My $156,000 Mistake

How I Lost $156,000 to a Robo-Advisor

I did everything right. At least, that's what I thought.

At 26 years old, I decided to randomly open two accounts, one with a robo-advisor and another with private equity just to try it out. It seemed like the smart, modern thing to do. The robo-advisor app was slick. The promises were reassuring.

"Diversify," they said. "Don't put all your eggs in one basket." "We'll optimize your portfolio automatically."

So I set up automatic contributions. I didn't touch it. I didn't panic when the market dipped. What started as an experiment became one of my primary investment accounts.

Seven years later, I finally looked at the numbers - really looked at them.

Here's the thing: my other investment accounts were averaging 30–40% annually. I had TQQQ, QQQ, venture investments - all crushing it. Crypto would sometimes do 200%+ in a single year. And here's the kicker: an account I was managing myself - not knowing what the f*ck I was doing - was averaging at least 23% returns. 💀

So I assumed everything was doing well. I glanced at the robo-advisor occasionally and thought the returns looked fine.

But I was reading it wrong.

When I finally did the actual math, I realized I had invested $94,000 over those seven years. My account showed $134,000. That's a 5% annual return. Not 15%. Not 20%. Five percent.

The algorithm - the sophisticated, optimized, "smart" diversification tool - was getting destroyed by me randomly picking tech stocks with zero experience.

I was on track, but I was also $156,000 behind.

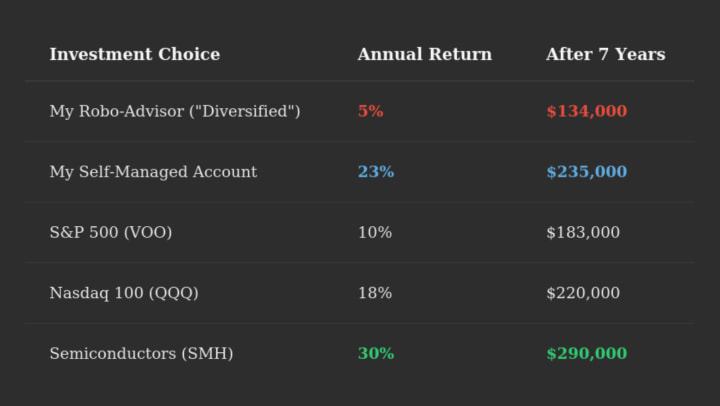

The Math That Broke Me

That same $94,000 contributed over seven years. Different investment choices:

I stared at that table for a long time.

$290,000 minus $134,000 equals $156,000. That's what my "safe" choice cost me. That's capital that could have been compounding. That's years of wealth-building, gone.

And I - a complete amateur - outperformed the algorithm by nearly 5x.

What My Portfolio Actually Held

I finally dug into what the robo-advisor had me invested in:

- IXUS - International stocks. Returned about 4% annually while US tech exploded.

- IJH - Mid-cap stocks. Went basically nowhere.

- IJR - Small-cap stocks. Same story.

- Bonds - For "stability." At 26. When I had 40 years until retirement.

Mind you, this is their most "aggressive" portfolio.

This was during the greatest technology bull run in history. AI was emerging. Cloud computing was taking over. Nvidia went up 10x. And I was holding international value stocks and bonds.

I wasn't diversified. I was diluted.

The Lie I Believed

Everyone told me to fear volatility. "What if the market crashes?" "What if you lose everything?"

But nobody told me to fear mediocrity.

Here's what I wish someone had explained to me at 26:

If the market crashes 50% when you're 26, you need a 100% gain to break even. Sounds terrifying. But at 30% annual returns, that takes about 2.5 years. By retirement, you won't even remember it.

But if you earn 5% instead of 30% for a decade? That gap compounds forever. It's not a temporary setback. It's a permanent handicap.

The real risk wasn't losing money. It was wasting time.

What I Did Next

Once I saw the math, I didn't hesitate.

I sold the entire robo-advisor portfolio that same day. First time I'd ever sold anything in my life - an unusual feeling for a diamond hands holder.

Then I did my own research. I looked at what was actually driving returns - technology, semiconductors, innovation. I built another portfolio around conviction, not "diversification for diversification's sake."

One of my first buys was SMH. Ironic, to say the least.

No more international small-caps. No more bonds in my twenties. No more trusting an algorithm to do what I should have been paying attention to myself.

What You Need To Know

I'm sharing this because I wish someone had told me sooner to stop f*cking around and trust the things you're doing that already work.

I didn't need this experimental portfolio. I didn't need to test things out. I didn't need to trust a robot.

"Diversification" and "playing it safe" are not inherently good strategies.

They're marketing terms that make financial advisors sound smart and make you feel comfortable while your wealth quietly stagnates.

Here's what I learned:

Time is everything. If you're young, volatility is your friend. A 50% crash in your twenties is a buying opportunity. A decade of 5% returns is a catastrophe.

Conviction beats diversification. I'd rather own 5 things I believe in than 50 things I don't understand. I'm bullish on tech, AI, space, and robotics.

Behavior beats stock picks. The best portfolio is worthless if you panic sell at -30%. Diamond hands beat diversification every time.

Run the damn math. Don't just accept "you're on track." Calculate what you could have. The difference between 5% and 30% isn't small - it's life-changing.

The Gyst

- I lost $156,000 because I believed "safe" was smart.

- I lost $156,000 because I was not fully paying attention to the experiment I was running.

- I lost $156,000 because I trusted an algorithm that optimized for low volatility instead of high returns.

- I lost $156,000 because nobody told me that the biggest risk for a young investor isn't losing money - it's wasting time.

So here's my advice: Run the numbers on every account you have. Don't just glance at it - actually calculate your annual returns. Compare them. Ask yourself if "diversified" is really helping you, or just making you feel comfortable while you fall behind.

Time is your most valuable asset. Don't waste it earning 5%.

Note 1: I also sold another account that was doing 13%. I just can't cope with mediocre returns, when you can easily get 20% from a simple ETF.

Note 2: The private equity account is going strong. At least something panned out from those two decisions. 😑

-

Disclaimer: This article reflects my personal experience and is for educational purposes only. It does not constitute financial advice. Past performance does not guarantee future results. Consult a financial advisor before making investment decisions.

About the Creator

Destiny S. Harris

Writing since 11. Investing and Lifting since 14.

destinyh.com

Keep reading

More stories from Destiny S. Harris and writers in Trader and other communities.

Gaming Market: The Rise of Digital Entertainment Worldwide

Overview The global gaming market stands as one of the largest and most dynamic entertainment industries worldwide, spanning video games on consoles, PCs, mobile devices, cloud gaming, and esports. Fueled by technological innovation, expanding internet access, and a diverse global audience, revenue continues to rise year after year. In 2025 alone, industry estimates suggest the gaming market could approach near $200 billion in annual revenue, with mobile games accounting for more than half of that total.

By James Smith4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.