Australian Mortgage Brokers Dominate

Australian Mortgage Brokers

Mortgage brokers have become a cornerstone of Australia’s home lending system, with their popularity skyrocketing among borrowers. Known for their ability to secure competitive deals, brokers offer not only low interest rates but also value-added benefits such as offset accounts, redraw facilities, and refinancing cashbacks. This dominant role is reflected in recent data, underscoring why brokers are indispensable in the lending process—and why this trend matters to investors.

The Rise of Australian Mortgage Brokers

According to the latest Mortgage & Finance Association of Australia (MFAA) report, mortgage brokers now facilitate 74.6% of all new home loans. This represents a 3.1 percentage point increase compared to the previous year and accounts for a staggering $103.2 billion in total loan value. Such numbers highlight how borrowers are increasingly turning to brokers for their expertise and personalized services.

Anja Pannek, CEO of the MFAA, commented on the trend: “Mortgage brokers are central to Australia’s home lending ecosystem. Their role drives competition, ensures better access to loans, and provides tailored solutions to borrowers in an evolving financial landscape.”

Impact on Banks and Investors

While broker-facilitated loans bring advantages for consumers, they pose financial challenges for banks. Brokers earn commissions from lenders, including upfront and trailing fees, which can erode banks’ profitability. For example, a 0.7% commission on a $1 million loan equals $7,000—a significant cost for banks in the loan’s initial stages.

Research by UBS underscores the impact of broker-channel loans on bank profitability. It reveals that loans offered through brokers with cashback incentives and a two-year churn rate yield an internal rate of return (IRR) of -58.4%. By contrast, proprietary loans without cashback offers and a six-year tenure generate an IRR of 16.7%.

For investors, these figures underline the importance of understanding a bank’s exposure to broker-originated loans. Commonwealth Bank of Australia (CBA) stands out with the lowest reliance on brokers among the Big Four banks, with just 43% of its loans written through this channel. In contrast, broker-originated loans for NAB, Westpac, and ANZ exceed 60%, impacting their net interest margins (NIM) and overall profitability.

The Role of Small Banks

Smaller banks, such as Pepper Money and Auswide Bank, are even more reliant on mortgage brokers. Lacking the brand recognition of the Big Four, these institutions depend heavily on brokers to reach potential customers. However, this dependency comes at a cost. Smaller banks often have to offer lower rates and still pay broker commissions, which puts additional pressure on their already tight profit margins.

Despite growing loan books, smaller banks struggle to maintain investor confidence due to these challenges. For investors, the heavy reliance on brokers makes these institutions less attractive compared to larger banks with diversified revenue streams and lower operational risks.

Why Brokers Are Here to Stay

The appeal of mortgage brokers lies in their ability to provide borrowers with tailored financial solutions, competitive interest rates, and access to a wide range of loan products. Additionally, their growing market share is a testament to consumer trust and the value they bring to the lending process.

For banks, adapting to the broker-driven market is crucial. While brokers might reduce banks’ profitability on a per-loan basis, they also expand the overall market by connecting borrowers who might not approach banks directly. This duality means that banks must strike a balance between managing costs and leveraging the reach of brokers.

Conclusion

Australian mortgage brokers have reshaped the home lending landscape, with their influence extending to both borrowers and banks. For investors, understanding the dynamics of broker-channel loans is essential. Banks with lower reliance on brokers, such as CBA, may offer more stable returns, while those heavily dependent on brokers face tighter margins and higher risks.

As brokers continue to dominate the market, their role in shaping Australia’s financial ecosystem remains undeniable. Whether you’re a borrower or an investor, staying informed about these trends can help you make better financial decisions.

About the Creator

Keep reading

More stories from AP The writer and writers in Trader and other communities.

Is a February rate cut from the RBA back on the table?

As we approach the first Reserve Bank of Australia (RBA) meeting for 2024, speculation grows about the possibility of a February rate cut. Mortgage holders and investors alike are cautiously optimistic, fueled by economic data and recent comments from the central bank. While there are no guarantees, signs of easing inflation and sluggish economic growth are providing hope for some much-needed relief.

By AP The writerabout a year ago in Trader

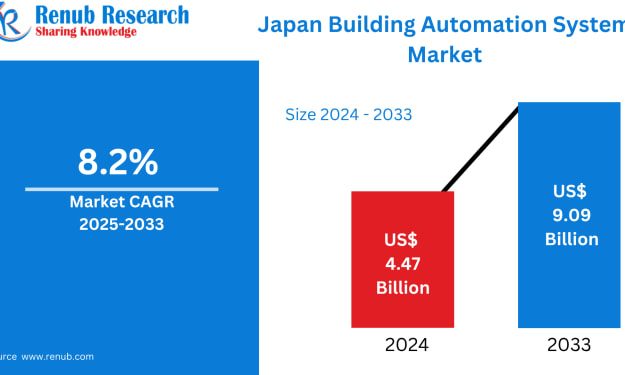

Japan Building Automation Systems Market Size and Forecast 2025–2033

Introduction Japan is undergoing a profound transformation in the way its buildings are designed, managed, and operated. From skyscrapers in Tokyo to manufacturing hubs in Aichi and logistics centers in Chiba, the demand for smarter, more energy-efficient, and digitally connected infrastructure is accelerating. At the center of this transformation lies the Building Automation Systems (BAS) market, which integrates mechanical, electrical, and electromechanical services into a centralized, intelligent control framework.

By Marthan Sir6 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.