Mexico Residential Real Estate Market Size and Forecast 2025–2033

A Market Shaped by Urban Growth, Nearshoring, and Lifestyle Migration

Mexico Residential Real Estate Market Overview

The Mexico Residential Real Estate Market is entering a decisive growth phase, supported by demographic expansion, urbanization, foreign investment inflows, and structural economic shifts. According to Renub Research estimates, the market is expected to grow from US$ 13.93 billion in 2024 to US$ 21.1 billion by 2033, registering a compound annual growth rate (CAGR) of 4.72% during 2025–2033.

Demand for housing is being driven by a mix of first-time homebuyers, internal migrants, and international buyers seeking second homes or long-term stays. Mexico’s strong tourism ecosystem, cultural appeal, and comparatively affordable property prices continue to attract retirees and remote workers, particularly from North America. At the same time, nearshoring and industrial expansion are transforming residential demand patterns in northern and central regions of the country.

Mexico Residential Real Estate Industry Outlook

Mexico’s residential real estate sector has evolved into a dynamic and multi-layered market. Population growth, a steadily expanding middle class, and accelerated urban development are pushing demand across apartments, condominiums, villas, townhouses, and gated communities. Large metropolitan areas such as Mexico City, Monterrey, and Guadalajara remain at the heart of residential development, supported by infrastructure upgrades, employment generation, and improved access to mortgage financing.

Government-backed housing initiatives and looser mortgage conditions have increased affordability for middle-income families. Simultaneously, the market is witnessing growing interest in smart homes, energy-efficient buildings, and sustainable residential projects, reflecting changing consumer preferences and long-term cost considerations.

Despite its promise, the industry faces structural challenges. Regulatory complexity, land tenure issues, and regional variations in zoning and permitting processes can delay projects and raise costs. Even so, Mexico’s residential real estate market continues to benefit from both domestic resilience and global economic integration.

Historical Performance and Pricing Trends

Mexico’s housing market has shown notable resilience over the past decade. National house price indices recorded consistent year-on-year growth, with strong appreciation observed between 2018 and 2022. After a brief slowdown during the COVID-19 pandemic, prices rebounded sharply as pent-up demand returned and construction activity resumed.

By late 2023, housing prices were rising again across most regions, although trends varied locally. According to data cited by Statista, Mexico City remains the most expensive residential market in the country, with average property prices exceeding MXN 2.9 million (approximately USD 148,000). Premium neighborhoods such as Condesa, Polanco, and Roma command some of the highest price-per-square-foot rates due to their architectural appeal, lifestyle offerings, and proximity to business hubs.

Interestingly, a segment of homeowners in major cities has begun relocating to suburban or secondary markets, either seeking larger living spaces or investing abroad. This trend is reshaping demand across peripheral regions and mid-sized cities.

Key Growth Drivers in the Mexico Residential Real Estate Market

Urbanization and Population Growth

Urbanization remains one of the most powerful drivers of residential real estate demand in Mexico. More than 80% of the population now lives in urban areas, and this proportion continues to rise. Major cities are expanding outward, while vertical housing projects are becoming increasingly common due to land scarcity and affordability constraints.

Young demographics play a crucial role in shaping demand. A large proportion of Mexico’s population is under 35, and many are entering the housing market for the first time. This demographic shift fuels demand for affordable apartments, starter homes, and rental properties close to employment centers and transport infrastructure.

Internal migration from rural to urban areas, driven by better job prospects and access to services, ensures sustained demand for new residential supply. Both public and private developers are responding by expanding housing projects across price segments.

Economic Decentralization and Nearshoring

Mexico’s growing importance in global supply chains has significantly altered regional real estate dynamics. Nearshoring—particularly by U.S. manufacturers—has accelerated industrial investment in northern states such as Nuevo León, Chihuahua, and Baja California.

As factories, logistics parks, and industrial corridors expand, they create employment hubs that drive demand for nearby residential developments. Workers, managers, and executives seek housing close to industrial zones, stimulating construction of both affordable housing and upscale residential communities.

Economic decentralization policies and infrastructure investments are also encouraging growth in mid-sized cities. New highways, rail links, and airport expansions have improved connectivity, making secondary cities more attractive for residential development. Nearshoring, therefore, has emerged as a structural growth engine for Mexico’s residential real estate market.

Lifestyle Migration and Second-Home Demand

Mexico continues to attract international buyers looking for second homes, retirement properties, or extended holiday residences. Coastal regions, colonial towns, and culturally vibrant cities remain popular among foreign nationals seeking lifestyle-oriented investments.

The rise of remote work has further strengthened this trend, as professionals relocate to Mexico for longer stays while maintaining overseas employment. This has boosted demand for furnished apartments, gated communities, and mixed-use residential developments that offer security and amenities.

Challenges Facing the Mexico Residential Real Estate Market

Regulatory Complexity and Land Tenure Issues

One of the most persistent challenges in Mexico’s residential real estate sector is regulatory complexity. Developers often face lengthy approval processes involving zoning, environmental permits, and municipal authorizations. Overlapping jurisdictions and inconsistent enforcement across regions add to uncertainty and cost.

Land tenure issues, particularly in ejido (communal land) areas, can delay or derail residential projects. Legal ambiguities surrounding ownership and property rights increase investment risk and discourage smaller developers. Addressing these regulatory inefficiencies will be essential for scaling housing supply and improving market transparency.

Economic Volatility and Interest Rate Fluctuations

Macroeconomic factors such as inflation, currency movements, and interest rate changes also influence residential real estate demand. Rising interest rates increase mortgage costs, making homeownership less affordable for first-time buyers and low-income households.

Inflation erodes purchasing power and raises construction costs, affecting project viability. Periods of global economic uncertainty can also dampen foreign investment, particularly in higher-end residential segments. While Mexico’s housing market has proven resilient, sustained volatility remains a risk to long-term affordability and growth.

Regional Analysis of the Mexico Residential Real Estate Market

Northern Mexico

Northern Mexico has emerged as one of the fastest-growing residential markets in the country. Industrial expansion and nearshoring have fueled strong housing demand in cities such as Monterrey, Tijuana, and Ciudad Juárez. Developers are responding with a mix of affordable housing, middle-class neighborhoods, and luxury suburban projects.

Improved infrastructure, better security conditions, and proximity to the U.S. border make the region attractive to both domestic and foreign buyers. However, rapid growth also places pressure on infrastructure and public services, requiring coordinated urban planning.

Central Mexico

Central Mexico, anchored by Mexico City, remains the largest and most diverse residential real estate market. Demand spans luxury condominiums in premium districts to affordable apartments in suburban municipalities.

Satellite cities such as Toluca, Querétaro, and Puebla are experiencing increased residential development due to improved transportation links and lower living costs. Developers are focusing on vertical and mixed-use projects to address land scarcity and traffic congestion. Despite high land prices and bureaucratic hurdles, Central Mexico continues to dominate national residential activity.

Southern Mexico and Other Regions

Southern Mexico presents long-term potential, supported by tourism development and infrastructure initiatives. While demand is currently lower than in the north and center, improving connectivity and economic diversification are gradually enhancing the region’s residential outlook.

Market Segmentation

By Property Type

Apartments

Villas

Condominiums

Towns

Gated Communities

By End User

First-Time Home Buyers

Second Home Buyers

Rental Investors

Institutional Investors

By Region

Northern Mexico

Central Mexico

Southern Mexico

Others

Competitive Landscape and Company Analysis

The Mexico residential real estate market features a mix of established national developers and diversified infrastructure players. Leading companies include Ruba, Consorcio Ara, Sab de CV, Grupo Garza Ponce, Grupo Lar, Grupo Jomer, Grupo HIR, Inmobilia, Grupo Sordo Madaleno, Aleatica, and Ideal Impulsora Del Desarrollo.

These companies are evaluated across multiple dimensions, including business overview, leadership, recent developments, SWOT analysis, revenue performance, and strategic positioning. Their investments in large-scale residential communities, mixed-use projects, and infrastructure-linked developments are shaping the future of Mexico’s housing market.

Final Thoughts

The Mexico Residential Real Estate Market stands at a pivotal moment. Supported by urbanization, demographic momentum, nearshoring-driven economic growth, and lifestyle migration, the sector is poised for sustained expansion through 2033. While regulatory hurdles and economic volatility present ongoing challenges, the market’s fundamentals remain strong.

With a projected valuation of US$ 21.1 billion by 2033, residential real estate in Mexico offers compelling opportunities for developers, investors, and policymakers alike. Strategic reforms, infrastructure investment, and sustainable urban planning will be key to unlocking the market’s full potential and ensuring inclusive, long-term growth.

About the Creator

Marthan Sir

Educator with 30+ years of teaching experience | Passionate about sharing knowledge, life lessons & insights | Writing to inspire, inform, and empower readers.

Keep reading

More stories from Marthan Sir and writers in Trader and other communities.

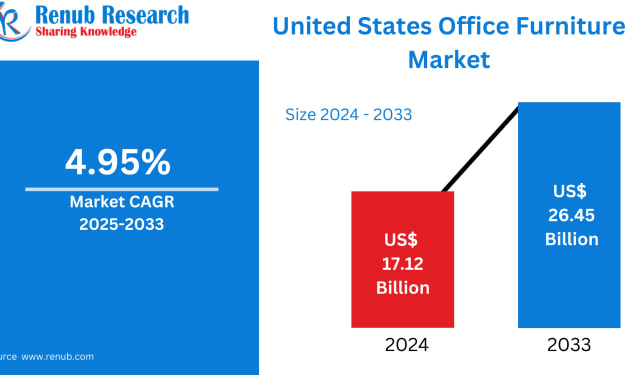

United States Office Furniture Market Size and Forecast 2025–2033

United States Office Furniture Market Overview The United States Office Furniture Market is entering a transformative decade as workplaces evolve in response to hybrid work models, employee wellness priorities, and rapid technological integration. According to Renub Research, the market is expected to grow from US$ 17.12 billion in 2024 to US$ 26.45 billion by 2033, expanding at a CAGR of 4.95% during 2025–2033.

By Marthan Sir14 days ago in Trader

Tesla share price drives investor emotions as Wall Street balances risk, reward, and confidence

Tesla share price plays a major role in how investors think and act each day. From small traders to large funds, many people watch Tesla share price closely before making decisions. A small rise can bring hope, while a sudden fall can create fear. This article explains how Tesla share price influences emotions, decisions, and long-term plans. It also helps readers understand how to approach Tesla share price with a calm and smart mindset.

By hamza mirza5 days ago in Trader

Day 4 of Quitting

If this is how sobriety feels, maybe it’s better to go through life a little buzzed… this, along with other hits like, I want to kill myself, I wish I was dead, and I’m going to throw myself off a bridge have been the only thoughts on rotation these past few days. I promise myself that if, in a month, I still feel like this (‘this’ meaning despondent, full of rage, and simultaneously numb) I can go back to smoking. Until mid-February though? Nicotine is off the table.

By sleepy drafts4 days ago in Longevity

Comments

There are no comments for this story

Be the first to respond and start the conversation.