How to Reduce Your Insurance Premium Without Sacrificing Coverage

Learn how to lower your insurance premium without compromising on coverage. Explore discounts, adjustments, better driving habits, and more to save money.

Car insurance premiums can feel like a hefty monthly expense, but there are ways to reduce them without cutting essential coverage. The goal is to find a balance between paying less and ensuring you’re still fully protected in case of an accident or other unfortunate event. Here are several strategies that can help you lower your insurance premium without sacrificing coverage.

1. Look for Discounts

One of the quickest ways to reduce your premium is to take advantage of discounts offered by your insurer. Best Car Insurance companies often provide several types of discounts, and some might apply to you without much effort. Here are some common discounts to explore:

Safe Driver Discount: If you maintain a clean driving record with no accidents or traffic violations, you could qualify for a safe driver discount. This discount is often available to drivers who haven’t had any claims for a certain period, making you a less risky customer for the insurer.

Multi-Policy Discount: Bundling your car insurance with other policies like home, renters, or life insurance can save you money. Many insurers offer a multi-policy discount, which means you’ll pay less for each policy by combining them. This is a simple way to reduce costs without changing your coverage.

Low Mileage Discount: If you don’t drive much, some insurers offer discounts based on your annual mileage. You might qualify for this discount if your daily commute is short or you primarily use your car on weekends or for errands.

Safety Features Discount: Vehicles equipped with safety features such as anti-theft devices, airbags, automatic braking, or advanced driver assistance systems (ADAS) may qualify for a discount. Modern vehicles with higher safety ratings are less likely to be involved in accidents, which can reduce the insurer’s risk.

By ensuring you’re aware of all the available discounts, you can make sure you’re not paying more than you need to.

2. Make Adjustments to Your Coverage

While it’s important to maintain sufficient coverage to protect yourself financially, you might be able to adjust your coverage limits to reduce your premium. Here are a few ways to tailor your policy:

Increase Your Deductible: A higher deductible means you’ll pay more out of pocket in the event of a claim, but it also lowers your premium. If you can afford to pay a higher deductible in case of an accident, this can be a great way to reduce your monthly costs.

Remove Extras: Review any add-ons or extra coverage you may not need. For example, if you have roadside assistance or rental car coverage but rarely use them, removing these extras can reduce your premium. Be sure to evaluate whether these services are truly necessary based on your driving habits and lifestyle.

Modify Coverage Limits: Depending on your vehicle's age and value, you might consider adjusting your coverage limits. For instance, if your car is older and has significantly depreciated, you may not need comprehensive coverage. Adjusting your policy to reflect your car’s current value could save you money.

When adjusting coverage, it’s essential to ensure that you still have enough protection for your needs. Don’t compromise on critical aspects of your policy, such as liability coverage, as it helps protect you in case of an accident where you are at fault.

3. Improve Your Driving Habits

Your driving habits directly affect your insurance premium. By making a few simple changes, you can lower your risk profile and potentially reduce your rates. Here are some tips:

Drive Less: If possible, try to lower your mileage. The more you drive, the higher the likelihood of being involved in an accident, which increases your risk and, consequently, your premium. If you can, opt for public transport, carpool, or work from home. Even reducing your weekly mileage can make a difference in your premium.

Take a Defensive Driving Course: Many insurers offer discounts for completing a defensive driving course. These courses teach safe driving techniques that can reduce your risk of accidents. Not only does it help improve your driving skills, but it may also make you eligible for a discount on your car insurance.

Avoid Distractions: Distracted driving, such as texting while driving or using a phone, increases the risk of accidents. Keeping your focus on the road can reduce your risk of causing an accident and help you maintain a good driving record, which can result in lower insurance premiums.

By adopting safer driving habits, you demonstrate to your insurer that you’re a responsible driver, which may lead to a reduction in your premium.

4. Review and Compare Policies Regularly

Car insurance rates can change from year to year, so it’s a good idea to regularly review and compare policies to ensure you’re still getting the best deal. Here’s how to do it:

Shop Around: Insurance companies often adjust their rates based on various factors, such as your driving history, location, and the vehicle you drive. To find the best rates, it’s a good idea to shop around and get quotes from different insurers. Even if you’re happy with your current insurer, you might find a better rate elsewhere.

Ask for Policy Adjustments: If you’ve been with the same insurer for a while, it’s worth asking them to review your policy and see if they can offer you a better rate or more suitable coverage. Loyalty discounts or changes in your risk profile (such as moving to a safer neighborhood) might lead to lower rates.

Check for Rate Increases: Sometimes, insurers raise premiums without a clear reason. By reviewing your policy and staying on top of rate changes, you can spot any unnecessary increases. If you see a jump in your premium, contact your insurer to discuss the change or consider switching to another provider.

By regularly reviewing your policy and comparing quotes, you ensure you’re getting the best value for the coverage you need.

5. Maintain a Good Credit Score

Did you know that your credit score can influence your car insurance premium? Insurers often use credit scores as one of the factors to determine your rate, as individuals with higher credit scores are statistically less likely to file claims. To lower your premium, it’s important to maintain a good credit score by:

- Paying bills on time

- Reducing outstanding debts

- Monitoring your credit regularly to ensure there are no errors

Improving your credit score can not only help you get better rates on your car insurance, but it can also benefit your overall financial health.

Final Thoughts

Reducing your insurance premium doesn’t have to mean sacrificing coverage. By taking advantage of discounts, making smart adjustments to your policy, improving your driving habits, and regularly comparing rates, you can lower your costs without compromising your protection. Remember, the key is finding the right balance—adequate coverage at an affordable price. Take action today to save on your car insurance while ensuring you're still well-covered.

About the Creator

Yankit Gayakvad

With 4 years of experience in digital marketing, I specialize in SEO, SMO, SEM, and content strategy. I use data-driven techniques to enhance online visibility, boost engagement, and drive measurable growth for brands.

Keep reading

More stories from Yankit Gayakvad and writers in Wheel and other communities.

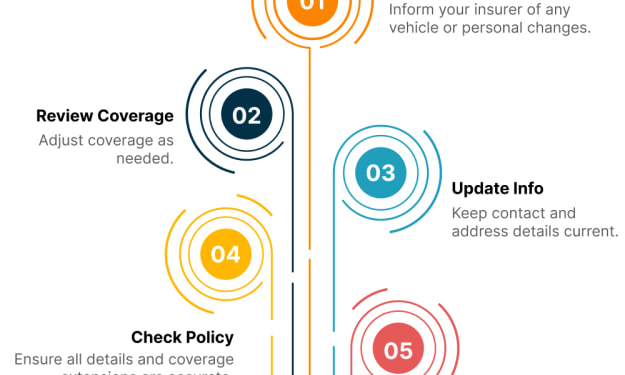

How to Update Your Car Insurance Policy: A Simple Guide

Updating Your Car Insurance Policy Your car insurance policy is more than just a one-time purchase—it’s an ongoing contract that requires updates to reflect changes in your life, vehicle, or coverage needs. Whether you’ve recently moved, purchased a new car, or just want to make sure your policy fits your current needs, it’s important to keep your policy up to date. Here’s a simple guide on how to update your car insurance policy effectively.

By Yankit Gayakvadabout a year ago in Wheel

Road Trips and the Reality of Animal Collisions

Road trips — what can be a better way to enjoy a holiday? Get together with your family or friends, pack all your things in your SUV or a van, load up some music you like, and set off for a big adventure. Driving through highways, watching the scenery change with little towns and mountains flying by.

By Michal Grayenabout 14 hours ago in Wheel

Comments

There are no comments for this story

Be the first to respond and start the conversation.