as those enforced by the Securities and Exchange Commission (SEC), work to promote transparency. They enforce rules by punishing bad actors and protect investors.

State regulations may be able to further refine refund eligibility criteria, leading to a patchwork of rules around the country.

Regional Regulations Impacting Refunds

Different states have unique regulations affecting MBS refunds. This means, for instance, that the consumer protection laws of California might provide greater rights to investors than would the same laws of a state like Texas.

Yet, these local laws can cause a patchwork of discrepancies in the refund process. So, investors should always be aware of what’s happening at the regional level.

Legal Precedents in Refund Disputes

Legal case precedents play a huge role in MBS refund claims. These important cases have established standards for refund processing. One notable exception to this rule is Lehman Brothers Holdings Inc. V. Greenpoint Mortgage Funding.

Court rulings set the precedent for future disputes to come, but underscore the importance of having a legal advocate that understands this complicated landscape.

How Regulations Shape the Process

Even with these limited exceptions, regulations strongly control the process for filing/processing any refund claims, detailing extensive compliance requirements. An accurate grasp of these regulations goes a long way, as they’re the key to determining how quickly you’ll be able to process refunds.

Maintaining a close watch on the evolving regulatory landscape is imperative to remain compliant and stay ahead of the curve.

Technological Innovations in Refund Processes

The mortgage-backed security (MBS) market is currently experiencing a historic change brought about by new technology, which is enhancing the processing of mortgage repayments and making the refund process faster, easier, and more trustworthy.

Role of Blockchain in Transparency

Blockchain technology is key to creating unprecedented transparency in MBS transactions. By allowing the creation of an immutable ledger of every transaction, stakeholders would be able to track the path of every one of their mortgage-backed securities to guarantee accountability.

Smart contracts take automation and security to the next level, executing the terms of agreement automatically without the need for human involvement. This minimizes the potential for incorrect payments and fraudulent activities.

By tracking the performance of mortgages and the payment of claims, blockchain provides real-time transparency that builds confidence in investors.

Advancements Reshaping Refund Claims

Technological innovations, including machine learning and data analytics, are helping states process refunds more efficiently and effectively than ever. Artificial intelligence increases the accuracy of refund eligibility and claims to avoid disputes as much as possible.

Digital platforms help improve communication between all of the different stakeholders, making it easier to submit and approve refund claims. By enabling greater interconnectedness, these technologies streamline communication for faster resolutions and improve refund process satisfaction.

Future Trends in Mortgage-Backed Security Refunds

Looking forward, changing technologies will further transform the MBS refund arena. Additional regulation and oversight could encourage more stability in the market.

Investor expectations are changing, with increasing calls for more transparency and quicker turnaround times for refunds. With every new technological innovation, the landscape of the MBS sector is ever-shifting toward a more efficient, transparent, and user-friendly system.

Best Practices for Fair Refund Distribution

Distributing mortgage-backed security (MBS) refunds fairly and equitably to both MBS will lead to improved investor confidence. A clear process can go a long way toward making that happen. It begins with knowing what the rules are and applying the refund policy the same way for everyone.

Regularly auditing the refund process is essential. Regular audits are key to quickly flagging discrepancies, especially if proper procedures aren’t being followed. In this vein, transparency and accountability are key—necessary to establish trust among MBS investors.

Recommendations from Experts

Here are some best practices for fair refund distribution that experts say goes a long way. To start, creating a centralized claim processing system would reduce redundancies.

Regular training sessions for all stakeholders involved in the refund process are vital. This keeps everyone informed of current regulations and best practices.

Adaptive feedback loops must be established to develop learnings and improve refund practices through an iterative process that leads to ongoing best practices.

Ensuring Transparency in the Process

Effective and clear communication about refund distribution policies is key. MBS investors deserve convenient access to clear, comprehensive information on how and why refunds are being calculated and distributed.

Regular public reporting of refund distribution outcomes will help build public confidence in the process. It helps potential investors understand whether the process is fair and equitable.

Keeping a record of every step in the refund process is important. It establishes a clear record that can be referred back to if there are future disputes.

Strategies for Stakeholder Engagement

Bringing stakeholders to the table to discuss how best to distribute refunds can provide valuable information. Cooperation between private industry actors can help achieve better outcomes, strengthening the public-private partnership.

Other educational initiatives have proven fruitful, including spreading the word about MBS refunds and empowering investors to better understand and utilize the MBS refund system.

Conclusion

By better understanding mortgage-backed security refunds, you’ll be able to cut through the confusion and mystery of this complex financial world. Knowing how these securities work helps you stay ahead of the game. Further, it educates your agency on what kind of situations would result in a refund. Eligibility and the claims process may feel daunting, but with the right knowledge, you’ll be able to proceed with assurance. Regulatory requirements and technological progress have made the process of refunding much easier. Providing advanced notice and following best practices helps guarantee equity in how any refund gets distributed.

Staying informed allows you to make smart decisions about your investments. If you believe you are eligible for a refund, don’t delay—act now. Compile your paperwork and contact a trusted financial professional to discuss what’s available to you.

About the Creator

Keep reading

More stories from US Mortgage Recovery and writers in 01 and other communities.

Meeting Emission and Dust Standards: Environmental Upgrades and Concrete Batching Plant Cost

Environmental compliance has become a decisive factor in the modern concrete batching plant business. As governments tighten emission limits and dust-control requirements, batching plant operators must look beyond basic production capacity and consider the environmental performance of their facilities. While environmental upgrades inevitably influence concrete batching plant cost, they also play a critical role in long-term business sustainability, regulatory approval, and market competitiveness.

By consrtuctionmachinesabout 24 hours ago in 01

AI Development Cost Explained: What Businesses Really Pay For (and Why)

Artificial intelligence has moved far beyond buzzwords and demos. Today, businesses are using AI to automate operations, personalize customer experiences, predict demand, and make smarter decisions at scale. Yet one question still causes hesitation at the boardroom table: how much does AI actually cost to build?

By alan michael3 days ago in 01

Comments