Risk of Dividend Decrease for These 5 Stocks in 2023

Risk For 5 Stocks In 2023

Many investors have experienced the disappointment of a sudden reduction in dividends, leading to a drop in stock price. This can result in a diminished income stream and a significant loss in the value of one's investments.

As interest rates increase and a potential recession looms, it is likely that we will see more instances of this in 2023. Those who are successful in navigating this will be those who are able to identify strong dividends and avoid those that are at risk of being reduced.

To assist in protecting yourself from this, I have researched and identified five stocks that may be at risk of having their dividends reduced. If you currently hold any of these stocks, it may be wise to consider selling them.

If you have visited a mall recently, you may have noticed that stores have increased their inventory levels. This is a mixed news: the positive aspect is that it suggests that supply chains are recovering.

The downside is that these rebuilt supply chains are now releasing inventory that was ordered over a year ago, when demand for goods was high, resulting in overstocked shelves.

Target may not be a top choice for dividend investors due to its relatively low yield of 2.8%. However, if the company were to cut its payout, the stock would likely suffer significantly. Additionally, Target's inventory management issues, which received significant media coverage in 2022, have not improved. As of October's end, the company's inventory remained on shelves for an average of 75 days before being sold - a level not seen since before the pandemic.

This is a challenging position for Target to be in, especially with a potential recession on the horizon and rising inflation and interest rates putting pressure on consumers. Furthermore, the competition for consumer spending from services such as travel and dining out is increasing as people spend more on experiences they missed during the pandemic.

Furthermore, Target's free cash flow (FCF) payout ratio, which is the percentage of FCF used to pay dividends, is currently negative. This means that Target is paying out dividends while generating negative FCF, which is a concerning sign.

The company is making up for this shortfall by increasing its debt: long-term debt rose from $13.7 billion to $16.4 billion in the 12 months leading up to October's end. This is a significant burden to bear in today's economic environment. If you still own this stock, it is advisable to sell it now as it may remain weak for an extended period of time.

Best Buy’s 4.5% Payout Could Suffer With Tech and Retail

Which brings me to Best Buy. I have become increasingly concerned about the electronics retailer in recent weeks, even though the retail sector likely had a good holiday shopping season, I fear that it was not enough to significantly decrease BBY's high inventory levels.

As of October 31, Best Buy's inventory was sitting on shelves for about 74 days, a historically high level, similar to the level it was taking to sell in October 2021. However, at that time, sales times quickly dropped to 50 days as lockdowns drove spending on goods and supply chain disruptions limited product availability.

I do not anticipate a similar shift happening this time, especially with the possibility of a recession on the horizon.

Investors have already recognized Best Buy's sensitivity to the impact of rising rates, inflation and a possible recession, resulting in a 24% decrease in the stock's value in the past year. This has driven the dividend yield up to 4.5%.

However, it's important not to be swayed by the high yield, as the FCF supporting the dividend is under pressure. Currently, dividends account for 64% of the last 12 months of FCF, a significant increase from 27% a year ago. This puts a dividend cut in play, especially with Best Buy facing the possibility of resorting to deep discounts to clear out its overstocked warehouses.

A Slow-Motion Dividend Squeeze Could Hit These 3 Office REITs

The bottom line is that now is a challenging time for office landlords. This fact alone makes office Real Estate Investment Trusts (REITs) a risky investment, despite their high dividends.

Dividends are high in the sector, mainly because share prices have dropped significantly. For example, Vornado Realty Trust (VNO) has a yield of 9.9% and is primarily focused in New York City, where it owns or has stakes in 67 office and retail properties.

With only 48% of New York office workers back in their workplaces, it will be many months, if not years, before Vornado's retail tenants see the same level of foot traffic as before the pandemic.

Management did cut the quarterly dividend by 20% with the August 2020 payout, bringing the quarterly payout to $0.58 a share. This relieved some of the pressure on funds from operations (FFO, the best measure of REIT performance): on an annualized basis, the lower dividend amounts to 74% of the last 12 months of per-share funds from operations.

This is manageable and Vornado's tenants are mostly signed to long-term leases. However, occupancy rates are decreasing, from a peak of 97.2% in 2018 to 92.2% as of the end of 2021. With work-from-home now being permanent for many individuals, it's difficult to envision this trend reversing. Additionally, lease renewals are closely tied to employee attendance, with a lag- and this alone could eventually force office REITs to sell buildings in an already crowded market.

About the Creator

Goran Vinchi

Passion for writting

Keep reading

More stories from Goran Vinchi and writers in Trader and other communities.

Indonesia Logistics Market Analysis: Growth Potential & Market Forecast

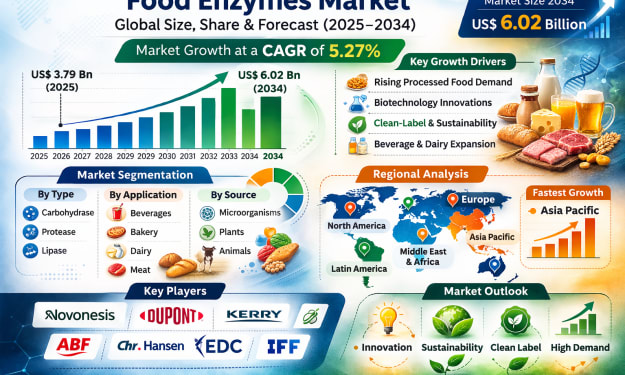

According to IMARC Group's latest research publication, "Indonesia Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region, 2026-2034", the Indonesia logistics market size reached USD 72.4 Billion in 2025. The market is expected to reach USD 132.2 Billion by 2034, exhibiting a growth rate (CAGR) of 6.91% during 2026-2034.

By Abhishek Dixit7 days ago in Trader

"Scream 7" (2026): Running out of Fresh Screams

This is the seventh time we’ve had a Ghostface crisis. Scream 7 is the latest edition of the Scream franchise. Sydney Prescott and her family are under attack by another anonymous killer dressed in a Ghostface costume. While having issues with her daughter, Tatum, they run from the bloody murders, trying to determine who is behind it all.

By Marielle Sabbag2 days ago in Horror

Comments

There are no comments for this story

Be the first to respond and start the conversation.