From $3,000 to $20,000 Profit: A Trader’s Case Study Using FXroad

A practical, no-hype review of one trader’s strategy development, risk process, and the FXroad features that helped along the way.

Overview

This is the story of a retail trader let’s call him Mark who spent six months building and testing his own trading system, then took it live with FXroad and turned an initial $3,000 into a $20,000 profit over the following year. This isn’t a get-rich-quick tale; it’s a blueprint: the habits, tools, and risk rules he used, how he handled setbacks, why he chose FXroad, and the exact mechanics of his strategy. Where relevant, you’ll find real numbers, a month-by-month progression, and the psychological framework that kept him consistent.

Important: This is one person’s experience, not typical or guaranteed. Trading leveraged CFDs and forex involves significant risk. Past performance does not predict future results.

Why FXroad?

Before we get into the strategy, it’s worth understanding the broker choice. Mark had three non-negotiables:

Execution quality during the London and London-New York overlap (his primary trading windows).

Transparent costs, especially spreads and commissions on EUR/USD and XAU/USD (his two core markets).

Reliable funding - fast deposits for flexibility and straightforward withdrawals to lock in milestones.

What he found with FXroad:

Consistent execution on MT5 (his preferred platform), even around scheduled data releases - slippage was present during extreme volatility, as expected, but fills were clean outside of those windows.

Competitive costs - tight majors, stable gold spreads during active sessions, and straightforward fee schedules.

Smooth payouts - his first “confidence withdrawal” of $75 arrived same day via e-wallet; larger bank-wire withdrawals during the year typically landed within 24–48 hours.

These points mattered not just for convenience: they fed back into his risk math. If spreads widen unexpectedly or withdrawals are slow, the strategy’s edge and the trader’s psychology both suffer. FXroad checked those boxes for him.

The Strategy: “HTF Structure + LTF Trigger”

Core markets: EUR/USD and XAU/USD

Timeframes:

Higher timeframe (HTF): Daily & 4H (for structure and directional bias)

Lower timeframe (LTF): 15M (for entries), sometimes 5M (for precision on news days)

System idea: Trade with the higher-timeframe trend after a pullback to value, then wait for the lower timeframe to confirm momentum shift. This avoids trying to “call tops/bottoms” and focuses on catching the meat of the move.

The Four Rules

Bias: Only trade in the direction of the HTF swing (HH/HL = long; LH/LL = short).

Zone of interest: Enter only from value—prior demand/supply, 200 EMA, or session VWAP clusters.

Trigger: LTF break of structure (BOS) or strong momentum candle off the zone.

Risk: Fixed fractional—1.0% per trade early on, later 1.25–1.5% once the live stats proved stable. Maximum of two correlated positions at the same time.

Risk & Trade Management

Initial stop: Just beyond the structure that invalidates the setup (never random pip counts).

Sizing formula:

Position size = (Account Equity × Risk%) / Stop Distance (in $)

Take-profits:

TP1 at +1R, close 50% and move stop to breakeven.

Trail remainder behind developing swing structure or via ATR, whichever kept him in the trend longer.

No-go periods:

He avoided fresh entries within 30–45 minutes of high-impact news unless already partially secured (after TP1).

He skipped low-liquidity hours (late NY/early Asia) unless gold was trending smoothly.

The Build: Backtest → Demo → Micro-Live → Scale

Mark treated the build as a mini product launch.

Backtest (6 years, spot checks by regime)

He didn’t try to label every tick; he sampled trending, range, and volatile periods for both EUR/USD and gold to make sure the rules held up.

He tracked expectancy, not just win rate:

Expectancy = (Win% × Avg Win) – (Loss% × Avg Loss)

The system needed positive expectancy across multiple regimes to proceed.

Demo (8 weeks)

Traded exactly as if live: same session windows, same routine, same screenshots, same risk % (scaled to demo size).

Required two consecutive profitable months with no rule breaks before going live.

Micro-Live (the $3,000 start)

First three weeks at 0.75% risk per trade to absorb the emotional jump to real money.

One tiny withdrawal in Week 2 to confirm payout speed.

After four weeks of clean stats, he moved to 1.0% risk.

Scaling

Risk increased to 1.25–1.5% only after three live months with controlled drawdown (<10%) and consistent expectancy.

No “rewarding a hot hand.” The risk change was pre-scheduled and rule-based.

The First Big Edge: Journaling and Review

Every trade had three screenshots: pre-plan, entry, and exit with brief notes. Each weekend, Mark reviewed:

Win rate, profit factor, and average R

Peak-to-valley drawdown and the recovery time from equity dips

Session analysis: London vs. overlap performance

Rule integrity: Any revenge trades? Any entries inside the no-go window?

The review didn’t just pat him on the back. It told him what to stop doing. Early on, he cut countertrend gold fades entirely. That single change lifted his average R and lowered drawdown.

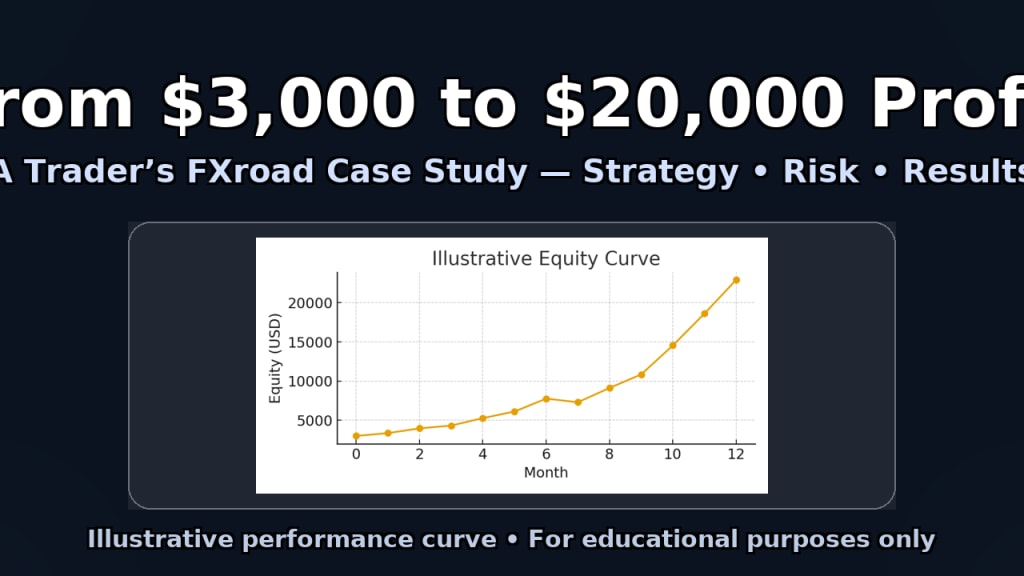

Month-by-Month Progression

Below is a simplified version of his year. These are rounded numbers that reflect the equity curve logic he recorded (starting equity $3,000, ending equity $23,000, i.e., $20,000 profit). Returns varied month to month; the key was compounding with controlled risk.

Final month push, paid self via withdrawal

This path isn’t “normal”; it’s the result of a good market year, rule discipline, and letting compounding do the heavy lifting. Some years will be flatter. The drawdown month (−6%) was psychologically hard, but the process didn’t change that’s the difference between a system and a hunch.

Three Representative Trades

1) EUR/USD Continuation (Month 4)

HTF: Daily uptrend; 4H pullback to prior demand

LTF trigger: 15M BOS; strong close above minor range

Risk: 1%

Management: 50% at +1R; trail behind 15M swing lows

Outcome: +2.4R net after trailing

Why it worked: Simple confluence - structure + location + momentum. No hero moves.

2) Gold Trend Leg (Month 6)

HTF: Daily uptrend; 4H compression under a key level

LTF: Explosive break; minor pullback; momentum continuation

Risk: 1%

Management: TP1 at +1R; ATR-based trail on remainder

Outcome: +3.1R

Why it worked: He didn’t try to “top tick.” He entered after momentum confirmed, then let the trailing logic capture the leg.

3) Choppy Week Recovery (Month 7)

Context: Three small losers early in the week (−1.5% total)

Change: Reduced size to 0.75% for the remainder of the week; waited for cleaner HTF condition

Result: Single +2.2R trade recovered the dip; ended week roughly flat

Why it mattered: He protected mental capital. Instead of chasing, he slowed down and let probability reassert itself.

The Psychology That Made It Work

One setup, many reps. He didn’t add five “edges.” He ran one system across two markets.

Pre-commitment. The risk ladder and upgrade path were defined before the year began.

Rule-based scaling. Size went up only after time and metrics said so.

Withdrawal habit. Small, regular withdrawals created tangible wins and reduced the urge to gamble.

Where FXroad Helped (and Why It’s Relevant)

Execution on MT5 during his preferred windows felt consistent; no odd freezes in his logs. That made it easier to trust his entries.

Costs stayed within his expected ranges, which kept expectancy intact.

Funding & support were predictable. There was always someone human to clarify symbol specs or margin during busier weeks.

These aren’t minor points. A lot of otherwise solid systems are undermined by sloppy fills or opaque costs. Mark’s broker choice supported the edge; it didn’t fight it.

What He Would Do Differently

Quicker pruning of B-setups. The data said “ditch countertrend gold” in Month 2; he waited until Month 3.

Earlier ATR trails. On trending months, wider ATR trails beat structure trails. He made that switch mid-year.

More rest days. The best weeks came after weekends where he unplugged completely.

Practical Takeaways (Steal These)

Write your risk ladder before you begin (when to increase risk, and by how much).

Journal with screenshots planning, entry, and exit so reviews aren’t guesswork.

Make a tiny withdrawal in Month 1; process confidence matters.

Track expectancy, not just wins. A 50% win rate can beat 70% if your average R is higher.

Reduce size after a sting. Protect mental capital; you’re not a robot.

Keep the playbook small. One setup across two or three liquid markets is enough to compound.

FAQs

Is a 6–8× return in a year realistic?

It’s possible, but not typical. It requires a good system, a good market year, clean execution, unflinching risk discipline, and a lot of luck. Many years will be far lower; some will be negative.

Why not 3–5% risk per trade to get there faster?

Because larger risk increases drawdown depth and the odds of emotional decision-making. Mark’s edge relied on survival first, compounding second.

Could this work with a different broker?

Potentially. The key is execution, costs, and funding reliability. FXroad happened to meet those needs for him.

Final Word

Turning $3,000 into $20,000 profit didn’t happen because of a secret indicator. It happened because Mark built a repeatable process, reviewed it weekly, protected his risk per trade, and chose a broker FXroad whose execution, costs, and funding didn’t sabotage his edge.

If you want to follow this path, copy the process, not the number. Start small, verify withdrawals early, journal relentlessly, prune what doesn’t work, and let compounding do the heavy lifting.

About the Creator

Keep reading

More stories from Linda Morris and writers in Trader and other communities.

AI Tools for Forex Trading (Tested on Algobi)

Why use AI for FX? AI won’t magically predict every candle. What it can do—reliably—is compress research time, enforce risk discipline, and surface high-probability conditions you might otherwise miss. In my tests on Algobi (WebTrader with TradingView-grade charts + MT5 desktop/mobile), AI helped me:

By Linda Morris4 months ago in Trader

Building Consistency With Commodities Trading Strategies

Commodities markets attract traders who seek diversification, price transparency, and exposure to global supply and demand trends. This guide explains how commodities trading strategies fit within a balanced approach, with practical insights designed to support disciplined planning and steady execution for your portfolio.

By Miguel Militao4 days ago in Trader

The steps to losing a child

Step One: Lose a child. Not what anyone wants to happen and nothing you can do to change it, but you can go through steps to becoming happy again. You can go through steps to loving again. You can go through steps to become a new you because after losing a child you will never be the same person you once were.

By Tabitha Hinkley3 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.