Was the Closely Watched Core PCE deflator a Bad Number?

Rising Prices

Yes, it was a disappointing outcome!

Moreover, things are likely to get worse for several more months. The Federal Reserves' monetary strategy should eventually extinguish the rampant flames of inflation. Moreover, the current sentiment in Washington towards controlling its future spending means that fiscal policy will also support the move toward dampened inflation pressures over the next couple of years.

Still, the core PCE (i.e., the personal consumption expenditure deflator excluding food and energy), rose by 4.7% on a year-over-year basis versus market expectations of a 4.5% rise in November 2021. It was déjà vu all over again, given that the previously reported Consumer Price Index (CPI) revealed an even firmer 4.9% comparable rise in the core CPI during the same month.

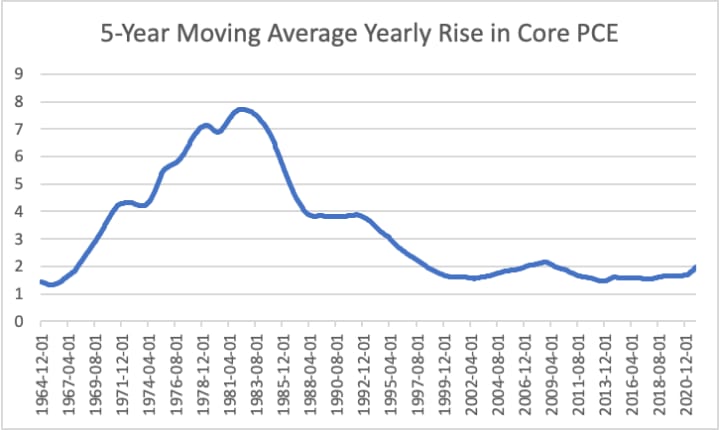

However, economy watchers seem to forget that in August 2020, Fed Chair Powell announced that the Fed would be switching to flexible average inflation targeting. This strategy hinted that if inflation moved below its 2.0% target, it would allow inflation to move above its target in future years to make up for prior undershoots. Taking a closer look at the average rise in the core PCE over the last decade reveals massive undershoots in this inflation metric.

However, the Fed Chair failed to tell us whether the window for such targeting was one, two, or three years in duration so that we could all judge the success or failure of this strategy. In October 2021, St. Louis Federal Reserve President James Bullard stated in an interview (with Christopher Jeffrey (October 2021) on Central Bank.com) that he favored using a five-year moving average window.

That means that we could compute the average yearly rise in the Core PCE (which is the Fed’s preferred inflation metric) over the past five years. Although inflation, as measured by various metrics, has surged well beyond the Fed's 2.0% target, the latest five-year window yielded an average yearly rise of 1.97%. If we take Bullard at his word, the Fed has met its inflation target.

Although the Fed will soon exceed its 2.0% target over a five-year window, there is little reason to doubt (as short-term rates rise and real economic growth slows) that we will eventually move back towards lower inflation rates. Besides, while things look bleak today, a quick review of our historical chart reveals that we are nowhere near the overshoots we experienced during the early 1980s following the 1973 and 1979 oil price shocks.

So When Will our Inflation Outlook Improve?

While rental housing prices and energy prices are likely to remain stubbornly high, the effects of federal spending, an accelerated tapering schedule, and an earlier than expected rise in the federal funds rate will eventually dampen inflation pressures. Investors should pay particular attention to the current negotiations in Washington, DC to see how many aggressive spending programs are limited to one or two years in duration.

We make no judgment as to which programs are worthwhile. That is for voters and legislators to decide. All we wish to do is advocate that spending programs are selected to ensure that aggregate demand does not continue to exceed aggregate supply so that inflation pressures can ease over time.

If Federal Reserve officials follow through on what they have said so far, no one should be surprised if inflation pressures peak sometime around the middle of 2022. Rising short-term rates and slower economic growth have always been a recipe for lower inflation. The only issue is whether the Federal Reserve will raise short-term rates fast and high enough.

Only time will determine whether the Fed has the resolve to accomplish this mission!

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

Fleeting Leaves

Autumn leaves drift down, Beauty fades as time rushes Life, too, feels so brief.

By Anthony ChanExclusive • 6 months ago

Philippines LED Market 2026: Energy-Efficient Lighting Growth, Infrastructure Expansion & Sustainability Trends

Philippines LED Market Overview The Philippines LED market is expanding steadily as energy-efficient lighting solutions gain traction across residential, commercial, institutional and industrial applications. Light Emitting Diode (LED) technology offers significant advantages over conventional lighting — including lower energy consumption, longer lifespan, reduced maintenance costs and environmental sustainability — making it a preferred choice in new construction, retrofit projects and infrastructure upgrades. Market growth is supported by rapid urbanisation, increasing environmental awareness among consumers and businesses, and ongoing innovations that enhance LED performance and versatility.

By Manisha Dixit2 days ago in Trader

Flower Bloom 369

FLOWER Bloom 2/25/26 Wednesday By Mariann Carroll Karen had been with Tony for 7 years. Tony started acting strangely after her surgery. He would mow the lawn in the rain and be on his cellphone. He started pushing Karen away. Tony came clean about seeing someone. Karen moved out two months later. Karen moved in with a friend. She felt betrayed.

By Mariann Carroll7 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.