Global Caustic Soda Market: Navigating Lithium-Ion Battery Demand and Industrial Growth

Examining the role of sodium hydroxide in electrode coating and battery material processing as supply constraints tighten growth dynamics in the 2034 chemical market.

In the world of industrial chemicals, Caustic Soda (Sodium Hydroxide) is often referred to as the "alkali of choice." It is a fundamental building block that keeps the global supply chain moving—from the aluminum in our vehicles to the soaps in our homes. As we navigate through 2026, the market is experiencing a significant shift. While traditional demand from paper and textiles remains a cornerstone, a new wave of growth is emerging from the energy transition, particularly as aluminum becomes the metal of choice for lightweight electric vehicles (EVs).

Market Growth Drivers: The surge in global caustic soda consumption is primarily anchored in the rapid expansion of the alumina and textile industries. In the aluminum sector, caustic soda is indispensable for refining bauxite; with the electric vehicle revolution demanding lighter chassis, aluminum demand has hit record highs. Similarly, the textile industry relies on caustic soda for mercerization, a process that strengthens cotton fibers and enhances dye affinity. As emerging economies in Asia and Latin America ramp up garment exports, factories are requiring larger, more consistent volumes of high-purity lye. Furthermore, municipal investments in wastewater treatment—driven by stricter environmental standards—are creating a massive secondary demand for pH regulation across global infrastructure projects.

Get a Sample Report for Actionable Market Insights

Market Trends: Sustainability is no longer a buzzword in the chlor-alkali sector; it is the primary technological trend. We are seeing an industry-wide migration toward Membrane Cell Technology, which is significantly more energy-efficient and eliminates toxic mercury emissions. A standout trend is the rise of "Green Caustic Soda," where producers utilize 100% renewable electricity for the electrolysis process, offering a product with a drastically lower carbon footprint. Additionally, the shift toward localized, modular production units is helping companies bypass global logistics bottlenecks, ensuring that supply remains resilient even during volatile shipping periods. This localization is proving vital for just-in-time manufacturing in the pharmaceutical and detergent sectors, where inventory reliability is paramount.

Recent News and Developments in the Caustic Soda Market: The landscape has been marked by major capacity expansions and strategic policy shifts. In February 2026, AGC Vinythai successfully launched its expanded chlor-alkali facility in Thailand, boosting its caustic soda capacity to approximately 220,000 tons annually to meet soaring Southeast Asian demand. Meanwhile, in India, the government’s allocation of over US$ 18 billion to the Ministry of Chemicals and Fertilizers in the 2025-26 budget is catalyzing domestic infrastructure, including major new petrochemical regions like the PCPIR in Paradip.

On the corporate front, market leaders are focusing on "value over volume." Olin Corporation recently ended a force majeure following hurricane-related disruptions, signaling a return to steady supply for the North American market. Additionally, the Indian government’s implementation of stricter Quality Control Orders (QCOs) through the Bureau of Indian Standards (BIS) is helping stabilize the market by ensuring that only high-purity, technically compliant chemicals enter the supply chain.

Market Data Summary (Extracted from IMARC Group)

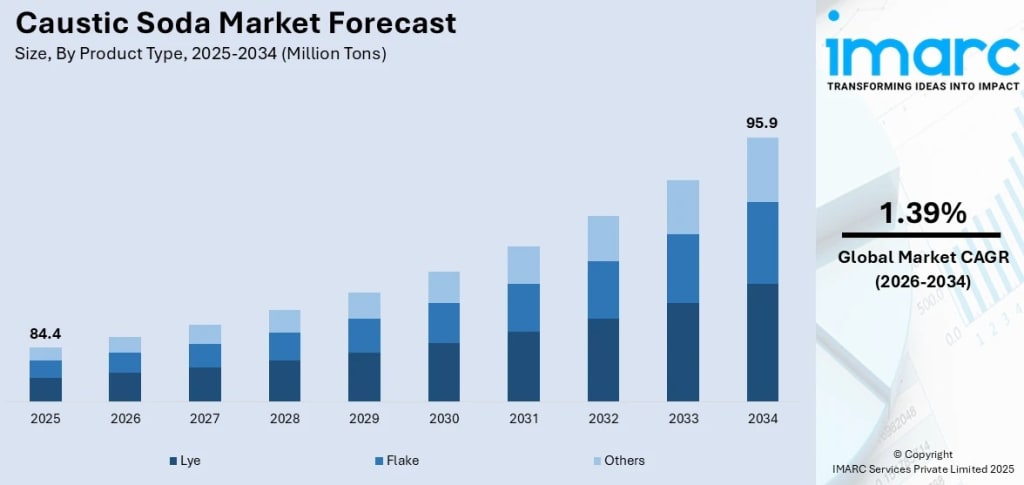

Key Market Statistics: According to the latest IMARC Group data, the global caustic soda market reached a significant volume of 84.4 Million Tons in 2025. Projections indicate a steady climb to 95.9 Million Tons by 2034. This analysis covers the historical period of 2020-2025 and provides an outlook for the 2026-2034 window.

Market Segmentation:

By Product Type: Lye (Liquid Caustic Soda) continues to hold the largest market share due to its ease of handling in large-scale industrial processes, followed by Flakes and Pellets.

By Manufacturing Process: The Membrane Cell process is the dominant and fastest-growing technology, followed by the Diaphragm Cell and the nearly phased-out Mercury Cell.

By Grade: Segments are categorized into Industrial Grade (the bulk of the market), Reagent Grade, and Pharmaceutical Grade.

By Application: Major applications include Organic Chemicals (the largest segment), Alumina Refining, Pulp & Paper, Textiles, Soaps & Detergents, and Water Treatment.

By Region: Asia Pacific leads with over 50% of the global market share, while North America and Europe remain key hubs for high-purity and specialty grades.

Top Industry Players: The market is driven by global giants including Olin Corporation, Tata Chemicals Limited, Dow Chemical Company, Occidental Petroleum Corporation (OxyChem), Shin-Etsu Chemical Co., Ltd., and Formosa Plastics Corporation.

Industry Outlook: Navigating the 2034 Horizon

As we look toward 2034, the caustic soda market is evolving from a pure commodity play into a specialized chemical sector. While the "Big Three" applications—Alumina, Pulp/Paper, and Textiles—will continue to consume the lion's share of volume, the growth of high-purity grades for the pharmaceutical and food sectors represents a high-margin frontier.

The industry is currently balancing a period of capacity expansion with a need for operational efficiency. For stakeholders, the message is clear: the future belongs to those who can produce efficiently, meet the new "Green" standards, and navigate the digital traceability required by modern global regulations.

About the Creator

Rahul Pal

Market research professional with expertise in analyzing trends, consumer behavior, and market dynamics. Skilled in delivering actionable insights to support strategic decision-making and drive business growth across diverse industries.

Audit Evidence vs Audit Documentation: Key Differences Explained

Audit evidence and audit documentation are closely connected concepts in auditing, but they serve different purposes in the audit process. Understanding their distinction is essential for auditors, Accounting students, and finance professionals who want to ensure compliance with international auditing standards and produce reliable audit reports.

By charliesamuel3 days ago in 01

Comments

There are no comments for this story

Be the first to respond and start the conversation.