United States Pain Management Therapeutics Market Size and Forecast 2025

How Aging, Chronic Pain, and Innovation Are Reshaping America’s Pain Care Landscape Through 2033

United States Pain Management Therapeutics Market Overview

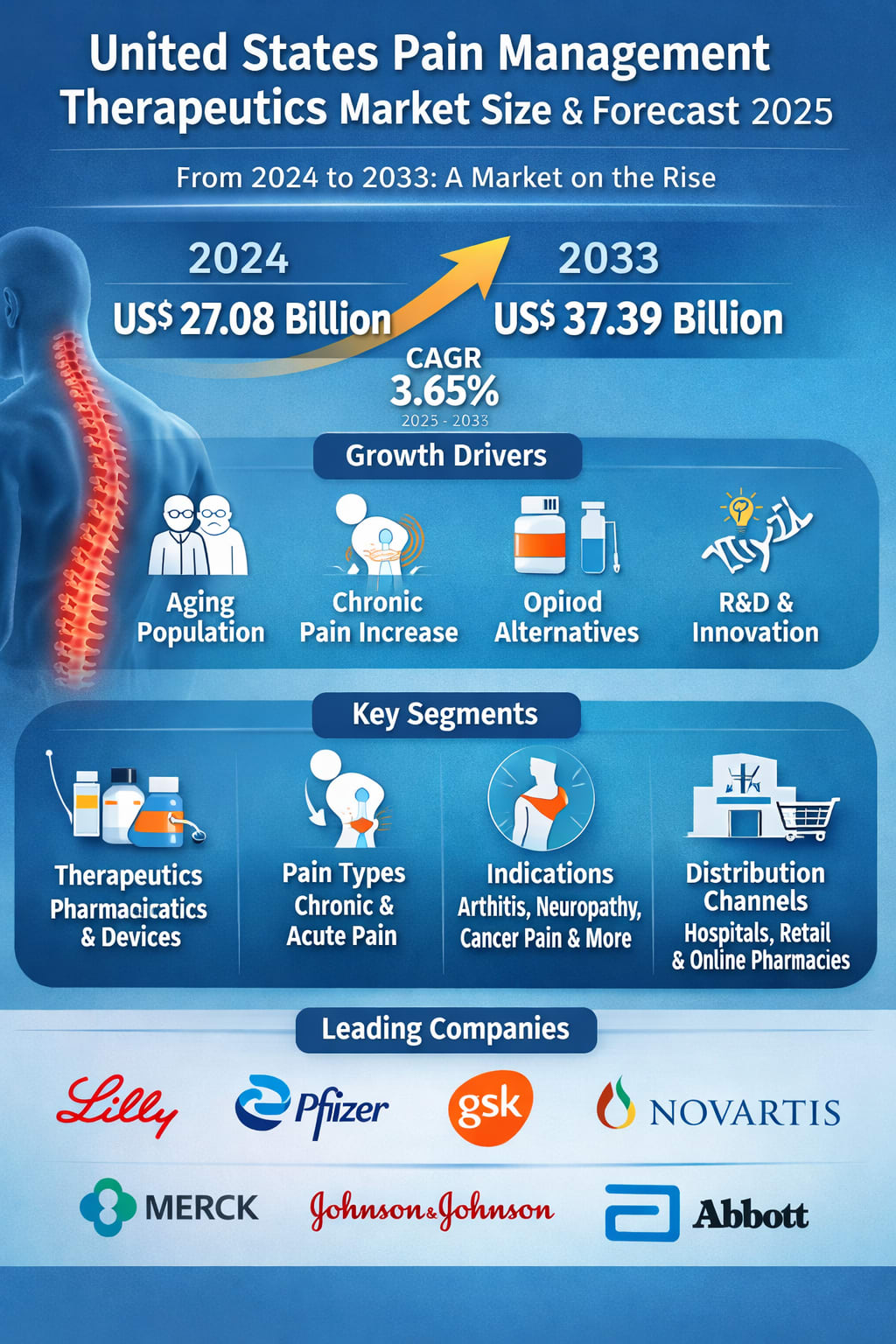

The United States Pain Management Therapeutics Market is entering a crucial phase of transformation, driven by demographic shifts, rising chronic disease burden, and rapid innovation in both pharmaceuticals and medical devices. According to Renub Research, the market is expected to grow from US$ 27.08 billion in 2024 to US$ 37.39 billion by 2033, registering a compound annual growth rate (CAGR) of 3.65% from 2025 to 2033.

Pain management therapeutics refers to a broad range of treatments aimed at reducing or eliminating pain across acute and chronic conditions. These therapies include medications such as analgesics, non-steroidal anti-inflammatory drugs (NSAIDs), opioids, antidepressants, anticonvulsants, and anesthetics, as well as medical devices like electrical stimulators, radiofrequency ablation systems, analgesic infusion pumps, and neurostimulation devices. In addition, non-pharmacological approaches—such as physical therapy, cognitive behavioral therapy (CBT), acupuncture, and nerve blocks—are increasingly integrated into comprehensive pain care strategies.

In modern clinical practice, multimodal pain management has become the gold standard. This approach combines multiple therapies to improve effectiveness while reducing reliance on any single method, particularly opioids. The choice of treatment depends on the cause of pain, severity, duration, and the patient’s overall health profile, making personalized care an increasingly important theme in this market.

Several powerful forces are shaping the U.S. pain management therapeutics landscape. These include the rapidly aging population, the rising prevalence of chronic pain conditions, the urgent demand for opioid alternatives, and continuous advancements in non-invasive and minimally invasive treatments. At the same time, regulatory support for innovative therapies and growing public awareness about pain management options are expanding access and driving adoption across healthcare settings.

Market Size and Forecast: A Steady, Resilient Growth Story

The U.S. remains one of the largest and most sophisticated healthcare markets in the world, and pain management is a critical component of this ecosystem. With millions of Americans living with chronic pain conditions such as arthritis, neuropathy, cancer pain, and chronic back pain, demand for effective and safer therapies continues to rise.

Renub Research estimates that the market will grow from US$ 27.08 billion in 2024 to US$ 37.39 billion by 2033, reflecting a CAGR of 3.65% over the forecast period. While this growth rate may appear moderate compared to some high-growth biotech segments, it represents a stable and sustainable expansion in a mature but essential healthcare category.

This steady growth is supported by several long-term trends:

The aging U.S. population, which has a higher incidence of chronic pain and degenerative conditions

Rising awareness and diagnosis of pain-related disorders

Technological innovation in both drug development and medical devices

A policy-driven shift away from opioid-centric pain management toward safer, multimodal approaches

Together, these factors are ensuring that pain management therapeutics remains a strategic priority for healthcare providers, pharmaceutical companies, and medical device manufacturers alike.

Key Growth Drivers in the United States Pain Management Therapeutics Market

Growing Geriatric Population

One of the most powerful drivers of the U.S. pain management therapeutics market is the rapidly aging population. Every day, more than 10,000 Americans turn 65, and over the next decade, the number of people aged 80 and above is expected to rise by nearly 50%, from 13.9 million to 20.8 million. This growth far outpaces the overall U.S. population increase.

Older adults are significantly more likely to suffer from chronic pain conditions such as arthritis, osteoporosis, neuropathy, and degenerative spine disorders. These conditions often require long-term, carefully managed pain treatment, increasing demand for both pharmaceutical therapies and medical devices.

In addition, seniors are more vulnerable to falls, fractures, and surgical procedures, all of which require effective post-operative and rehabilitative pain management. This demographic shift has also accelerated the development of specialized therapies designed for older patients, including treatments with fewer side effects, lower addiction risk, and minimally invasive delivery methods.

As healthcare systems place greater emphasis on improving quality of life for aging populations, pain management is becoming a central pillar of geriatric care—further fueling market growth.

Rising Prevalence of Chronic Pain Conditions

The increasing burden of chronic pain in the United States is another major growth catalyst. Chronic pain is commonly associated with conditions such as diabetes, arthritis, back pain, neuropathy, cardiovascular diseases, and musculoskeletal disorders—many of which are becoming more prevalent due to aging, lifestyle factors, and longer life expectancy.

According to updates from the Centers for Disease Control and Prevention (CDC), 38.4 million Americans were living with diabetes as of October 2022, and a significant proportion of these patients develop diabetic neuropathy, a painful and often debilitating complication. Furthermore, CDC data from November 2023 indicates that more than one in three Americans are at elevated risk of developing diabetes, suggesting that the future burden of pain-related complications will continue to rise.

Beyond diabetes, the growing incidence of obesity, sedentary lifestyles, and occupational stress is contributing to higher rates of chronic back pain, joint disorders, and musculoskeletal injuries. As the number of patients living with long-term pain increases, so does the demand for effective, targeted, and sustainable pain management solutions—directly supporting market expansion over the forecast period.

Ongoing Research and Development (R&D)

Continuous research and development is playing a crucial role in reshaping the U.S. pain management therapeutics market. Pharmaceutical companies, biotech firms, and academic research institutions are investing heavily in safer, more effective, and more personalized treatments.

Key areas of innovation include:

Non-opioid pain medications aimed at reducing addiction risk

Advanced neuromodulation technologies for chronic and neuropathic pain

Regenerative medicine approaches, such as stem cell therapies and biologics

Personalized medicine, using genetic and biomarker data to tailor treatments

Improved drug delivery systems, including transdermal patches and targeted injections

The growing focus on precision medicine is particularly significant, as it promises to improve treatment outcomes while minimizing side effects. At the same time, increased federal funding and private investment in pain research are accelerating the development pipeline.

As more innovative therapies receive regulatory approval, they are expected to expand treatment options, improve patient outcomes, and drive long-term market growth.

Increased Awareness About Pain Management Options

Public and professional awareness of pain management choices has increased substantially over the past decade. Patients today are more informed about the risks of long-term opioid use and are actively seeking safer alternatives such as physical therapy, acupuncture, mindfulness-based therapies, and non-opioid medications.

Healthcare providers are also placing greater emphasis on patient education and shared decision-making, discussing a wider range of treatment options and encouraging multimodal pain management strategies. This shift is supported by:

Public health campaigns promoting opioid alternatives

Growing acceptance of non-pharmacological therapies

Expanded insurance coverage for certain alternative treatments

Increased focus on holistic and individualized care plans

As awareness continues to grow, more patients are entering the healthcare system earlier and exploring comprehensive pain management solutions, which in turn is boosting demand across both pharmaceutical and device segments.

Challenges Facing the U.S. Pain Management Therapeutics Market

High Costs

Despite strong demand, high treatment costs remain a significant barrier. Advanced therapies—such as novel biologics, regenerative treatments, and specialized medical devices—can be expensive, and insurance coverage is not always comprehensive. For many patients, out-of-pocket expenses limit access to the most advanced or effective options.

This cost burden is particularly challenging for uninsured or underinsured populations, potentially slowing the adoption of innovative therapies and widening gaps in care.

Regulatory Challenges

The U.S. pain management market is also shaped by strict regulatory oversight, particularly from the Food and Drug Administration (FDA). While these regulations are essential for ensuring safety and efficacy, they can make drug and device development time-consuming and costly.

In addition, evolving regulations around opioid prescribing and heightened scrutiny of pain management practices have added complexity for healthcare providers and manufacturers. These regulatory pressures can delay market entry for new treatments and, in some cases, discourage innovation—posing a challenge to long-term growth.

Market Segmentation: A Diverse and Evolving Landscape

The United States Pain Management Therapeutics Market is segmented as follows:

By Therapeutics

Pharmaceuticals

Devices

Electrical Stimulators

Radiofrequency Ablation

Analgesic Infusion Pumps

Neurostimulation

By Drug Class

Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

Anesthetics

Anticonvulsants

Anti-Migraine Agents

Antidepressants

Opioids

Non-Narcotic Analgesics

By Indication

Arthritic Pain

Neuropathic Pain

Cancer Pain

Chronic Back Pain

Post-Operative Pain

Migraine

Fibromyalgia

Bone Fracture

Muscle Sprain/Strain

Acute Appendicitis

Others

By Pain Type

Chronic Pain

Acute Pain

By Distribution Channel

Hospital Pharmacies

Retail Pharmacies

Online Pharmacies

Competitive Landscape: Key Players Shaping the Market

Leading companies operating in the U.S. pain management therapeutics market include:

Eli Lilly and Company

Pfizer Inc.

GlaxoSmithKline plc

Novartis International AG

Merck & Co., Inc.

Abbott Laboratories

Johnson & Johnson

Baxter International Inc.

These companies are analyzed across five key dimensions:

Overview

Key Persons

Product Portfolio

Recent Developments

Financial Insights

Competition in this market is driven by innovation, portfolio diversification, strategic partnerships, and ongoing investment in R&D, particularly in non-opioid and device-based therapies.

Final Thoughts

The United States Pain Management Therapeutics Market is on a steady growth path, projected to expand from US$ 27.08 billion in 2024 to US$ 37.39 billion by 2033 at a CAGR of 3.65%. This growth reflects a healthcare system in transition—moving away from opioid-centric models toward safer, more personalized, and more holistic approaches to pain care.

With an aging population, rising chronic disease burden, increasing awareness, and continuous technological innovation, pain management is becoming more sophisticated and more patient-centric than ever before. While challenges such as high costs and regulatory complexity remain, the long-term outlook is clearly positive.

For healthcare providers, investors, and industry players alike, the coming decade will be defined by innovation, integration, and individualized care—making pain management therapeutics one of the most important and dynamic segments of the U.S. healthcare market.

About the Creator

Future Market Outlook: Will 2025 Be the Next Crypto Bull Run?

As we approach 2025, the global financial landscape is once again turning its gaze toward the volatile yet undeniably transformative world of cryptocurrency. After the rollercoaster ride of the 2022–2024 market cycles—marked by regulatory shake-ups, macroeconomic uncertainty, and technological breakthroughs—the crypto community is buzzing with anticipation: Could 2025 be the year of the next major bull run? For investors, traders, and institutions alike, the answer may lie in a combination of technological evolution, macroeconomic shifts, and increasing institutional adoption. And for those ready to position themselves at the forefront of this potential surge, platforms like Exbix Exchange are emerging as essential tools for navigating the future of digital asset trading.

By crypto19925 days ago in Trader

The Lesions of Devotion

Every day I set myself down on the freshly cut lawn and strip myself bare. I take my guitar and finger the frets and pick at the strings, listening for dissonance. My life is dissonance. I twist the tuning pegs until each string sounds bright. Then I kneel, calves pointing behind me, kneecaps facing forward. All exposed to the breeze. I close my eyes and play the melody.

By Paul Stewart4 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.