Saving for retirement, according to Elon Musk, will be "irrelevant" in 20 years.

According to the CEO of Tesla and SpaceX, AI, automation, and decreasing costs may alter how people plan for work, income, and retirement.

Although Elon Musk has never been known for giving conventional advice, his most recent remarks regarding retirement planning have rekindled debate regarding the future of income security, work, and wealth. The billionaire entrepreneur and CEO of Tesla and SpaceX has argued, in interviews and posts on social media over the past week, that "saving for retirement will lose its importance over the next two decades."

Musk suggested that society is moving in the direction of a world in which traditional retirement planning may simply become obsolete, rather than focusing on saving money for later life. It is a daring and provocative position that reveals as much about Musk's own worldview as it does about the shifting structure of work and technology.

Musk's argument rests on the conviction that the "future economy will look fundamentally different from the one in which the majority of retirees grew up." He believes that advanced robotics, automation, and artificial intelligence will gradually lower the cost of goods and services to the point where people will need less money to afford the necessities of life. People wouldn't need as much money in savings to live comfortably in the future if that were to happen.

In one interview, Musk stated, "If you have a decent amount of money... you’ll have freedom and flexibility, but otherwise you don't really need to save that much over your life." I believe that saving for retirement will become less important in twenty years. This viewpoint is based on optimism regarding technological advancement. Musk envisions a future in which rising productivity, largely driven by AI and automation, reduces costs to such an extent that most people no longer have to worry about their basic financial concerns.

Labor could become a choice rather than a necessity as a result of robots and machines producing much of the economy's output, and retirement savings could become an outdated tradition. That's where many everyday workers and financial professionals disagree. For most people now, saving for retirement isn’t optional. It's about staying afloat financially. People are increasingly being forced to fund their own retirement through vehicles like 401(k), IRAs, or national social security systems as a result of rising lifespans, rising costs for health care, and the demise of traditional pension plans.

The stark reality is that many workers worldwide, including those without access to employer-based savings plans or steady income, already feel unprepared for retirement. One financial planner recently stated to a major media outlet, "If you don't save today, you may be forced to work much later in life, or you may depend on social safety nets that are strained by demographic shifts."

This directly refutes Musk's implied notion that retirement planning will simply disappear. It is helpful to consider the "bigger picture of where he sees the economy heading" in order to comprehend Musk's perspective:

1. Numerous jobs will be replaced by AI and automation. Musk has long warned that many forms of labor may become less dependent on humans. Although it raises concerns regarding employment and income distribution if machines produce more of the goods and services that people want, it could theoretically reduce the need for income generation.

2. The cost of living might go down a lot. It's possible that technologies like self-driving cars and robotic manufacturing will lower the cost of goods and services. Musk suggests that the amount of money required for each person to retire comfortably may decrease when necessities like food, housing, and utilities become less expensive.

3. It's possible that redistributive policies like universal basic income (UBI) will be required. Musk has previously advocated for the concept of universal basic income (UBI), which would provide monthly payments to all citizens regardless of their employment status, as a safeguard against widespread job displacement caused by automation. Retirement savings might, in fact, look very different in such a world.

In this sense, Musk's remarks are less about encouraging financial responsibility in the present and more about depicting a different economic system in the future, one in which traditional ways of working and saving could drastically change.

Critics contend that Musk may be "overestimating the pace of economic transformation" in spite of his optimism. Although technological advancement does increase productivity, the question of whether it will happen quickly enough to eliminate the need for retirement planning is another one. It's possible that increasing the number of robots or making goods cheaper will not solve structural problems like wealth disparity, healthcare costs, affordability of housing, and demographic shifts, particularly among aging populations.

Additionally, not all trends point to a prosperous future for all. Many people's retirement security may become even more precarious if automation disproportionately benefits capital owners, or those who already control productive assets, rather than laborers. "It's not clear that lower costs alone will ensure everyone a comfortable post-work life," wrote one economist in response to Musk's remarks. Wealth distribution is important.

The majority of people who live in this day and age agree with financial experts that: Consistently save money through personal retirement accounts or employer-sponsored plans. To strike a balance between growth potential and risk, diversify investments. Prepare for the costs of healthcare and long-term living, which are unlikely to significantly decrease without structural change.

Even if Musk's vision of a low-cost future comes true, the majority of people cannot rely on it at this time. Elon Musk’s prediction that retirement saving could become “irrelevant” in 20 years reflects a broader belief in the transformative potential of technology, particularly AI and automation. It is innovative and disruptive, just like Musk himself.

However, retirement planning is still an essential part of most people's financial well-being for the time being and probably for at least the next ten years. Even in the midst of visions of a radically different tomorrow, one thing remains constant in the rapidly shifting landscape of work and wealth: preparing for the future is a prudent decision.

About the Creator

Keep reading

More stories from Raviha Imran and writers in Trader and other communities.

As banks warn of a credit crunch, Trump calls for a cap of 10% on credit card interest rates.

By proposing a broad measure that he claims would provide relief to millions of American borrowers struggling with high borrowing costs, President Donald Trump has reignited a contentious debate regarding the costs associated with credit cards by calling for a temporary cap of 10% on credit card interest rates for a period of one year.

By Raviha Imran6 days ago in Trader

Philippines Travel Technology Market: Digital Transformation, Consumer Trends & Industry Growth

Philippines Travel Technology Market Overview The Philippines travel technology market is expanding rapidly as travel operators, service providers and consumers increasingly adopt digital solutions to enhance convenience, efficiency and overall travel experiences. Travel technology — encompassing online booking systems, mobile applications, artificial intelligence (AI), cloud platforms, data analytics, digital payments and customer engagement tools — has become a strategic cornerstone for airlines, hotels, tour operators, travel agencies and transport services. The Philippines travel technology market size reached USD 214.00 Million in 2024. Looking forward, the market is expected to reach USD 361.86 Million by 2033, exhibiting a growth rate (CAGR) of 6.01% during 2025-2033. This growth reflects rising internet penetration, mobile usage, digital payment adoption and a resurgent travel demand post-pandemic as Filipinos and international tourists seek seamless digital journeys.

By Manisha Dixit5 days ago in Trader

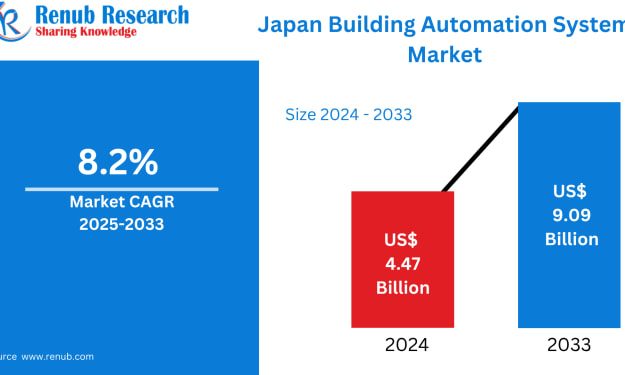

Japan Building Automation Systems Market Size and Forecast 2025–2033

Introduction Japan is undergoing a profound transformation in the way its buildings are designed, managed, and operated. From skyscrapers in Tokyo to manufacturing hubs in Aichi and logistics centers in Chiba, the demand for smarter, more energy-efficient, and digitally connected infrastructure is accelerating. At the center of this transformation lies the Building Automation Systems (BAS) market, which integrates mechanical, electrical, and electromechanical services into a centralized, intelligent control framework.

By Marthan Sirabout 19 hours ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.