How much do you need to invest to be a Millionaire if you start at 25-years-old?

Money made easy

Many of us would like to be millionaires, however, how much do we need to get there? There are plenty of variables that go into calculating an amount. However, having a rough ballpark figure can be very helpful in working towards an amount that is known.

Retirement Savings Stats and Facts

- The median retirement savings are $65,000.

- The median retirement savings for people aged 55–64 are $120,000.

- The average amount of retirement income for households aged 60–64 is $100,842.

- 40% of workers estimate they will need at least $1 million for retirement.

- Households aged 65–74 have a net worth of $1,217,700 at retirement.

- 68% of workers think they will need to work for income in retirement.

Based on the statistics you can see almost 40% believe they need at least $1 million in this lifetime to live a decent life.

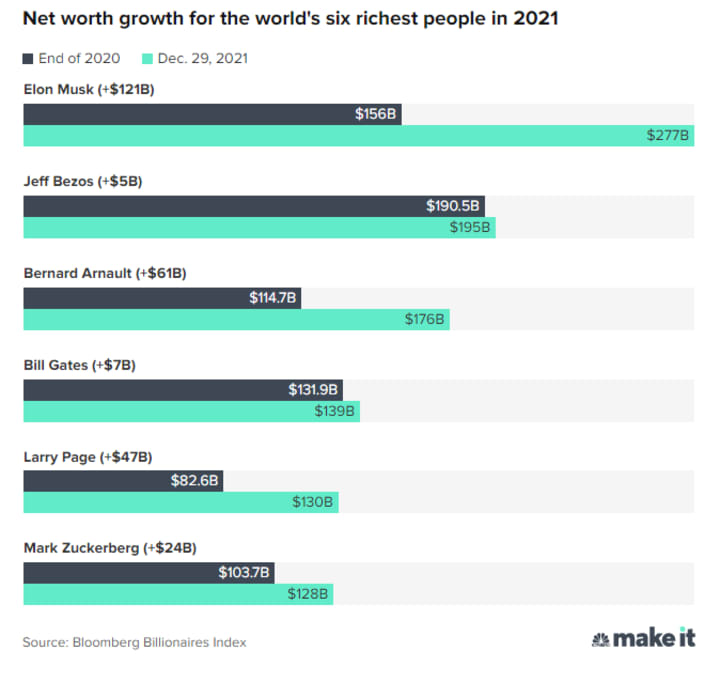

To put the amounts of the ultra-wealthy into perspective have a look below:

- You need $1,000,000

- Jeff Bezos has $195,000,000,000

The truth is most people, don't even reach that $1million mark in this lifetime, more so if they are not intentionally working towards it. Conversely, ultra-wealthy high net worth individuals like Jeff Bezos that has added value to humanity is able to in theory have a disposal income of $1 million each year for 195,000 years if it was even humanly possible to live up to 195,000 years old.

Below is a chart from CNBC Make it, source by Bloomberg to show you the 6 richest people in 2021.

And while there is so much advice out there when it comes to building wealth, one of the most important suggestions that are often repeated (for good reason) is to start investing as early as you can.

It can be a real struggle to invest especially when you have rent, student loans, emergency funds, debts, a social life that you have to take care of. However, investing in your future should also be considered a priority.

How much money you want to have at the end of the day ultimately depends on:

- How much you invest

- The rate of return

- The time period for your investment to compound

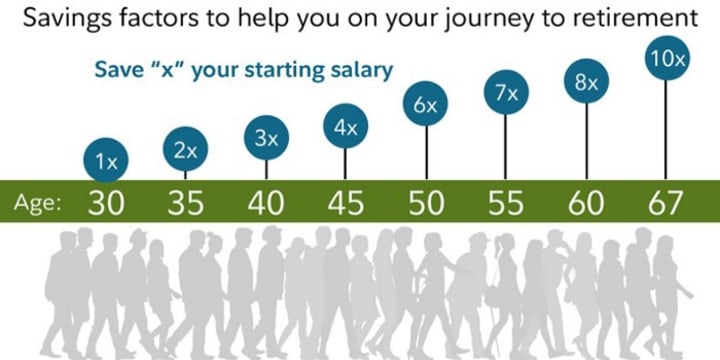

Most experts agree that by the time you are 60, you should have eight or ten times your current annual salary in retirement savings. So for example, if your starting salary is $50,000 in your first job in your 20’s by the time you reach your 60’s you should have around $400,000 saved up.

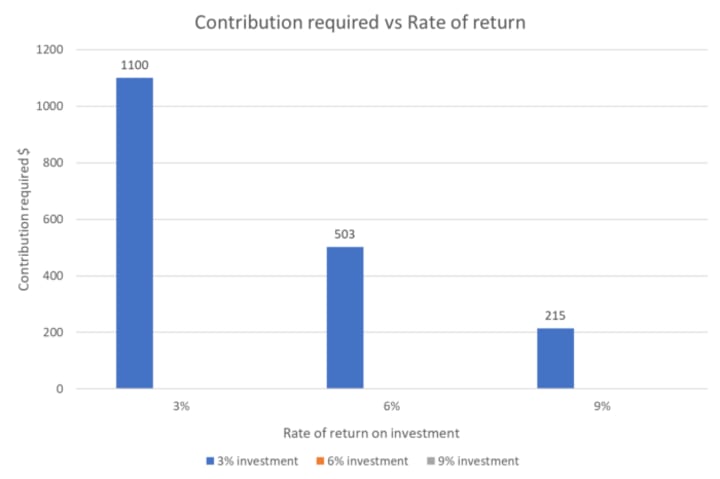

When crunching the numbers here are the three different return rates. The retirement age of 65 was used, which would give 25-year-olds 40 years to reach $1 million.

Here’s are the numbers:

- 25-year-old making investments that yield a 3% yearly return would have to invest $1,100 per month for 40 years to reach $1 million.

- If they instead make investments that give a 6% yearly return, they would have to invest $503 per month for 40 years to reach $1 million.

- But if they choose more aggressive investments that yield a 9% yearly return, they would only need to invest $215 per month for 40 years to reach $1 million.

This will give you an idea of how much you need to set aside depending on the rate of return of your investment.

This shows you how critical the rate of return on your investment vehicle is in affecting how much you need to contribute each month. If your investment vehicle is generating a higher return per annum, you would require a lesser amount to contribute compared to if your investments generated a lower rate of return.

Hence, you always want to consider what investments vehicle you use to grow and compound your investments. The calculation above assumes a fixed rate of return annually although, in reality, most investments could go up and down throughout the 40 year period.

These milestones in this example are estimates. You likely won’t meet all of them. The interest rate of returns could change year on year, the rate of inflation could change, the amount that you can contribute may change and other external factors beyond one’s control. But for the most part, they can serve as a benchmark to help you make a plan to invest enough to reach the $1 million mark.

So what investment vehicles to consider?

Based on the chart above you can a higher return can allow you to invest less money each month and still achieve the same goal. A 3% return is common for a more conservative portfolio of mostly bonds, money market accounts, and treasury bills, whereas a 6% return is a bit more moderate and usually consists of a combination of stocks and bonds. However, a 9% return is on the more aggressive end and can usually be received through a portfolio that’s stock heavy.

A good strategy would be to consider a low-cost broad range index fund or ETF that tracks the stock market as a whole, as the S&P 500. According to Investopedia, the S&P 500 has historically returned an average of 10% to 11%.

Some ETF examples that you can consider include the IVV, SPLG, VOO and SPY.

You can also consider investing in individual shares of a company if you are comfortable with the company’s overall financial health, position in the marketplace, potential growth & viability and current & future prospects.

Why people don’t invest?

When Business Insider and Insider Intelligence asked millennials (defined as ages 21 to 38) about their investment behaviours for the Master Your Money Invest & Thrive Survey, many said their income is part of what’s holding them back from investing.

Based on the survey, in total, 41% of the 2,020 survey respondents said they’re not currently investing in any financial products.

Among them, 48% said they don’t have enough money. Exactly half of the non-investors said earning more would cause them to start.

Other reasons cited included:

- Focusing on savings.

- Not understanding how to invest.

- Not having enough money which was the top choice cited.

The simple truth is that the earlier you start saving and investing, the easier it is for you to reach your goal. There will be losses to contend with, but generally, the stock market goes up over time.

Conclusion

If you wait for the perfect moment to take the plunge well, you might learn there’s no such thing. Lastly, don’t let your life be defined by what you didn’t know or didn’t do. Start today, you’ll be glad you did.

About the Creator

Bitcoin Tests a Critical Zone as the Fed Signals a Pause

As of January 19, 2026, Bitcoin is once again approaching a psychologically significant price level. After climbing to approximately 97,000 dollars, Bitcoin has reached its highest level in nearly two months. This recovery has reignited market discussion around whether Bitcoin can attempt another move toward the 100,000 dollar mark before February. However, expectations that the Federal Reserve will maintain its current interest rate policy remain a critical variable shaping investor sentiment.

By crypto geniea day ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.