Timing the Market?

Here’s Why That’s Costing You Wealth

Let’s face it — market volatility is like that unpredictable friend who crashes the party without warning. One moment, you’re sipping your gains, and the next, you’re clutching your portfolio like a life jacket. The financial headlines flash red, experts start debating on primetime, and investors scramble to “do something.”

But here’s the thing: market swings aren’t surprises. They’re cycles. And if you’re an investor — especially one playing the long game — it’s time to stop fearing the waves and start learning how to surf.

The Temptation of Market Timing: A Dangerous Mirage

When markets dip, so does investor confidence. Panic texts your brain. The urge to exit is strong. You tell yourself, “I’ll get back in when things look better.” But here’s the hard truth: timing the market is like catching lightning in a bottle. Nearly impossible, even for seasoned professionals.

Let’s rewind to April 2022. The markets were reeling from a perfect storm of global shocks: a post-COVID correction, inflation creeping up like an unwanted guest, and geopolitical tensions rising due to the Russia-Ukraine conflict. The Nifty fell about 6% in just two weeks.

Investors panicked. Many pulled their money out.

Then, just as quickly, the market bounced back. The Nifty surged by 9% in the following two weeks. Those who had stayed invested saw recovery. Those who exited? They missed the upswing and ended up with losses driven by fear, not fundamentals.

Volatility happens. But panic? That part’s optional

Let this sink in: markets don’t destroy wealth, emotions do. It’s not what the market does; it’s how you respond that makes or breaks your financial outcome.

Think about the last time markets dipped. Did you feel anxious? Did you consider stopping your SIPs or redeeming your mutual funds? You’re not alone. It’s a very human response.

But markets have weathered it all — wars, pandemics, recessions, policy shifts, tech bubbles. And yet, they have historically risen over the long term. Volatility is part of the market’s DNA, not a defect.

While Others Chase Trends, SIPs Chase Time

Systematic Investment Plans (SIPs) are the unsung heroes of modern investing. They thrive in volatility. When markets dip, SIPs buy more units. When markets rise, your accumulated investments grow. Over time, this rupee-cost averaging turns unpredictability into opportunity.

Yet many investors pull the plug on their SIPs at the worst possible time — during market corrections. This is like running out of a store just because there’s a discount. It defeats the very purpose of investing systematically.

By staying invested and continuing your SIPs during market downturns, you’re essentially buying low. When the market rebounds (and history says it always does), you gain more.

Mind the Gap — In Train Stations and in Your Investment Journey

There’s a brilliant analogy often shared in investing circles: When in the train station, we are told to “mind the gap.” It’s a safety warning. But in the world of investing, not minding the emotional gap between market movements and investor reactions is where the real danger lies.

Many investors lose more money by reacting poorly than they would by simply staying put. They sell in panic and re-enter in greed, repeating a vicious cycle that leaves them drained — both financially and emotionally.

Bridging this gap means cultivating emotional intelligence around your investments. It means having a plan and sticking to it, regardless of the noise.

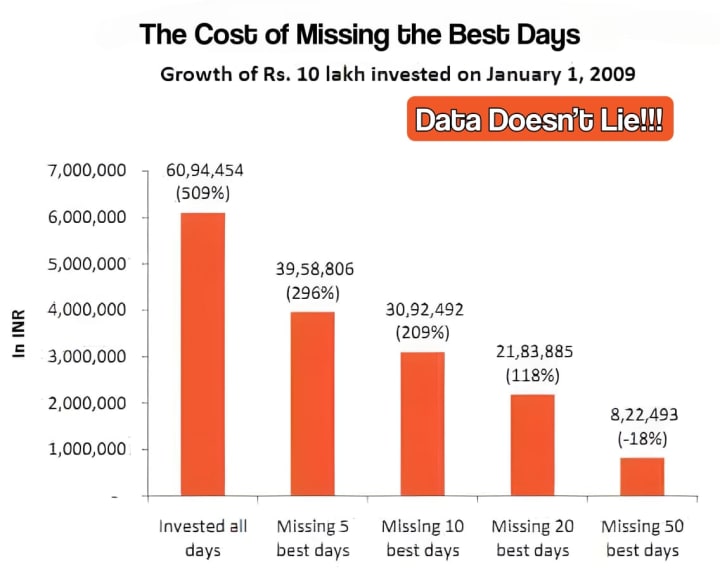

Data Doesn’t Lie: The Cost of Missing the Best Days

Here’s a sobering stat: if you missed just the 10 best days in the market over a decade, your returns would be significantly lower than someone who stayed invested the entire time. And those “best days” often come right after the worst.

For instance, if you had invested in the Nifty 50 from 2012 to 2022 and stayed put, your CAGR (Compound Annual Growth Rate) would be around 11–12%. But if you missed just the 10 best days, your returns could drop to 7–8%, or even lower.

Trying to time your entries and exits not only increases your stress but erodes your returns.

The Long Game Always Wins

Investing isn’t about predicting the next quarter. It’s about planning for the next decade.

Think of your financial goals — a child’s education, retirement, a home, or a vacation. These aren’t short-term desires. They deserve long-term discipline.

By staying invested through market ups and downs, you allow your investments to compound, adjust, recover, and grow. Markets will always have corrections. But corrections aren’t crashes. They’re opportunities.

What Should You Do in Volatile Times?

● Stay invested. The market rewards patience, not panic.

● Continue SIPs. Don’t stop the engine when the road gets bumpy.

● Review, don’t react. If your goals haven’t changed, your plan shouldn’t either.

● Diversify. A well-diversified portfolio absorbs shocks better.

● Consult an expert. Don’t DIY your way into financial heartbreak.

A Final Word: Discipline Beats Drama

In a world where noise is endless — news cycles, stock tickers, tweet storms, and WhatsApp forwards, the rarest asset is not any secret tip, it’s a clear mind, it’s clarity. And discipline? That’s your secret superpower. It doesn’t just help you survive turbulent times — it helps you thrive through them.

Staying calm when others panic isn’t just admirable — it’s a winning strategy.

So, the next time the market takes a dip, when red bleeds across your screen and your heartbeat skips with every breaking headline — pause.

Breathe. Zoom out. Look not at the moment but at the mission.

Because volatility is temporary, regret from emotional decisions can last far longer.

Remember: The market might be unpredictable, but your strategy doesn’t have to be.

Stick to your SIPs. Trust your asset allocation. Let your investments weather the storm while you focus on what matters, living your life, chasing your dreams, and keeping your eyes on the horizon.

Stay invested. Let compounding do what hype never can — build quiet, lasting wealth. You don’t need to predict the next big thing. You need to prepare for the next decade of growth.

So, here’s the real question:

Would you rather gamble with fear — or grow with faith?

Your portfolio is waiting for your answer.

Your future self is too.

About the Creator

SubhShanti Wealth

Since 2011, SubhShanti Wealth has empowered investors by transforming one-sided sales into meaningful conversations that prioritize financial well-being. Beyond mutual fund distribution, we guide you toward lasting financial security.

Keep reading

More stories from SubhShanti Wealth and writers in Trader and other communities.

Robo-Advisors vs Financial Advisors: Who Should Guide Your Money?

It was a breezy Saturday—the kind that makes you feel like time’s finally on your side. Aryan and I had carved out a rare afternoon from our chaotic schedules to reconnect. Amid the aroma of coffee beans and the hum of weekend conversations, we swapped stories, from awkward office gossip to half-baked vacation plans.

By SubhShanti Wealth9 months ago in Trader

Australia Residential Real Estate Market: Housing Demand, Urban Growth & Market Dynamics

Australia Residential Real Estate Market Overview The Australia residential real estate market remains one of the most closely watched segments of the nation’s economy, given its critical role in household wealth, urban development, investment flows and housing supply. Residential real estate — encompassing houses, apartments, townhouses and multi-unit dwellings — reflects broader demographic changes, migration patterns, policy dynamics and consumer preferences. The Australia residential real estate market size was valued at USD 6.40 Trillion in 2025 and is projected to reach USD 7.99 Trillion by 2034, growing at a compound annual growth rate of 2.49% from 2026-2034. This growth illustrates sustained long-term demand, evolving lifestyle preferences and structural shifts that continue to influence housing markets across major cities and regional areas.

By Amyra Singh8 days ago in Trader

Stanislav Kondrashov Explores Gold’s New Identity: Why the 2026 Surge Is More Than Just Market Panic

Gold has always had its moments. But 2026 is shaping up to be something entirely different. With prices smashing records — reaching $4,639.42 per troy ounce — and silver climbing beyond $90, global markets are buzzing. Is this just another run to safety, or is something deeper unfolding?

By Stanislav Kondrashov7 days ago in Trader

Smart phones, Humans and Aliens.

WARNING. I will be tapping into one of your favorite creative tensions: The absurdity of humans worshipping their glowing rectangles as if they were tiny oracles. There’s something deliciously poetic about that contradiction, and it lends itself beautifully to an instructive proviso.

By Novel Allen5 days ago in Poets

Comments

There are no comments for this story

Be the first to respond and start the conversation.