How much should you have saved at every age?

Money made easy

How much you should be saving for retirement is an age-old question that just about everybody wants to know.

The amount you need depends on:

- How old do you plan to retire?

- How much do you want annually upon retiring?

Extensive analysis has been done by many organisations to come up with age-based retirement savings factors that can help you plan for retirement. These milestones are aspirational.

You likely won’t meet all of them due to changes along the way. But they can serve as goalposts to help you make a plan to save enough to maintain your lifestyle upon retiring.

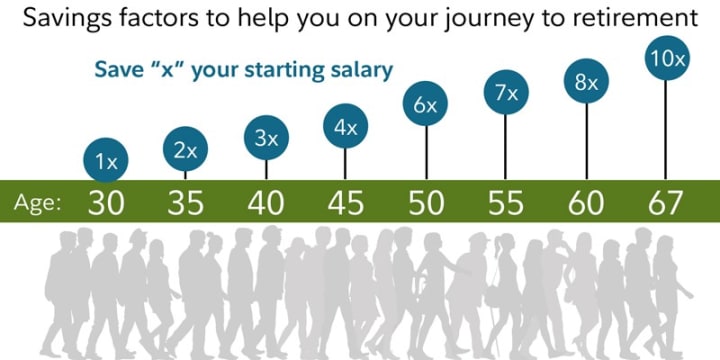

How much should you have saved at each age?

Here’s how much cash they say you should have stashed away at every age:

- By age 30: the equivalent of your annual salary saved: if you earn $55,000 per year, by your 30th birthday you should have $55,000 saved.

- By age 40: three times your income

- By age 50: six times your income

- By age 60: eight times your income

- By age 67: ten times your income

What investment vehicles to use?

If you're based in the States:

- Max out your Roth IRA ($6,000 limit in 2021 and $7,000 for age 50 and older).

- Contribute to your employer-sponsored 401(k), especially if there is a match (that’s free money for you!).

- Savings, certificates of deposits, bonds, loan notes, and treasury bills.

- Investment accounts

- Real estate

- High yields savings account

If you are based outside of the United States:

- Invest in a private retirement scheme.

- Contribute to a personal pension plan or a work pension plan, especially if there is an employer-sponsored pension (you get free money!).

- Savings, certificates of deposits, bonds, loan notes, and treasury bills.

- Investment accounts

- Real estate

- High yields savings account

How do you want to live in retirement?

- Do you expect your expenses to go down when you retire? We call that a below-average lifestyle.

- Or will you spend as much as you do now? That’s average.

- If you expect your expenses will be more than they are now, that’s above average.

For eg, let's say investors all plan to retire at 65. The below chart will give you an idea of how much to set aside for retirement.

- Joey is planning to downsize and live frugally in retirement, so he expects his expenses to be lower. His savings factor might be closer to 8x his annual starting salary.

- Monica plans to maintain her standard of living upon retiring. Her savings factor would ideally be 10x her annual starting salary.

- Chandler plans to travel extensively upon retiring, hence, he may want to have a larger amount saved up to accommodate this, and 12x his annual starting salary at his retiring age of 65 might make sense for him.

Maybe you want to retire early? Median income?

This can be a viable option as well if you calculate how much you need to set aside currently until you reach your desired retirement age.

The goal for an average person will be to have a million dollars upon retiring. About six in 10 Americans (58%) think that $1 million will be enough for “a comfortable retirement.” That’s according to TD Ameritrade’s 2019 Retirement Pulse Survey, which surveyed 1,015 U.S. adults ages 23 and older with at least $10,000 in investable assets.

The median necessary living wage across the entire US is $67,690.

The median necessary living wage across the UK is £31,460. (around $42,631)

You can see the median income by different countries below here:

- Median Income By Country 2021

For the most part, you will want to calculate and look at the net income, not the gross annual income. After all, the tax payable amount is the amount automatically deducted from your payslip. You only have control of the net amount which is the amount that you receive in your bank account.

You can aim for the $1m pool of funds or a $500k investment earning a 7%- 10% annual interest return if you plan to retire comfortably at retirement age, 65 onwards.

F.I.R.E

For others that plan to retire early, there is this whole movement on Financial Independence Retire Early (FIRE) online that centres on retiring early and achieving financial freedom at an early age.

How much do you need to contribute monthly to retire early?

On average if you have a $450,000 to $500,000 invested in a fund that generates you 8% return per annum, you would get an annual income of $40,000 (8% x $500,000) which is a decent average annual net income for most people. It's a decent median income to live off, pay mortgage/rent, buy food, etc.

You can adjust this pool of money to a higher or lower amount depending on the annual net income you would like to receive per year.

So the goal would be to ask yourself how do I get to the $500,000 as soon as possible? Assuming an annual rate of return of 7%, taking into account inflation.

If you start at 25 years old and plan to retire at different ages (30, 40, 50, 60 etc….) the amount you need to contribute monthly is as follows:

- 5 years invested — retire at 30: $6,984 monthly contributions

- 10 years invested — retire at 35: $2,889 monthly contributions

- 15 years invested — retire at 40: $1,577 monthly contributions

- 20 years invested — retire at 45: $960 monthly contributions

- 25 years invested — retire at 50: $617 monthly contributions

- 30 years invested — retire at 55: $410 monthly contributions

- 35 years invested — retire at 60: $278 monthly contributions

- 40 years invested — retire at 65: $190 monthly contributions

These milestones are estimates. You likely won’t meet all of them. The interest rate of returns could change year on year, the rate of inflation could change, the amount that you can contribute may change and other external factors beyond one’s control. But for the most part, they can serve as a benchmark to help you make a plan to save enough to maintain your lifestyle in retirement.

Fidelity recommends that you save 15% of your income each year (since age 25) and that, over your lifetime, you invest more than 50% of your savings in stocks to get a higher return on your money, retire at age 67, and continue to maintain this pre-retirement lifestyle in retirement.

Conclusion

Retiring early isn’t some far fetched dream that is impossible. Anybody can achieve this if they truly want to. It's challenging, it's tough, but it’s not impossible.

Believe it or not, you can still achieve your financial goal without starting a business, inventing something or doing anything drastic from your current life. By saving consistently and making use of the power of compounding interest you can actually achieve financial freedom.

It just comes down to:

- knowing how much to set aside each month and

- how passionate you are about retiring early.

Now that’s thinking ahead!

----------------------------------------------------------------------------------------

If you would like to support my writing, please consider liking my story, subscribing, pledging and/or tipping. Thank you for reading!

About the Creator

Automotive Actuators Market Size and Forecast 2026–2034

Automotive Actuators Market Outlook The global automotive industry is rapidly transforming as vehicles become increasingly electrified, connected, and automated. Within this evolving ecosystem, automotive actuators play a crucial role in enabling modern vehicle functions. According to Renub Research, the global Automotive Actuators Market is expected to grow from US$ 21.18 Billion in 2025 to US$ 34.91 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.71% between 2026 and 2034.

By shibansh kumara day ago in Trader

Stanislav Kondrashov on Nikkei Volatility and the Global Economic Signals Behind It

The beginning of the week has brought renewed turbulence across several major financial markets. Indices such as the Nikkei 225 in Japan, Germany’s DAX, Switzerland’s SMI, and the Dow Jones in the United States have all shown sudden movements that reflect a broader atmosphere of economic uncertainty.

By Stanislav Kondrashovabout 3 hours ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.