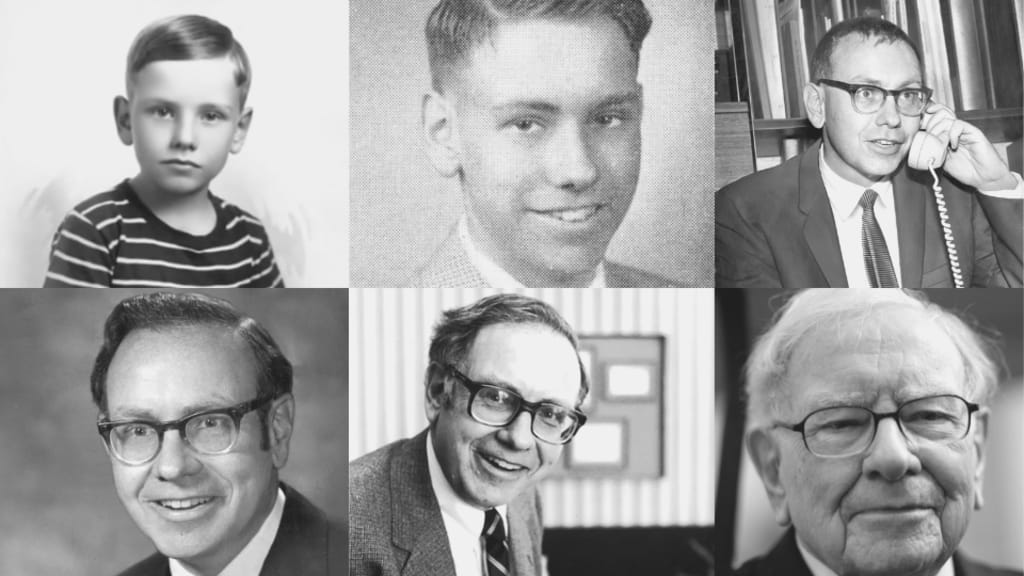

"The Security I Like Best" by Warren E. Buffett

Warren Buffett's Early Investment Philosophy: A Blueprint for Value Investing and Long-Term Success

In his article The Security I Like Best, published in The Commercial and Financial Chronicle on December 6, 1951, Warren Buffett outlines his early investment philosophy and sheds light on his approach to investing that would later propel him to legendary status in the financial world. At the time, Buffett was a young man working at Buffett-Falk & Co. in Omaha, Nebraska, and his ideas were strongly influenced by his mentor, Benjamin Graham, the father of value investing.

Focus on Intrinsic Value

Buffett begins by emphasizing the importance of buying securities at a price below their intrinsic value, which was a central tenet of Graham’s philosophy. He defines intrinsic value as the true worth of a business, determined by its earnings, assets, and long-term potential rather than its market price at any given moment. He explains that the market often misprices securities, which creates opportunities for investors who are diligent in their research and analysis.

This concept of intrinsic value would become a cornerstone of Buffett's investment strategy. By purchasing stocks at prices below their intrinsic value, investors gain a margin of safety, which provides protection against unforeseen risks or market downturns. This principle of protecting against the "permanent loss of capital" would guide much of Buffett’s future decision-making, helping him to avoid speculative investments and focus on sound, long-term opportunities.

The Role of Management

In the article, Buffett also stresses the importance of a company’s management. He acknowledges that even if a company is undervalued, its long-term success is heavily dependent on its leadership. A company with strong, ethical, and competent management is more likely to navigate economic downturns, make wise decisions, and ultimately generate consistent profits.

Buffett emphasizes the need for investors to not only look at financials and valuations but to assess the integrity and capabilities of a company’s leadership team. At the time, Buffett’s emphasis on management was groundbreaking, as many investors at the time focused more on quantitative metrics than on qualitative factors like leadership. This would become a hallmark of his later investments, where he sought out businesses with capable management teams that would continue to grow the companies and protect shareholder value.

The Long-Term Perspective

Buffett argues that the best investments are those that provide long-term value, rather than those driven by short-term speculation. He advocates for a patient, long-term investment horizon, where the focus is on the underlying fundamentals of a business, not the daily fluctuations of the stock market. Buffett’s approach was in stark contrast to the speculative mindset that dominated much of the investment world at the time.

By focusing on long-term growth, Buffett believed that investors could avoid the pitfalls of market timing and short-term volatility. He likened investing to owning a business—if an investor purchases a business with strong fundamentals, the stock will naturally rise over time as the company grows and generates profits. Buffett’s preference for companies with durable competitive advantages would later be cemented as one of the defining features of his investing style.

Undervalued Businesses

Buffett continues by discussing his preference for investing in undervalued businesses. He asserts that the most successful investments are those in companies that are trading below their intrinsic value, yet have strong earning potential over the long run. Buffett’s philosophy was to buy businesses when they were "on sale" in the market, ensuring a margin of safety.

However, he cautions that this strategy requires patience. Market prices do not always reflect the true value of a business in the short term, and an investor must be willing to wait for the market to realize the intrinsic value of the company. This strategy requires discipline and the ability to resist the urge to chase short-term market trends.

Avoiding Speculation and Short-Term Focus

Buffett is very clear in the article about his disdain for speculation. He warns against making investment decisions based on market trends or short-term noise. He argues that speculative investments are often driven by fear and greed, leading investors to buy high and sell low, which results in poor long-term outcomes.

Instead, he advocates for a focus on the long-term health and potential of a business. By doing so, investors are more likely to make rational decisions that are based on sound financial analysis rather than emotional reactions to market movements.

Conclusion

In The Security I Like Best, Warren Buffett lays the foundation for the investment principles that would later make him one of the wealthiest and most successful investors of all time. The article provides valuable insight into his early approach to value investing, emphasizing the importance of intrinsic value, strong management, long-term growth, and avoiding speculative behavior. These core tenets of Buffett’s philosophy have remained consistent throughout his career and continue to serve as a model for investors seeking to achieve sustainable wealth over time.

Even in 1951, Buffett's approach was remarkably forward-thinking, with a focus on value, patience, and a deep understanding of the businesses in which he invested. His insights in this article foreshadow the wisdom that would guide him in transforming Berkshire Hathaway into a global investment powerhouse, and they continue to influence investors around the world today.

About the Creator

O2G

I am a storyteller exploring love, resilience, and self-discovery. Through relatable tales, I aim to inspire reflection, stir emotions, and celebrate the courage and beauty in life’s complexities.

Australia Stearic Acid Market: Industrial Demand, Sustainability Trends & Functional Applications

Australia Stearic Acid Market Overview The Australia stearic acid market is witnessing robust growth driven by rising demand from end-use industries such as personal care, cosmetics, detergents, rubber processing, pharmaceuticals and industrial chemicals. Stearic acid — a saturated fatty acid typically derived from vegetable fats (such as palm oil, coconut oil) or animal fats — serves as a versatile ingredient in lubricants, surfactants, emulsifiers, stabilisers, and texturising agents across a wide range of applications. The Australia stearic acid market size reached 0.19 Million Tons in 2024. Looking forward, IMARC Group expects the market to reach 0.30 Million Tons by 2033, exhibiting a growth rate (CAGR) of 5.20% during 2025-2033. This growth mirrors steady industrial activity, increasing consumer goods production, and a growing emphasis on functional and sustainable raw materials in manufacturing and formulations.

By Amyra Singh2 days ago in Trader

Australia Switchgear Market: Power Reliability, Grid Expansion & Industrial Demand

Australia Switchgear Market The Australia switchgear market is experiencing robust growth as the nation expands its power infrastructure, modernises electricity networks and integrates renewable energy sources. Switchgear — electrical equipment used to control, protect and isolate electrical circuits — plays a critical role in ensuring reliable power distribution across residential, commercial, industrial and utility sectors. According to IMARC Group, The Australia switchgear market size reached USD 1.5 Billion in 2025. Looking forward, the market is expected to reach USD 2.4 Billion by 2034, exhibiting a growth rate (CAGR) of 5.29% during 2026-2034.

By Amyra Singh2 days ago in Trader

Bruce Lee and The God of War: Kuan Ti

It starts with love.. The Power to the God Of War and Wealth Walk into a Chinese restaurant (even in Oklahoma, USA), a Chinese police station, a kung fu martial arts studio or even a Chinese temple and you often see a red faced warrior holding a heavy quan-do (spear like weapon).

By WILD WAYNE : The Dragon King6 days ago in Chapters

Comments

There are no comments for this story

Be the first to respond and start the conversation.