How to Build a P2P Payment App

Get the essentials on creating a peer-to-peer (P2P) payment app, including the process, different kinds of apps, key features, best practices, and more.

Users want payments that are both seamless—happening instantly and without friction—and fully under their control. Meanwhile, regulators are watching your every move. On top of that, your onboarding experience somehow needs to feel as intuitive and engaging as TikTok. Building a payment app is anything but simple: you’re juggling strict compliance requirements, fierce market competition, handling highly sensitive data, addressing real user frustrations, keeping up with shifting trends, and much more.

Yet it’s far from impossible. You don’t need to be a well-funded startup with venture capital or a dedicated compliance department to succeed. With the right technology stack, a capable team, and a few smart, battle-tested strategies, you can create a payment app that’s lightweight, secure, and genuinely valuable to users.

In this article, I’ll break down the essentials: the key technologies, common pitfalls to avoid, and how to zero in on what users truly care about.

What exactly is a payment app?

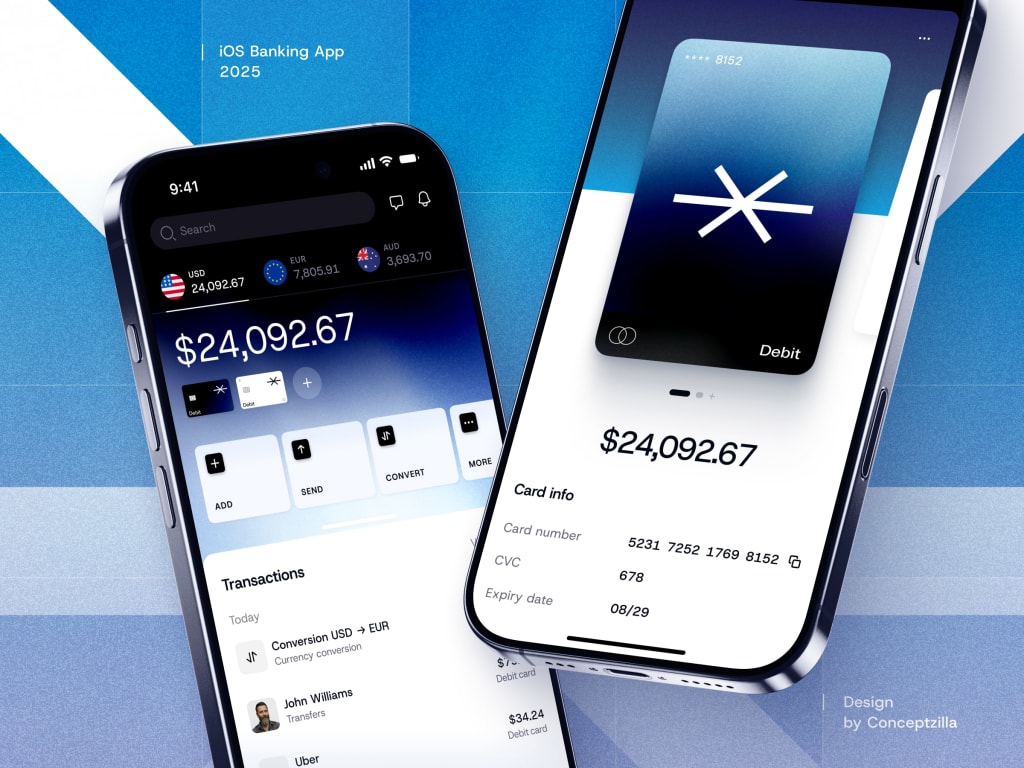

Fundamentally, it’s a digital platform that enables people to send, receive, or manage money without relying on physical cash or paper checks. Think of services like Venmo, Zelle, or WhatsApp Pay—they effectively transform your smartphone into a virtual wallet you never have to pull out of your pocket.

Today’s payment apps often combine multiple features: digital wallets for storing funds or card details, detailed transaction logs, tools for splitting bills, QR-code payments, and even integrated loyalty rewards. Some push the envelope further by adding functionalities like micro-investing, “buy now, pay later” (BNPL) options, or the ability to top up cryptocurrency balances.

And while “fintech” might sound like corporate jargon, it’s simply a shorthand way of describing the intersection of finance and technology. At the center of this space sits the peer-to-peer payment app—a sweet spot where user convenience meets regulatory complexity, where user experience must coexist with ironclad security, and where your product must solve real problems for real people.

How to Build a Payment App: A Practical, Step-by-Step Guide

Step 1: Research & Strategic Clarity

Jumping straight into coding without groundwork is a recipe for failure. Start by defining your purpose with precision:

- Who is your user? Be specific—“freelance designers in Lagos” or “students sharing rent in Lisbon” beats vague claims like “everyone.”

- What gaps exist in current solutions? Maybe competitors are clunky, overcomplicated, or lack local relevance (e.g., Venmo’s social feed feels invasive, or bank apps take 48 hours to settle).

- What’s your edge? Could be hyperlocal partnerships, a radically simpler interface, transparent pricing, or faster settlement times.

Next, map the competitive landscape—not just global giants but regional players too (e.g., Opay in Nigeria, Pix-integrated apps in Brazil, or GrabPay in Indonesia). Most importantly, talk to real users. A single 15-minute conversation with someone who splits bills weekly can reveal more pain points than months of internal speculation.

Step 2: Nail Down Your Business Model & Legal Foundations

This is where vision meets reality and regulation.

Revenue streams to consider in 2025:

- Small transaction fees (on P2P or merchant payments)

- Premium features (e.g., instant transfers for a fee, standard ones free)

- B2B offerings (white-label payment infrastructure for SMBs)

- Earning interest on user balances (only if you hold funds and have the proper license)

Compliance isn’t optional—it’s core to your architecture:

- KYC: Verify user identities upfront

- AML: Implement systems to flag and report suspicious activity

- PCI DSS: Avoid handling raw card data; use tokenization via Stripe, Adyen, or similar

- Local licensing: In the U.S., that means money transmitter licenses; in the EU, an EMI (Electronic Money Institution) license may be required

Consult a fintech-savvy lawyer early—even a one-hour call can save you from months of regulatory missteps. Many assume “P2P = low risk,” but regulators rarely see it that way.

Step 3: Design a Scalable, Secure System Architecture

Think of your app as a set of interconnected services:

- Modular backend: Separate components for authentication, transaction processing, compliance, and reporting

- Event-driven design: Payments are asynchronous—plan for retries, partial failures, and reconciliation workflows

- Cloud infrastructure: Use AWS, Google Cloud, or Azure with auto-scaling to handle traffic spikes

- Resilience patterns: Implement idempotency keys (to prevent duplicate charges), circuit breakers, and dead-letter queues

- Data security: Never store raw card numbers, SSNs, or bank credentials. Use encrypted vaults (e.g., AWS KMS, Basis Theory, or dedicated tokenization services)

Step 4: Craft Intuitive, Trust-Building UX/UI

Money is emotional, so confusion or delay erodes trust instantly.

- Map core user journeys first: How does a new user send money in under 30 seconds? What’s the recovery path if a payment fails?

- Prototype and test early: Build clickable mockups and observe real users. Note where they pause, scroll back, or abandon.

- Prioritize accessibility: Support dynamic text sizing, screen readers, and sufficient color contrast—often a legal requirement, not just a nicety.

Step 5: Develop with Speed, Security, and Flexibility

- Frontend: Use cross-platform frameworks like React Native or Flutter unless you’re targeting only iOS or Android. Keep the interface snappy—payment apps should feel effortless.

- Backend: Choose mature, scalable stacks—Node.js, Go, or Python are solid picks. Start with RESTful APIs, and consider gRPC later for internal microservices.

Key integrations:

- Payment rails: Stripe, Adyen, or local systems (UPI in India, Pix in Brazil)

- KYC/identity: Onfido, Jumio, or regional providers

- Fraud prevention: Sift, Arkose Labs, or similar

Data layer:

- Databases: PostgreSQL (for relational integrity) or MongoDB (for flexible document models)

- Performance: Separate read/write paths; use caching strategically

- Auditability: Log every critical action with immutable, timestamped, and cryptographically signed records

Don’t wait for sandbox access. Mock external APIs early so development isn’t blocked by third-party onboarding delays.

Step 6: Rigorous Testing, Security, and Compliance Validation

This phase is non-negotiable. Test like both a user and an adversary:

- Penetration testing: Hire ethical hackers to probe your system

- Load testing: Simulate 10,000 concurrent transactions—does your system hold up?

- Edge-case scenarios: Negative amounts, timezone bugs, bank callback failures

- Compliance checks: Ensure your KYC flow actually blocks sanctioned individuals

- Accessibility & localization: Run automated checks if launching in multiple regions

Document everything. Your future self, investors, and auditors will thank you.

Step 7: Controlled Launch & Real-Time Monitoring

Go live but cautiously: use feature flags to roll out to 1% of users first. Prepare for App Store/Play Store scrutiny—Apple especially scrutinizes financial apps. Have your privacy policy, terms of service, and compliance documentation ready upfront.

Set up real-time alerts for failed transactions, latency spikes, and fraud indicators.

Tools like Datadog, Sentry, or open-source alternatives (e.g., Prometheus + Grafana) are essential. And always have a disaster recovery plan—your users’ money depends on it.

Step 8: Iterate Based on Real-World Feedback

Post-launch is just the beginning.

- Track core metrics: payment success rate, crash frequency, support ticket volume

- Monitor user sentiment via app store reviews and direct feedback

- Measure what truly matters: active senders, repeat usage, and Net Promoter Score (NPS)

- Continuously improve: Release small, frequent updates based on insights

- Stay compliant: Schedule quarterly reviews of AML policies, data practices, and licensing requirements

Building a payment app is complex, but with focus, the right team, and disciplined execution, it’s entirely achievable, even without a Silicon Valley war chest.

Applying Best Practices in Payment App Development

Building a successful payment app isn’t just about moving money—it’s about doing so securely, reliably, and with the user’s experience at the core. The foundation lies in adopting a security-first philosophy from day one.

This means integrating protective measures directly into the architecture rather than tacking them on later. Sensitive data—whether in transit or stored—should always be protected with end-to-end encryption. Rather than handling raw card or bank account details, rely on tokenization through trusted payment processors like Stripe or Adyen, who manage the most sensitive aspects of the transaction flow. Embrace a zero-trust model: treat every request as potentially malicious until verified.

Beyond that, enhance security with intelligent, proactive layers—such as real-time fraud scoring and automatic session termination when suspicious behavior is detected. And remember, meeting regulatory requirements like PSD2, GDPR, CCPA, and local anti-money laundering laws isn’t optional; it’s essential to establishing trust and legitimacy.

Scalability should be baked into your design from the outset. Even if you're launching for a small user base in a single market, architect your system as if you're preparing for millions across multiple regions. Monolithic systems rarely survive sudden growth without costly rewrites.

Instead, favor a modular, API-driven structure where distinct components—authentication, wallet management, transaction processing, compliance, and notifications—operate as independent but interconnected services. Leverage event-driven communication (using tools like Kafka or RabbitMQ) to allow each piece to evolve without disrupting the whole.

Host your infrastructure on cloud platforms like AWS or Google Cloud that can scale automatically, especially during peak usage times like holidays or flash sales. Keep integrations flexible: whether you’re changing KYC vendors or adding a new payout method, your code shouldn’t require a major overhaul. Early use of adapter patterns and clear interface abstractions makes this possible.

And while comprehensive logging is crucial, ensure logs are structured so you can trace a single transaction seamlessly across all services—something you’ll deeply appreciate when troubleshooting issues.

User experience in payment apps succeeds when it fades into the background. People aren’t looking to “engage” with a financial tool—they just want to send money quickly and move on. That means minimizing steps, reducing mental effort, and anticipating user needs before they arise. Offer clear, easy ways to cancel or correct a payment before it’s finalized, and make support accessible at critical moments.

Flexibility in design is equally important: your interface must accommodate diverse users—those who read right-to-left, rely on screen readers, have limited vision, or deal with spotty internet connections. Support dynamic layouts, scalable text, strong color contrast, and offline functionality so the app remains usable under less-than-ideal conditions.

Artificial intelligence, when applied thoughtfully, can significantly enhance both security and usability. In 2025, machine learning shines in areas like adaptive fraud detection—moving beyond rigid rules to assess real-time risk and flag anomalies without blocking legitimate users.

It can also offer predictive insights, such as alerting a user they’re likely to run out of wallet balance by midweek and offering an auto-top-up. Personalized prompts—like suggesting a recurring payment to a frequent contact—add convenience without being intrusive. However, automation should never override human judgment when money is at stake. Always allow users to challenge or bypass AI-driven decisions, and regularly audit your models to prevent bias that might unintentionally exclude certain demographics.

Finally, view your initial launch as just the starting point. A payment app must evolve continuously to stay relevant and reliable. Establish a steady, sustainable cadence for improvements: review crash reports, support inquiries, and transaction failures weekly; roll out small interface or performance enhancements monthly; and introduce one substantial new feature each quarter based on actual user behavior.

Use feature flags to safely test changes with a small segment of users before broad deployment, and always measure real impact—did that new group-splitting tool actually drive more transactions, or just add visual noise? And don’t let technical debt pile up unchecked. Schedule dedicated time for code refactoring just as you would for building new features. In the world of fintech, maintenance isn’t overhead—it’s what keeps your app secure, fast, and trusted.

Conclusion

Digital wallet development places you at the intersection of genuine, everyday utility and surging global demand. People now depend on digital money as a routine part of their lives—whether splitting dinner costs, paying gig workers, or sending money across borders. If you can address one of these real-world frustrations with a clean, intuitive solution, you’re not just building a feature—you’re creating something users will stick with, scale with, and truly value.

Why Building Payment Apps Matters More Than Ever in 2025

The shift to digital payments is no longer on the horizon—it’s already here. We’ve moved well beyond adoption thresholds; digital transactions are the standard, not the exception.

In 2024, more than 75% of consumers around the world used mobile payments, according to Statista. Instant payment infrastructures like Pix in Brazil, UPI in India, and FedNow in the U.S. are now operational in over 70 countries, enabling near-instant, low-fee transfers. Meanwhile, users are growing less tolerant of platforms that lack smooth peer-to-peer or integrated payment capabilities.

If your product involves any form of value exchange—whether goods, services, or digital content—omitting a native payment experience is increasingly seen as a weakness. For entrepreneurs and builders, this isn’t just a market gap; it’s a powerful opportunity paired with a clear duty to deliver secure, seamless, and user-centered financial functionality.

About the Creator

Shakuro

We are a web and mobile design and development agency. Making websites and apps, creating brand identities, and launching startups.

Power BI Dashboard Development Guide

Introduction: What Is Power BI Dashboard Development? Power BI dashboard development services help businesses transform raw data into visually engaging and interactive dashboards that support informed decision-making. A Power BI dashboard offers a consolidated view of key performance indicators (KPIs) and metrics, often across multiple datasets, enabling users to monitor trends, spot issues, and derive insights at a glance.

By Wahid Hussain7 days ago in 01

It's 2026. Songs Turning 10 This Year

In 2016, we saw the rise of short form videos and what would lead to the birth of TikTok. We cannot forget the Snapchat filters no matter how cringe worthy some of them might have been. It was also the year in which the hit series Stranger Things debuted.

By Jasmine Aguilar7 days ago in Beat

Comments

There are no comments for this story

Be the first to respond and start the conversation.