Debt: An Eye of the Storm

The battle has not yet over; it has only just begun.

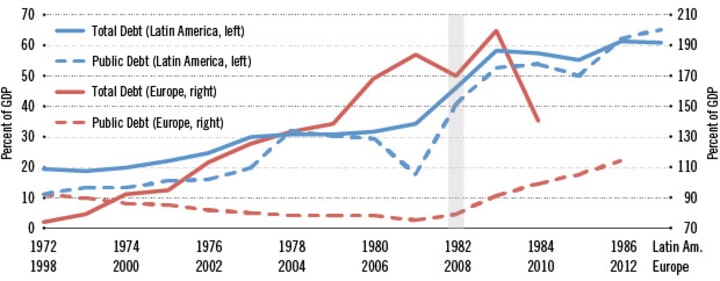

Do you remember the 80s glorious times? Sometimes called as “green decade”. The age of extreme fashion such as ‘big hair’, Rap music, and Breakdance. A strange and magical era that is still celebrated widely but not in Latin America. They called the 80s ‘Lost Decade’.

Why?

They faced financial turmoil in the 80s. A debt typhoon that eroded their economies. High oil prices disturbed their finances, causing large deficits, pushing their foreign debt to historic highs, and pushing their economies to collapse. Mexico was the first country to fall in 1982. It declared that it will not be able to pay its debt. What followed was a series of sovereign defaults in Latin America one country after another.

Three decades on, is history repeating itself? Developing countries the world over are struggling with a sovereign debt crisis. One of them had already succumbed.

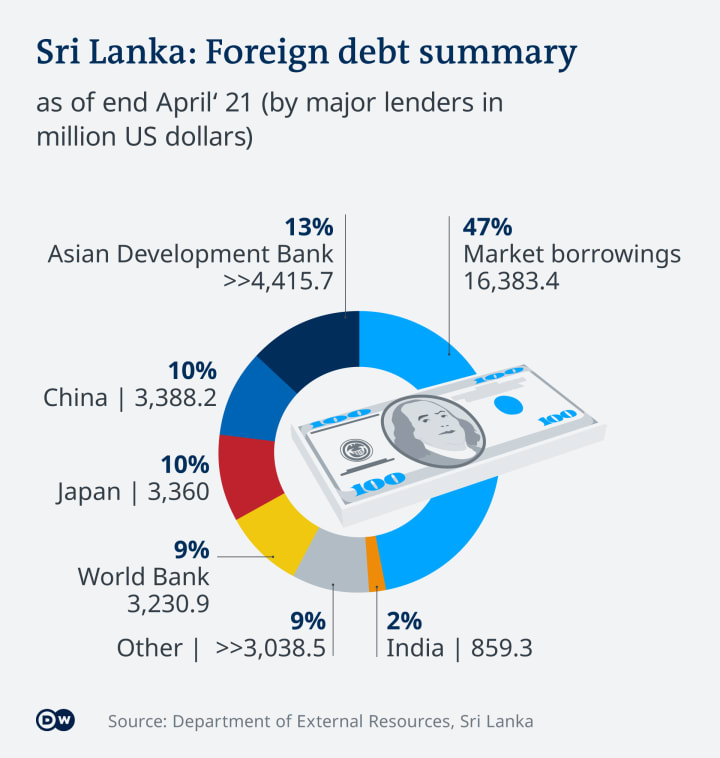

Srilanka has collapsed after ballooning debt and depleting foreign reserves. People are unable to pay for basic necessities. Their oil reserves are empty leading to long-stranded lines. This results from mismanaged finances, unviable spending, and deep tax cuts. But look at the global factors. Russia’s invasion of Ukraine, the Covid-19 pandemic, soaring oil prices, increased food prices, high inflation, and high borrowing costs have compounded the Srilankan crisis.

And the irony is, World does not have time to look at them.

Colombo is just the canary in the coal mine. More countries are said to fall. The entire developing world is at risk.

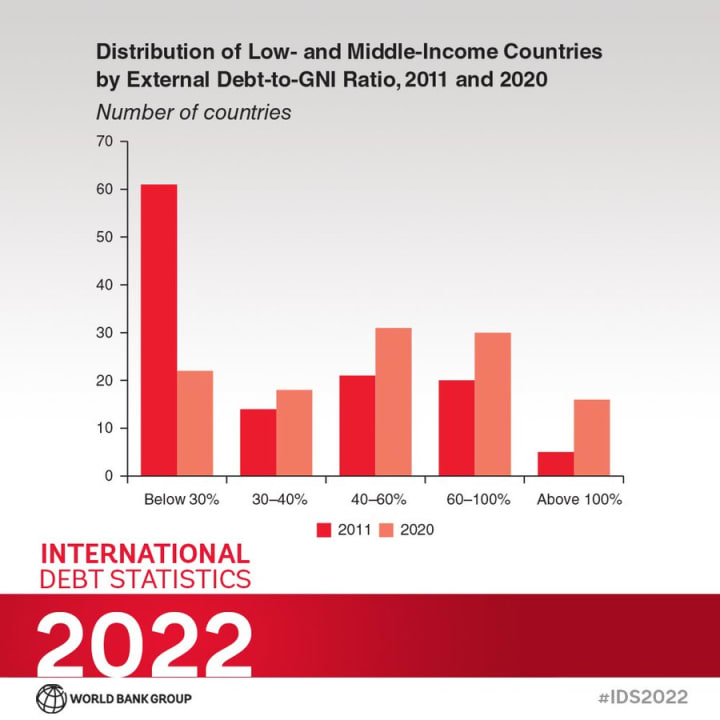

Nine days before Russia invaded Ukraine, World Bank issued a warning that developing and low-income countries may face a debt crisis. Nine days later Russia invaded Ukraine and it threw financial markets into disarray and it triggered oil crises. Disrupted supply chains can lead to a food crisis. In the next month, United Nations released a report in which it listed 107 countries that may face at least one of the risks out of three.

First, Rising food prices. Second, rising oil prices. And third, tougher financial conditions.

There are 69 countries that face all three risks. That means they can go the Srilankan way.

Now We have Argentina, the land of tango in Latin America. They are also caught on the wrong foot. High inflation is paralyzing its economy along with mounting external debt. They had defaulted 9 times on debt repayment. Now they are at IMF’s door to avoid the 10th one, amounting to 45 billion. In the same way, other countries, like Peru and El Salvador, face hyperinflation, soaring food prices, and mass unemployment.

In Africa, Egypt is hit by supply chain disruptions. Egypt is the largest wheat importer and Ukraine and Russia are the largest exporter. An invasion, a so-called “special military operation” by Putin, has ignited a food crisis in Egypt. Food supplies are getting out of stock.

Tunisia, the birthplace of Arab spring, has a debt of more than 100 percent of its GDP. It is overheating under a high trade deficit, and higher inflation.

In sub-Saharan Africa, Ghana, Kenya, and South Africa could be the worst hit. Kenya has debt climbed to 70 billion dollars accounting for 70 percent of its GDP. In South Africa, debt has reached 80 percent of its GDP. There is a looming threat of civil unrest.

Now, look at South Asia. Afghanistan is facing a food crisis, receiving wheat from India. Their banking system has collapsed and maintaining their financial accounts on foreign aid. Pakistan Rupees has crossed the 200 mark first time in its history. The Indian rupee has touched its lowest point recently. Global financial institutions have forecasted more than 8% growth for India. But individual states within India have more than 100 percent debt to GDP ratio. And nothing more to say about Srilanka.

The list has not ended here.

Now here is the thing, the entire world is in debt distress. National debts are at breaking points, and some governments are forced to cut spending, some are borrowing heavily to stay afloat.

But what can we do to stop this? How can the world prevent a debt typhoon?

Low-income countries are always vulnerable to external crises as a high proportion of their debt is external currency. To increase their resiliency, the world needs to develop a sustainable mechanism to absorb external shocks and restructure its debt better. Alternatively, developing countries can help them to build social and economic frameworks. High levels of literacy rate and empowered human capital can increase their job opportunities and income levels.

It is not one-way traffic. Low-income countries must insulate themself from unusual confidentiality clauses of borrowing. They must not succumb to foreign policy dictates and save themselves from debt traps. Srilanka is a classic example of it.

For far the too long world has looked the other way. A debt crisis can emerge as a security issue very much like Covid-19 which has ripple effects all over the world. Relief comes very late and very little. A preemptive action framework must be in place to immune the world from a global recession.

The world is one!

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Read next->> Srilakan crisis- 2022

So, what can I write for you? Feel Free to Suggest Topics in the Comment Section. If I could help you with my articles, you can buy me a coffee for support.

Don't forget to Subscribe, Share, and Like!

About the Creator

NoExitStories

Unsolved cases. Haunted towns. Lost people.

Once you're in, there’s no way out. Each story with no dead-end.

Welcome to NoExitStories.

Keep reading

More stories from NoExitStories and writers in Trader and other communities.

kospi index market update investors watch sudden shift in South Korea stocks

kospi index is one of the most important indicators of the South Korean stock market. Investors around the world track the kospi index daily to understand how major companies in South Korea are performing. When the kospi index moves, it reflects the overall mood of the market. Recently, the kospi index has shown a new trend that is attracting strong attention from traders and long-term investors. Market activity has increased, and several sectors are helping the kospi index maintain steady movement. Because of this change, many investors are closely watching the kospi index for signals about the next market direction.

By John.doe7984 days ago in Trader

Silver Price Outlook: Market Trends, Investment Demand, and Future Expectations

Silver Price Analysis: Market Trends and Future Outlook The silpricever has always attracted the attention of investors, traders, and commodity analysts around the world. As one of the most important precious metals, silver plays a dual role in the global economy. It is not only a safe-haven investment like gold but also a critical industrial metal used in electronics, solar panels, and manufacturing. Because of these unique characteristics, movements in the silver price often reflect both financial market sentiment and industrial demand.

By Hammad Nawaz5 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.