Learn from scratch how to manage your investments yourself

Investing money on your own brings many benefits

Three years ago we accumulated about five thousand euros (about six thousand dollars) from friends and family after our son was born. This is a common custom in our country, Bosnia and Herzegowina, but probably in many other countries as well. My wife’s idea was to keep that money in his savings account and give it to him once he turns 18. I could not stop shaking my head and hitting imaginary slaps on my forehead. My wife is well-educated but does not know much about investing and is no expert in economics. I started unwrapping, one layer after another, and patiently explaining to her why that idea was foolish.

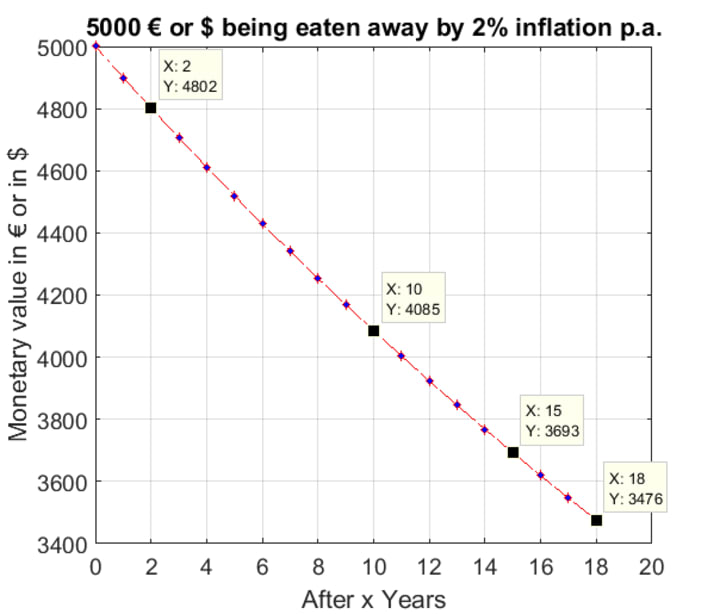

First, there is inflation. In Europe and the U.S., it is somewhere around two per cent, but that adds up over the years. Allow me to illustrate. As the time-horizon, I am picking 18 years because of our son and his college savings fund but the points I want to make in this article are the same as for any other long-term horizon. I want you to understand and ponder over the next crucial figure about the loss of monetary value.

How money loses value over the years, assuming an average inflation rate of 2% per annum.

Source: Author

As you can read in the figure, after 18 years of uninvested money and assuming an average inflation rate of 2% per year, the money’s worth will be around 3500€ in today’s money, once our son turns 18.

Second, there would be an opportunity cost of leaving money uninvested.

This story’s target audience is people who have some money on the side, but limited knowledge about investing, maybe even fear.

The age of the target audience of this article is people in their 20s and 30s and low 40s who have at least 20 years left until retirement. The second prerequisite is for them to have some liquid savings or the potential of putting aside a fixed amount each month for investment.

Why invest in stocks and not in something else

Everyone setting out to invest should know beforehand about the options he has. Some instruments take up too much transaction costs, others, like cryptocurrencies, fluctuate too much and you can potentially lose a lot of money very quickly. For new investors, the reasonable options are savings accounts, an investment fund plan where you invest each month into an actively managed fund, or ETFs (for an explanation, see the last section).

Savings accounts in banks currently yield some 0.1% in the European Union and maybe slightly more in the U.S. That is like nothing in the investing world. The second alternative is investment funds managed by your bank. which usually charge high performance and management fees while at the same time not many of them have a track record where they outperformed the market repeatedly. So, why pay someone high fees to more or less guess the market, something you could do as well after some months of learning by doing.

Investing is a marathon run over decades

I was provoked to speak out in the hope this article might help many of you trigger some interest towards educating yourself on how best to invest your money wisely. Some of you might, indeed, start following my piece of advice and start investing yourself.

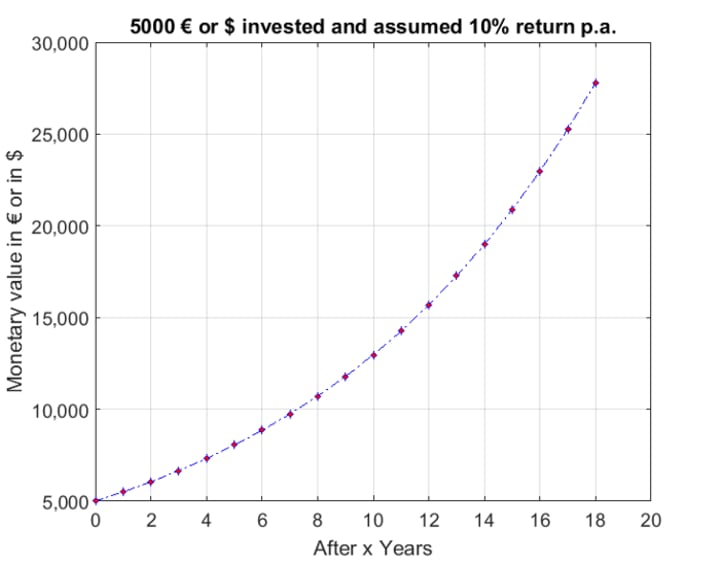

Firstly, let me deliver some basic, and maybe deterring truths: investing is a 42 something kilometres run, not a 100-meter sprint and this article is not about how to get rich quickly nor how you can build up passive income on the side. Although you would have an additional income stream from dividends and potential stock price gains, those gains should stay in that investment pot which you ought to touch only for pre-agreed purposes and in cases of proper emergencies. The reason why you should not eat up your dividends is because of a concept called compounding. Compounding is very powerful, but you see its effect only after many years (see in the next two figures).

Investing 5 thousand and making an annual return of ten per cent on average will yield 27,000 after 18 years. Source: Author

One possible scenario for your investment path is shown here. I assume a starting amount of 5000 and adding 2500 each quarter. The power of compounding yields you almost 800 thousand by 2040 while having invested 200 thousand of hard cash by then. The assumption is that you get a ten per cent return per year.

Source: Author

Source: Author

Have a look at the excel spreadsheet calculations in the picture above. I assume a time horizon of 19 years, 2500 dollars or euros to be added to your investments at the end of each quarter and I assume the performance of ten per cent on average per annum. In 2040 you might potentially end up with almost 800 thousand while putting in close to 200 thousand of hard cash in total by then. That is the power of compounding at its best. The excel file can be obtained upon request from me if you want to experiment with your own numbers.

As a side note, ten per cent is not far fetched for the stock market. According to Investopedia the average stock market return from 1926 until 2018 was 10–11%, where there is much discussion about definitions and periods observed. Also, one needs to account for inflation. Then you get to 7%, also according to the same source.

Main principles to know before investing

Before setting aside parts of your savings to invest into more risky assets, like stocks, real estate investment trusts, or maybe even gold, I want to transmit few basic principles of investing that I wish I knew upfront.

There is no free lunch: one of the economics basics! If the stock price of a company looks cheap, you might deep dive into the reasons why the investing community regards it as cheap. There must be some reasons. If you take home only one message from my article, I would wish it to be this principle. In general, throughout your life, always know whenever there is an opportunity to make lots of money quickly, be stringently aware, the opportunity to lose as much is maybe more probable.

Emotions while investing need to be understood and taken control of: on your journey, you will have many ups and downs and once a trade runs against you, it is essential to not be like a gambler in the casino who keeps playing to make up the initial loss. Another word from poker is tilt. You will need to avoid and control those reactions.

Compounding will make you rich over the long-term: Compounding is a strategy that has worked for many smart investors over history. It requires discipline and patience, though.

How to start investing yourself

Phase 1: paper trading first

I would like to propose a cautious approach for those who are a bit more risk-averse. I know, it takes more time until you start investing yourself, but it will be worth the extra mile. This phase can take up some three to six months. Do not underestimate it and start trading after three weeks of good paper profits and start being infected by hubris.

I propose you start paper trading first. Paper trading means you open up a free broker account and do not use real money, but paper money and you play the investing game first.

Phase 2: real investing into two to three companies only

First, open a proper broker account. Do your research as to which one suits you best and does not charge a lot per trade. I am sure after a few Google searches and one or two hours spent on some geeky investment forum, you will figure out the best broker for your needs. I could get extra money by promoting my current broker, but I do not want you to think that the motivation for this article had a hidden agenda.

My suggestion is to look around you and identify a company that you think might do well in the future, a company whose product you love and you would be happy about the fact owning a part of that company. This can be anything that you can morally justify. Maybe you should not invest in an arms-producing nor a tobacco company. It can be Ford because you love the F-150, it can be Ferrari, maybe Twitter, Google, maybe General Electric because as an engineer you love the aeroplane engines they produce, or maybe Pfizer, because you are a doctor and know, how well some of their medication works.

Now comes the second step after identifying few candidates. You need to check if …

a) … this company is public, meaning if you can buy shares of this company or if it is just private (e.g. held by founding family, like for example IKEA) and

b) … the stock price of the identified company is a good bargain.

The answer to the first question can be found quickly, the crucial step lies in the second question, though.

What is a good bargain? A nice mansion on a Californian hill might be valued at one million dollars on a normal day, but facing a fire quickly approaching towards it, if someone offers you the house for 250 thousand, I am not sure it would be considered a bargain as opposed to on a usual day. Now imagine, you are an expert on physics and fire (if something like this even exists) and you estimate the likelihood of the fire catching that specific house is somewhere between ten and 20 per cent. Would you now buy it for 250 thousand? — I would! The mathematical concept behind this reasoning is expected value, an average of scenario outcomes, weighted by corresponding probabilities.

The same applies to stocks. Many participants believe to know better than the market. But even when a trade turns out to be a great investment, it does not mean it was a prudent decision at the time you invested. The same applies to bad trades. In the same way, you can bet your house on the next Lakers game, be lucky and win, but it was not the smartest decision in your life before the game.

How to spot a good business at a fair price

There are many books written on the topic of valuing a company or determining if its stock price is traded at a fair price. The finance industry likes to toss around with fancy-sounding words and jargon expressions just to emphasize their knowledge and justify the high fees they charge for their services, but mostly behind those fancy words and acronyms, there lies a simple economic principle. Let us say, a friend of yours offers to sell you a part of his bakery/coffee shop because he needs cash. He would continue to operate it for a salary, so you would just be a financial shareholder and not having to quit your job to run it. What are your first three questions? Think about it first, do not keep reading on.

You want to ask him what his revenues were and costs split into cost components of fixed and variable costs. Then you can figure out her profit.

You might ask if he has any assets in form of machines, furniture, and cash sitting in the bank account as a reserve for bad times so he can pay his employees in a bad month.

After knowing all these figures, you are interested in knowing which amount she is selling her bakery/coffee shop.

The questions thrown at in the previous two sections are exactly those you want to be answered before investing in a company. Owning stocks of a company means, you own small fractions of that company, so you want the same questions answered like when confronted with the possibility to buy your friend’s bakery/coffee shop.

Reading balance sheets of companies is a very complex and serious issue. It stretches over many semesters at university for students of business. I can not break it down into two sentences. But you can start small. And build your knowledge in this area on the way as you invest in companies.

Let us do the first step together and then in my next articles, if there is an interested audience, I will go deeper into this segment.

A crucial metric when investing is called the Price-to-Earnings (PE) ratio. After how many years, can you earn back your investment? Imagine you want to install solar panels onto your roof. The investment costs you 16 thousand, and you calculate to earn some 1200 dollars a year from the electricity you produce. The PE ratio would be 16000 divided by 1200 which equals 13.3 years. The difficulty comes when estimating the earnings for the future for many highly complex and uncertain business environments.

Phase 3: building a diversified stock portfolio

I want to quote Peter Lynch, a successful fund manager, in this context:

… it isn’t safe to own just one stock, because, in spite of your best efforts, the one you choose might be the victim of unforeseen circumstances.

In this phase, you should think of building a diversified portfolio to be prepared for various world economy scenarios. This will be explained in subsequent articles.

Legitime alternatives to stock picking

There are two alternatives to picking stocks: buying ETFs (passively-managed funds) or buying actively-managed funds. If you choose this path, you will have to do a good amount of research on the many different ETFs and funds. They differ a lot with regards to what collection of stocks they own and how much they charge you for their service of picking the stocks or of balancing a portfolio to mimic some index.

Short explanation about ETFs according to Wikipedia:

Most ETFs are index funds: that is, they hold the same securities in the same proportions as a certain stock market index or bond market index.

A stock market index is usually the basket of all the largest stock market companies of a country or economic sector.

In Conclusion

I would love it if I was able to convince someone to start this journey. It will change your life about looking at economics, money, investments, banks and the many clerks working at banks and trying to (cross-) sell you stuff.

If this article sparks enough interest I will keep on peeling one layer after another and support you with the knowledge that I have gathered over the previous years.

About the Creator

Keep reading

More stories from Mirsad Tulic and writers in Trader and other communities.

Why Most Crypto-pushing Articles and Videos are Useless

Some people retired early because of bold bets on bitcoin or whatever coin was the new trend, but those stories should not and must not urge you to invest in cryptocurrency unless you know what you are doing. Bear in mind that those cases get media presence but the millions who lost a few thousand dollars do not, nor do the few thousand cases who lost almost all their savings.

By Mirsad Tulic4 years ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.