Kevin O'Leary's Advice On How Much Should You Spend On Housing

Housing plans made easy

If you are a young adult, one of the milestones that you will probably want to achieve one day would be to own your own home. It provides a sense of independence, ownership and something that you can call your own.

For most people, homeownership provides a sense of stability, pride and comfort knowing that in a time of crisis they have a place to live. For others, renting may seem to make more financial sense especially if the cost of renting compared to buying is lower and if they aren't sure if they will stay in a single place long term.

Here is the natural progression for most people:

Go to school> College- Graduate> Get a job> First home and car> Get married> Have kids > Retire

Kevin O'Leary (one of the judges on Shark Tank) has a simple method of finding out if you should rent or buy your own home.

Renting vs Buying

According to Kevin O'Leary and CNBC's Money Court, the advice is to follow the 1/3 rule, which calls for a third of your after-tax income.

Here is the breakdown:

- 1/3 to go toward living expenses

- 1/3 to go towards home

- 1/3 to go towards savings and investments

Additionally, the government has recommended that people spend no more than 30% on housing costs since 1981.

The reason behind this is that if you spend more, you are going to put tremendous stress on yourself according to Kevin O'Leary. There is this cost burden and financial strain to meet the monthly mortgage payments when you have a larger portion of the pie to contribute.

What does this 1/3 include for renters and owners?

- Renters: For renters, this includes utility costs like heat, water and electricity.

- Owners: For owners, this includes homeowners insurance, property taxes, utilities and your mortgage.

In major cities like San Francisco, New York, London, Paris, Tel Aviv etc, it may be difficult to stick to the "one third-one third-one third" rule. However, it should hopefully serve as a yardstick of measure for each person planning to buy or rent a place.

Kevin O'Leary's advice would be to be patient and wait for one within your budget than to spend more than you can afford.

What do other experts say?

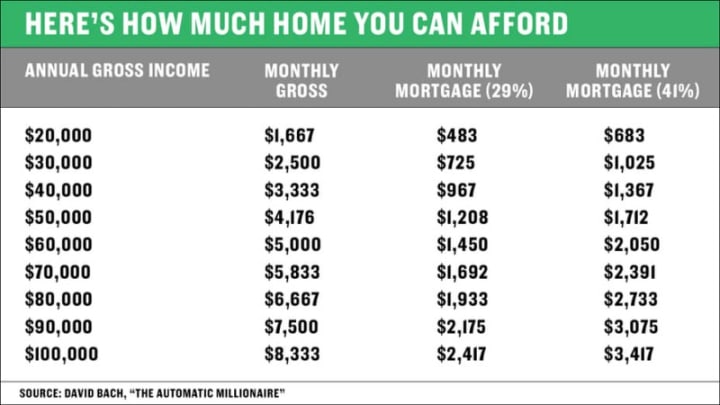

If you are familiar with David Bach, author of many good personal finance books including "The Automatic Millionaire" he offers a slightly different take.

Based on the Federal Housing Association, a good rule of thumb is that most people can afford to spend 29 per cent (close to 1/3 of their income) of their gross income on housing expenses and as much as 41 per cent if they have no debt.

The following numbers can be applied to rent, Bach notes. So for example if you earn :

- $40,000 a year, you should be able to spend at least $967 a month and up to $1,367 a month in the form of either rent or mortgage payments.

- $70,000 a year, you should be able to spend at least $1,692 a month and up to $2,391 a month in the form of either rent or mortgage payments.

- $100,000 a year, you should be able to spend at least $2,417 a month and up to $3,417 a month in the form of either rent or mortgage payments.

Is there another benchmark guide?

Yes, there is. They call it the "28/36 rule," which says that you should spend

Buy What You Can Afford

Indeed, temptations abound for borrowers to overspend on a house given the tight supply, which may happen amongst some borrowers.

Some of the advice includes:

Daniel Goldstein, an agent with Keller Williams Capital Properties in Bethesda, Maryland:

"Don't count on income growth to help you grow into that payment to get used to it," said Goldstein. "If you are anticipating getting that $500-a-week extra income from your side job or your overtime and it disappears, you're really in trouble."

Bruce McClary, senior vice president of communications at the National Foundation for Credit Counseling (NFCC):

"Don't go into this with your eyes bigger than your stomach when it comes to your appetite for borrowing. The bigger the home and loan, the bigger the commission a realtor or mortgage broker will make".

Conclusion

Ultimately, to figure out how much you can afford to spend on housing, keep these guidelines in mind, but also look at your budget and consider your long-term saving goals.

At the end of the day, figuring out how much you to allocate on housing can help you plan realistically and bring your goals to fruition while being wise with your finances.

----------------------------------------------------------------------------------------

If you would like to support my writing, please consider liking my story, subscribing, pledging and/or tipping. Thank you for reading!

About the Creator

Stanislav Kondrashov Explains How Circumvention Drives Technological Innovation

Technological progress rarely moves in a perfectly predictable direction. Breakthroughs often happen when traditional solutions stop working and innovators are forced to search for alternative paths. Instead of pushing directly through a challenge, they find a way around it. This approach — commonly described as circumvention — has played a quiet but essential role in shaping modern technology.

By Stanislav Kondrashov5 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.